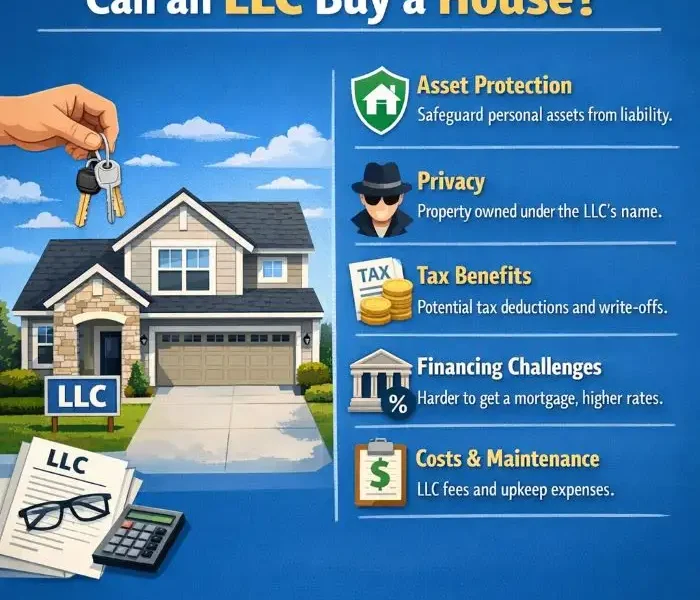

<p>If you have ever asked, <strong>“<a href="https://www.reddit.com/r/FirstTimeHomeBuyers/comments/1gfp2zv/rich_people_buy_houses_all_the_time_with_an_llc/">can an LLC buy a house</a>?”</strong>, you are not alone. A lot of real estate investors start with this exact question.</p>

<p>And it makes sense.</p>

<p>Buying property is a big financial move. It can create income, build wealth, and open the door to long-term growth. But it also creates risk. If something goes wrong—a lawsuit, a tenant injury, a debt issue, or a contract dispute—you do not want your personal assets exposed if you can avoid it.</p>

<p>That is why many investors look at using an <strong>LLC</strong>, or <strong>Limited Liability Company</strong>, to hold real estate.</p>

<p>For the right person, this setup can offer <strong>liability protection</strong>, <strong>better separation between business and personal finances</strong>, and <strong>more flexibility</strong> as your portfolio grows. But it is not a perfect fit for every situation. It can also create challenges with financing, ongoing fees, paperwork, and certain tax or homeowner benefits.</p>

<p>In this guide, you will learn <strong>how buying a house through an LLC works</strong>, when it makes sense, when it does not, and what steps you need to follow if you want to do it the right way.</p>

<p>If you are thinking about protecting your rentals or building a real estate business, this article will help you make a more confident decision.</p>

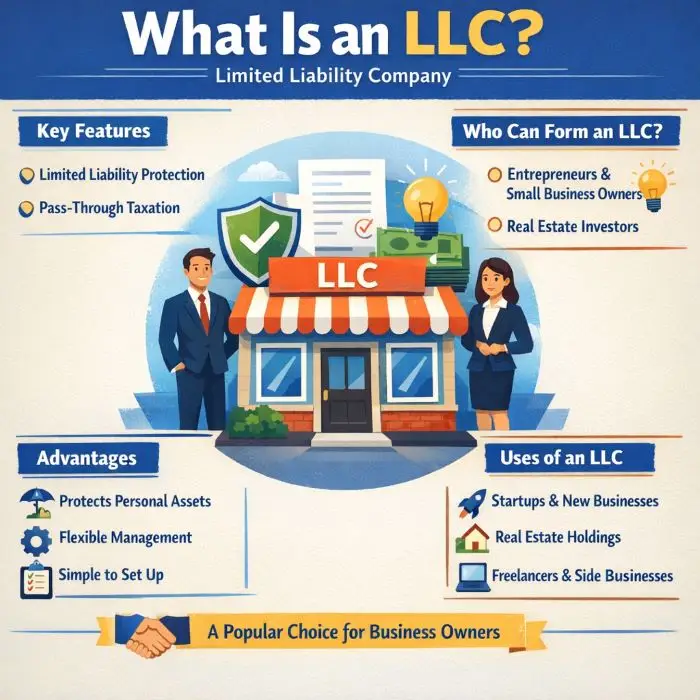

<h2 id="what-is-an-llc-">What Is an LLC?</h2>

<p><img class="aligncenter wp-image-6937 size-full" src="https://comeawayhome.co.uk/wp-content/uploads/2026/05/118548f6-94b2-4336-9e46-395f0fea90ced-ezgif.com-jpg-to-webp-converter.webp" alt="can an llc buy a house" width="700" height="700" /></p>

<h3 id="definition-and-basic-purpose">Definition and Basic Purpose</h3>

<p>An <strong>LLC</strong>, short for <strong>Limited Liability Company</strong>, is a legal business structure that sits somewhere between a corporation and a sole proprietorship.</p>

<p>In simple terms, it gives you a way to run a business while creating some legal separation between <strong>you</strong> and <strong>the business</strong>.</p>

<p>That separation matters.</p>

<p>If an LLC owns a property and the property becomes part of a lawsuit or debt issue, the goal is to keep the problem inside the LLC rather than letting it spill over into your personal life. That means your <strong>personal bank account, car, or other assets</strong> may be better protected—assuming you set everything up correctly and keep the business separate from your personal finances.</p>

<p>That is one of the biggest reasons real estate investors like LLCs.</p>

<p>Another reason is flexibility. LLCs are usually easier to manage than corporations. They often have fewer formal rules, and they can work well for one owner or several partners.</p>

<p>So if you want to buy a rental home, hold a flip project, or build a small portfolio of income properties, an LLC can be a very practical tool.</p>

<h3 id="who-owns-an-llc-">Who Owns an LLC?</h3>

<p>The owners of an LLC are called <strong>members</strong>.</p>

<p>A single-member LLC has one owner. A multi-member LLC has two or more owners.</p>

<p>The LLC can also be managed in different ways. In some cases, the members manage it themselves. In other cases, they appoint a manager to run the business side.</p>

<p>This matters when buying a <a href="https://comeawayhome.co.uk/the-white-house/">house</a> because the LLC—not you personally—will be listed as the buyer. An authorized person signs on the LLC’s behalf.</p>

<h3 id="why-investors-use-llcs-for-real-estate">Why Investors Use LLCs for Real Estate</h3>

<p>Real estate creates both <strong>opportunity</strong> and <strong>exposure</strong>.</p>

<p>Let’s say you own a rental property in your personal name. A tenant sues after an accident on the property. In that case, your personal ownership can make things more complicated and risky.</p>

<p>Now imagine the same rental is owned by a properly formed LLC with separate bank accounts, clear records, and business insurance. That setup may provide a stronger layer of protection.</p>

<p>That is why LLCs are often used for:</p>

<ul>

<li><strong>Rental houses</strong></li>

<li><strong>Vacation rentals</strong></li>

<li><strong>Fix-and-flip projects</strong></li>

<li><strong>Small multifamily properties</strong></li>

<li><strong>Commercial real estate</strong></li>

</ul>

<h3 id="llc-vs-personal-ownership">LLC vs. Personal Ownership</h3>

<p>When you buy in your personal name, the transaction is usually simpler. Mortgage options are often better. You may qualify more easily. And if the home is your primary residence, you may keep certain homeowner protections and tax benefits.</p>

<p>But simple does not always mean safest.</p>

<p>When you buy through an LLC, you add a layer of business structure. That can help with risk management, but it also adds paperwork and cost.</p>

<p>So the real question is not just <strong>can an LLC buy a house</strong>.</p>

<p>The better question is this:</p>

<p><strong>Should your LLC buy this specific house for this specific goal?</strong></p>

<p>That is where strategy comes in.</p>

<h2 id="can-an-llc-buy-a-house-legality-explained">Can an LLC Buy a House? Legality Explained</h2>

<h3 id="yes-an-llc-can-buy-a-house">Yes, an LLC Can Buy a House</h3>

<p>Let’s answer the main question clearly.</p>

<p><strong>Yes, an LLC can buy a house.</strong></p>

<p>In general, an LLC can own real estate just like an individual can. That includes many types of property, such as single-family homes, small rental properties, multifamily buildings, land, and even commercial spaces.</p>

<p>From a legal standpoint, an LLC is allowed to enter contracts, hold title, open bank accounts, borrow money, and own assets. Real estate falls under that umbrella.</p>

<p>So if you are wondering whether an LLC can be listed on a purchase contract and deed, the answer is <strong>yes</strong>.</p>

<h3 id="why-this-matters">Why This Matters</h3>

<p>This matters because ownership affects everything that comes after the purchase.</p>

<p>It affects:</p>

<ul>

<li><strong>Who signs the deal</strong></li>

<li><strong>Who receives rent</strong></li>

<li><strong>Who gets sued if a claim happens</strong></li>

<li><strong>How income and expenses are reported</strong></li>

<li><strong>How the property is financed</strong></li>

<li><strong>How the property may be transferred later</strong></li>

</ul>

<p>In other words, the name on the deed is not just a detail. It shapes the legal and financial structure around the property.</p>

<h3 id="the-rule-for-all-50-states">The Rule for All 50 States</h3>

<p>Broadly speaking, LLCs can purchase property in all U.S. states. But the way LLCs are formed, maintained, and regulated can vary by state.</p>

<p>That means the basic answer is yes, but the <strong>costs, filing requirements, privacy rules, annual reports, and fees</strong> may differ depending on where the LLC is formed and where the property is located.</p>

<p>This is especially important if you plan to form an LLC in one state and buy property in another. In that case, you may need to register as a <strong>foreign LLC</strong> in the state where the property sits.</p>

<p>That extra step can add complexity and cost.</p>

<h3 id="primary-residence-vs-investment-property">Primary Residence vs. Investment Property</h3>

<p>Here is where many people get tripped up.</p>

<p>Just because an LLC <strong>can</strong> buy a house does not mean it should buy <strong>every</strong> kind of house.</p>

<p>For <strong>investment property</strong>, LLC ownership often makes sense.</p>

<p>For a <strong>primary residence</strong>, it is usually less attractive.</p>

<p>Why? Because putting your main home in an LLC may create downsides such as:</p>

<ul>

<li>Harder mortgage approval</li>

<li>Higher interest rates</li>

<li>Loss of some homeowner protections</li>

<li>Possible loss of homestead benefits in some states</li>

<li>Insurance complications if the home is owner-occupied</li>

</ul>

<p>So while an LLC is often a strong move for a rental house, it is usually not the best structure for the home you live in every day.</p>

<h3 id="best-use-cases-for-llc-ownership">Best Use Cases for LLC Ownership</h3>

<p>If you are buying a property mainly to produce income or build a real estate business, LLC ownership often fits well.</p>

<p>Here is a simple breakdown:</p>

<table>

<thead>

<tr>

<th>Property Type</th>

<th>LLC Suitability</th>

<th>Main Advantage</th>

</tr>

</thead>

<tbody>

<tr>

<td>Rental House</td>

<td>High</td>

<td><strong>Liability protection</strong> and business separation</td>

</tr>

<tr>

<td>Vacation Rental</td>

<td>High</td>

<td>Easier to treat as a business asset</td>

</tr>

<tr>

<td>Flip Project</td>

<td>High</td>

<td>Clean structure for buying, renovating, and selling</td>

</tr>

<tr>

<td>Small Commercial Property</td>

<td>High</td>

<td>Useful for business operations and scaling</td>

</tr>

<tr>

<td>Primary Residence</td>

<td>Low</td>

<td>May reduce personal homeowner benefits</td>

</tr>

</tbody>

</table>

<p>The takeaway is simple: <strong>LLCs are generally best for business or investment real estate, not personal homeownership.</strong></p>

<h2 id="step-by-step-how-to-buy-a-house-with-an-llc">Step-by-Step: How to Buy a House With an LLC</h2>

<p>If you want to move forward, you need to do more than just create an LLC name and start shopping.</p>

<p>You need a clean process.</p>

<p>Here is the big-picture roadmap:</p>

<ol>

<li><strong>Form the LLC</strong></li>

<li><strong>Get an EIN and business documents in place</strong></li>

<li><strong>Open a business bank account</strong></li>

<li><strong>Secure financing or prepare cash</strong></li>

<li><strong>Make the offer in the LLC’s name</strong></li>

<li><strong>Complete due diligence</strong></li>

<li><strong>Close with the LLC on the deed</strong></li>

<li><strong>Maintain the LLC properly after closing</strong></li>

</ol>

<p>Now let’s walk through each step in detail.</p>

<h3 id="step-1-form-the-llc">Form the LLC</h3>

<p>Before the LLC can buy property, the LLC has to legally exist.</p>

<p>That starts with filing formation documents with the state. In most states, this means filing <strong>Articles of Organization</strong> or a similarly named form.</p>

<p>Once the state approves the filing, your LLC becomes a legal entity.</p>

<p>At this stage, you should also choose:</p>

<ul>

<li>The official LLC name</li>

<li>The registered agent</li>

<li>Whether it is member-managed or manager-managed</li>

<li>Who the members are</li>

<li>What the business purpose will be</li>

</ul>

<p>If you plan to use the LLC for real estate, make sure the business purpose allows for property ownership and related activities.</p>

<h3 id="step-2-create-an-operating-agreement">Create an Operating Agreement</h3>

<p>Even if your state does not require it, you should have an <strong>Operating Agreement</strong>.</p>

<p>This document explains how the LLC works.</p>

<p>It can cover things like:</p>

<ul>

<li>Ownership percentages</li>

<li>Voting rights</li>

<li>Profit distributions</li>

<li>Who can sign contracts</li>

<li>What happens if a member leaves</li>

<li>How major decisions are made</li>

</ul>

<p>If you are the only owner, this still matters. It helps show that the LLC is a real business structure and not just a name on paper.</p>

<p>That can be important for legal protection and for dealing with lenders, title companies, or attorneys.</p>

<h3 id="step-3-get-an-ein">Get an EIN</h3>

<p>An <strong>EIN</strong>, or Employer Identification Number, works like a tax ID number for your business.</p>

<p>You may need it to:</p>

<ul>

<li>Open a business bank account</li>

<li>Apply for financing</li>

<li>File taxes</li>

<li>Set up vendor accounts</li>

<li>Show that the LLC operates as a separate entity</li>

</ul>

<p>Even a single-member LLC often gets an EIN for practical business purposes.</p>

<h3 id="step-4-open-a-business-bank-account">Open a Business Bank Account</h3>

<p>This is one of the most important steps.</p>

<p>If you want the LLC to protect you, you need to <strong>treat it like a real business</strong>.</p>

<p>That means keeping business money separate from personal money.</p>

<p>Open a bank account in the LLC’s name and use it for:</p>

<ul>

<li>Down payments</li>

<li>Closing costs</li>

<li>Repair expenses</li>

<li>Rent deposits</li>

<li>Insurance payments</li>

<li>Contractor bills</li>

<li>Property taxes</li>

<li>Mortgage payments, if applicable</li>

</ul>

<p>When owners mix business funds with personal funds, they can weaken the LLC’s legal shield. This is sometimes called <strong>piercing the corporate veil</strong>, even though an LLC is not a corporation in the strict sense.</p>

<p>The message is simple: <strong>separate means separate</strong>.</p>

<h3 id="step-5-plan-your-financing">Plan Your Financing</h3>

<p>This is where many buyers hit their first real obstacle.</p>

<p>It is often easier to get a mortgage in your personal name than in an LLC’s name.</p>

<p>That is because many traditional home loans are designed for owner-occupied residential property—not for business entities.</p>

<p>If your LLC is buying the house, your financing may come from:</p>

<ul>

<li><strong>Commercial lenders</strong></li>

<li><strong>Portfolio lenders</strong></li>

<li><strong>Private lenders</strong></li>

<li><strong>Hard money lenders</strong></li>

<li><strong>Seller financing</strong></li>

<li><strong>Cash</strong></li>

</ul>

<p>In many cases, lenders want:</p>

<ul>

<li>A larger down payment</li>

<li>A higher interest rate</li>

<li>Strong cash reserves</li>

<li>A personal guarantee from the LLC owner</li>

<li>Proof the LLC is active and in good standing</li>

</ul>

<p>So yes, an LLC can buy a house with financing, but the process is often less friendly than a standard mortgage for a personal residence.</p>

<p>If you already own the property personally and want to transfer it to an LLC later, be careful. Some mortgages include a <strong>due-on-sale clause</strong>, which can allow the lender to call the loan due if ownership changes. That does not always happen in practice, but it is a real risk that you should not ignore.</p>

<h3 id="step-6-search-for-the-right-property">Search for the Right Property</h3>

<p>Once your LLC is active and your financing plan is clear, you can begin searching for the property itself.</p>

<p>At this point, it helps to think like a business owner, not just a buyer.</p>

<p>Ask questions such as:</p>

<ul>

<li>Will this property cash flow?</li>

<li>What is the repair budget?</li>

<li>What insurance will I need?</li>

<li>Are there local rental rules?</li>

<li>Does the neighborhood support my strategy?</li>

<li>Will this property fit inside the long-term goals of the LLC?</li>

</ul>

<p>This step matters because the LLC structure is only part of the equation. The property still needs to be a sound investment.</p>

<h3 id="step-7-make-the-offer-in-the-llc-s-name">Make the Offer in the LLC’s Name</h3>

<p>When you are ready to buy, the purchase contract should list the <strong>LLC as the buyer</strong>.</p>

<p>That sounds simple, but it matters a lot.</p>

<p>If you sign the contract in your personal name and try to swap in the LLC later, that can create title, lending, or closing issues.</p>

<p>The cleaner approach is to buy in the LLC’s name from the start whenever possible.</p>

<p>The person signing should sign as an authorized representative, such as:</p>

<p><strong>ABC Property Holdings, LLC, by Jane Smith, Member</strong></p>

<p>That wording helps make it clear that the business—not the individual—is the purchaser.</p>

<h3 id="step-8-complete-due-diligence">Complete Due Diligence</h3>

<p>Before closing, do your normal property checks.</p>

<p>That may include:</p>

<ul>

<li>Home inspection</li>

<li>Appraisal</li>

<li>Title review</li>

<li>Survey</li>

<li>Insurance quote</li>

<li>Repair estimates</li>

<li>Lease review if tenants are in place</li>

<li>Zoning or permit review if needed</li>

</ul>

<p>Try to keep these documents in the LLC’s file and complete them in the LLC’s name when practical.</p>

<p>You want a clean paper trail that supports the business structure.</p>

<h3 id="step-9-close-properly">Close Properly</h3>

<p>At closing, the final deed should transfer title to the LLC.</p>

<p>Double-check that:</p>

<ul>

<li>The LLC name is correct</li>

<li>The signer is properly authorized</li>

<li>The closing documents match the contract</li>

<li>The insurance policy reflects LLC ownership</li>

<li>The funds come from the LLC account when possible</li>

<li>The LLC is in good standing if the title company requires proof</li>

</ul>

<p>After closing, store all records carefully. That includes the settlement statement, deed, insurance, loan documents, and organizational documents.</p>

<h3 id="step-10-maintain-the-llc-after-purchase">Maintain the LLC After Purchase</h3>

<p>This is the part people forget.</p>

<p>Buying the house through an LLC is not a one-time trick. It is an ongoing business structure.</p>

<p>You need to maintain it.</p>

<p>That means filing annual reports, paying state fees, keeping records, renewing business licenses if needed, and continuing to use the LLC bank account for LLC business.</p>

<p>If you stop treating it like a business, you weaken the very protection you created it for.</p>

<blockquote><p><strong>Pro tip:</strong> If privacy is a concern, some investors look at states that offer more anonymity. But remember, the best state for formation is not always the best state for ownership. If your property is in another state, extra registration may still be required.</p></blockquote>

<h2 id="pros-and-cons-of-llc-house-ownership">Pros and Cons of LLC House Ownership</h2>

<p>Buying real estate through an LLC can be smart. But it is not automatically smart.</p>

<p>You need to look at both sides.</p>

<h3 id="key-benefits-of-buying-a-house-through-an-llc">Key Benefits of Buying a House Through an LLC</h3>

<h4 id="1-liability-protection">Liability Protection</h4>

<p>This is the headline benefit.</p>

<p>If the property is owned by the LLC and a tenant, contractor, guest, or vendor brings a claim tied to that property, the LLC may help shield your personal assets.</p>

<p>That does not make you untouchable. But it may help limit the damage to the assets inside the business structure.</p>

<p>For many investors, that protection alone is the reason they choose this path.</p>

<h4 id="2-cleaner-separation-between-business-and-personal-life">Cleaner Separation Between Business and Personal Life</h4>

<p>Real estate investing becomes easier to manage when you stop mixing it with your personal finances.</p>

<p>An LLC gives you a natural framework for that separation.</p>

<p>You can collect rent into the LLC account, pay repairs from the LLC account, track expenses more clearly, and create cleaner records for taxes, partners, and future deals.</p>

<p>That kind of organization becomes more valuable as your portfolio grows.</p>

<h4 id="3-tax-flexibility">Tax Flexibility</h4>

<p>An LLC is often a <strong>pass-through entity</strong> by default. That means the profits and losses usually pass through to the owner’s personal tax return rather than being taxed at the entity level in the same way a traditional corporation might be.</p>

<p>This can keep the tax side simpler for many investors.</p>

<p>Also, investment properties may allow deductions for common business expenses, which can improve your overall numbers.</p>

<h4 id="4-privacy-in-some-cases">Privacy in Some Cases</h4>

<p>In some states, LLC ownership can offer more privacy than personal ownership.</p>

<p>That does not mean invisible ownership. But it may reduce how directly your personal name appears in public property records, depending on the structure and the state.</p>

<p>For some investors, that added layer of privacy is appealing.</p>

<h4 id="5-easier-portfolio-growth">Easier Portfolio Growth</h4>

<p>If you plan to buy several properties, an LLC can make your investing feel more like a real business.</p>

<p>That can help with:</p>

<ul>

<li>Bringing in partners</li>

<li>Assigning ownership percentages</li>

<li>Tracking profits</li>

<li>Creating management systems</li>

<li>Selling membership interests later in some cases</li>

</ul>

<p>This is one reason more serious investors tend to think in terms of entities, not just individual properties.</p>

<h3 id="major-drawbacks-of-buying-a-house-through-an-llc">Major Drawbacks of Buying a House Through an LLC</h3>

<h4 id="1-financing-can-be-harder">Financing Can Be Harder</h4>

<p>This is the biggest downside for many buyers.</p>

<p>Traditional residential mortgages are often built for individuals, especially owner-occupants. Once an LLC enters the picture, the lender may treat the deal differently.</p>

<p>That can mean:</p>

<ul>

<li>Higher rates</li>

<li>Bigger down payments</li>

<li>More paperwork</li>

<li>Fewer lender choices</li>

<li>A required personal guarantee</li>

</ul>

<p>So even though an LLC can buy a house, the money side may be less convenient.</p>

<h4 id="2-extra-costs">Extra Costs</h4>

<p>An LLC is not free to create or maintain.</p>

<p>You may face:</p>

<ul>

<li>Formation fees</li>

<li>Annual report fees</li>

<li>Franchise taxes in some states</li>

<li>Registered agent fees</li>

<li>Accounting costs</li>

<li>Legal setup costs</li>

</ul>

<p>If you own just one modest property, these extra costs may not feel worth it.</p>

<h4 id="3-more-administrative-work">More Administrative Work</h4>

<p>LLCs come with responsibility.</p>

<p>You need to maintain records, keep accounts separate, sign documents correctly, and stay compliant with state rules.</p>

<p>If you are not willing to handle that, or pay someone to help, the LLC may become more of a headache than a benefit.</p>

<h4 id="4-potential-loss-of-personal-homeowner-benefits">Potential Loss of Personal Homeowner Benefits</h4>

<p>If you put a primary residence into an LLC, you may give up important benefits depending on state law and lender rules.</p>

<p>These may include:</p>

<ul>

<li>Homestead protections</li>

<li>Owner-occupied mortgage options</li>

<li>Certain tax advantages</li>

<li>Easier insurance arrangements</li>

</ul>

<p>This is why LLC ownership is usually stronger for investment property than for a home you live in.</p>

<h4 id="5-loan-transfer-risks">Loan Transfer Risks</h4>

<p>If you already own a house personally and want to move it into an LLC, do not assume you can do that without consequences.</p>

<p>Your mortgage documents may restrict transfers. Title changes can also affect insurance and tax treatment.</p>

<p>That does not mean it is impossible. It means you need to review the situation carefully before acting.</p>

<h3 id="pros-vs-cons-at-a-glance">Pros vs. Cons at a Glance</h3>

<table>

<thead>

<tr>

<th>Pros</th>

<th>Cons</th>

</tr>

</thead>

<tbody>

<tr>

<td><strong>Liability protection</strong> for investment activities</td>

<td><strong>Financing is often tougher</strong></td>

</tr>

<tr>

<td>Better separation of business and personal money</td>

<td>Formation fees and annual costs</td>

</tr>

<tr>

<td>Tax flexibility for many investors</td>

<td>More paperwork and compliance</td>

</tr>

<tr>

<td>Helpful for portfolio growth</td>

<td>May lose personal homeowner benefits</td>

</tr>

<tr>

<td>Potential privacy advantages in some states</td>

<td>Existing mortgages can complicate transfers</td>

</tr>

</tbody>

</table>

<p>The bottom line is simple: <strong>an LLC can be powerful, but only if the property and your goals justify the extra structure.</strong></p>

<h2 id="tax-implications-of-buying-a-house-through-an-llc">Tax Implications of Buying a House Through an LLC</h2>

<h3 id="pass-through-taxation">Pass-Through Taxation</h3>

<p>In many cases, an LLC does not pay tax as a separate entity by default.</p>

<p>Instead, income and losses usually <strong>pass through</strong> to the owner or owners. For a single-member LLC, that often means the activity is reported on the owner’s tax return. For a multi-member LLC, a partnership-style return may apply.</p>

<p>This setup is one reason LLCs are popular.</p>

<p>It can offer flexibility without forcing you into the full structure of a corporation.</p>

<h3 id="common-real-estate-deductions">Common Real Estate Deductions</h3>

<p>If the property is held as an investment, the LLC may allow you to track and claim legitimate business expenses more cleanly.</p>

<p>Those may include things like:</p>

<ul>

<li>Mortgage interest</li>

<li>Property taxes</li>

<li>Insurance</li>

<li>Repairs and maintenance</li>

<li>Property management fees</li>

<li>Legal and accounting fees</li>

<li>Utilities paid by the owner</li>

<li>Advertising for tenants</li>

<li>Depreciation</li>

</ul>

<p>Depreciation is a major concept in real estate because it allows owners to deduct a portion of a property’s value over time, subject to tax rules.</p>

<p>This can significantly affect your taxable income.</p>

<h3 id="transfer-taxes-and-re-titling-issues">Transfer Taxes and Re-Titling Issues</h3>

<p>If you already own a property personally and then transfer it into an LLC, you may trigger more than just loan issues.</p>

<p>Depending on where the property is located, you may also face:</p>

<ul>

<li>Transfer taxes</li>

<li>Recording fees</li>

<li>Reassessment concerns</li>

<li>Insurance changes</li>

</ul>

<p>That is why transferring a property after purchase should be reviewed carefully rather than done casually.</p>

<h3 id="keep-good-records">Keep Good Records</h3>

<p>No matter how simple or complex your LLC is, strong records matter.</p>

<p>Track:</p>

<ul>

<li>Rent received</li>

<li>Security deposits</li>

<li>Repairs</li>

<li>Capital improvements</li>

<li>Loan interest</li>

<li>Travel and management costs if applicable</li>

<li>Year-end statements</li>

</ul>

<p>The cleaner your records, the easier your tax filing becomes.</p>

<h3 id="why-a-cpa-matters">Why a CPA Matters</h3>

<p>Real estate taxes can get complicated fast.</p>

<p>This is especially true if you are dealing with:</p>

<ul>

<li>Multiple members</li>

<li>Short-term rentals</li>

<li>Cost segregation</li>

<li>1031 exchanges</li>

<li>Refinancing</li>

<li>Depreciation recapture</li>

<li>A mix of personal and business use</li>

</ul>

<p>A CPA who understands real estate can help you avoid expensive mistakes and find deductions you might miss.</p>

<h2 id="state-specific-rules-you-should-know">State-Specific Rules You Should Know</h2>

<h3 id="not-every-state-treats-llcs-the-same">Not Every State Treats LLCs the Same</h3>

<p>The broad answer to <strong>can an LLC buy a house</strong> is yes.</p>

<p>But the practical experience depends a lot on the state.</p>

<p>Some states are known for higher fees. Others are known for stronger privacy. Some are more investor-friendly in general. And some give homeowners protections that may not apply once a property is held in an LLC.</p>

<p>That is why state law matters.</p>

<h3 id="states-with-higher-costs">States With Higher Costs</h3>

<p>Some states have relatively high filing fees, annual fees, or franchise taxes for LLCs.</p>

<p>If your property is small or your margins are thin, those recurring costs can reduce the value of the LLC structure.</p>

<p>That does not mean you should avoid those states. It just means you need to run the numbers honestly.</p>

<h3 id="privacy-friendly-states">Privacy-Friendly States</h3>

<p>Some investors prefer states that offer more owner privacy or more flexible business laws.</p>

<p>That can sound attractive, and in some cases it helps.</p>

<p>But remember: if the property is in another state, you may still need to register there and comply with local rules. So forming in a privacy-friendly state does not automatically remove all exposure or paperwork.</p>

<h3 id="homestead-and-investor-considerations">Homestead and Investor Considerations</h3>

<p>States also differ when it comes to:</p>

<ul>

<li>Homestead rights</li>

<li>Creditor protection rules</li>

<li>Property tax treatment</li>

<li>Landlord-tenant laws</li>

<li>Recording and transfer rules</li>

</ul>

<p>If the house is a rental, landlord-tenant law may be just as important as LLC law.</p>

<p>If the house is your primary residence, homestead rules may matter even more.</p>

<p>The lesson here is simple: <strong>state details can change the strategy</strong>, even when the overall answer stays yes.</p>

<h2 id="common-mistakes-and-how-to-avoid-them">Common Mistakes and How to Avoid Them</h2>

<p>A lot of people set up an LLC because they want protection. Then they accidentally weaken that protection by how they operate.</p>

<p>Here are some of the most common mistakes:</p>

<ul>

<li><strong>Mixing personal and business funds</strong></li>

<li><strong>Buying in a personal name and trying to fix it later</strong></li>

<li><strong>Skipping the Operating Agreement</strong></li>

<li><strong>Ignoring annual reports and state filings</strong></li>

<li><strong>Using the wrong insurance setup</strong></li>

<li><strong>Assuming an existing mortgage can be transferred safely</strong></li>

<li><strong>Putting a primary residence into an LLC without understanding the trade-offs</strong></li>

<li><strong>Failing to document member decisions</strong></li>

<li><strong>Treating the LLC like a nickname instead of a real business</strong></li>

<li><strong>Not getting legal or tax advice for a complex deal</strong></li>

</ul>

<h3 id="why-mixing-funds-is-so-dangerous">Why Mixing Funds Is So Dangerous</h3>

<p>This one deserves special attention.</p>

<p>If your rent goes into your personal account, repairs get paid from your personal debit card, and the LLC exists only on paper, you are creating a problem.</p>

<p>Courts and creditors look at behavior, not just documents.</p>

<p>If you do not respect the separation, others may argue that the LLC should not be respected either.</p>

<h3 id="the-best-way-to-avoid-problems">The Best Way to Avoid Problems</h3>

<p>The safest path is usually the simplest one:</p>

<p><strong>Set up the LLC correctly, buy in the LLC’s name from the beginning, keep the money separate, maintain the records, and ask professionals when the deal gets complicated.</strong></p>

<p>That approach is not flashy. But it works.</p>

<h2 id="frequently-asked-questions">Frequently Asked Questions</h2>

<h3 id="can-an-llc-buy-a-house-with-a-mortgage-">Can an LLC buy a house with a mortgage?</h3>

<p><strong>Yes, an LLC can buy a house with a mortgage.</strong></p>

<p>But the loan is often not the same as a standard personal home loan. Many LLC buyers use commercial, portfolio, or investor-focused lenders. Expect more scrutiny, larger down payments, and sometimes a personal guarantee.</p>

<h3 id="can-i-transfer-my-personal-house-into-an-llc-">Can I transfer my personal house into an LLC?</h3>

<p><strong>Yes, in many cases you can transfer a house into an LLC.</strong></p>

<p>But that does not mean you should do it without review. The transfer may affect your mortgage, insurance, taxes, and legal protections. If the house has an existing loan, check the loan documents before making any move.</p>

<h3 id="is-it-smart-to-put-my-primary-residence-in-an-llc-">Is it smart to put my primary residence in an LLC?</h3>

<p>Usually, <strong>no</strong>, or at least not without very careful planning.</p>

<p>For most people, an LLC is a better fit for <strong>investment property</strong> than for a primary home. A personal residence often comes with benefits that may be reduced or lost in an LLC structure.</p>

<h3 id="is-one-llc-enough-for-multiple-properties-">Is one LLC enough for multiple properties?</h3>

<p>Sometimes yes, sometimes no.</p>

<p>A single LLC can hold multiple properties. That is simple and cheap. But it also means the properties may share risk inside the same entity.</p>

<p>Some investors prefer one LLC per property or one LLC per small group of properties. That costs more, but it can improve asset separation.</p>

<h3 id="what-if-i-am-the-only-owner-">What if I am the only owner?</h3>

<p>That is completely normal.</p>

<p>A <strong>single-member LLC</strong> can still buy and own a house. Many investors start that way. You still need to keep records, separate funds, and operate properly.</p>

<h3 id="does-an-llc-eliminate-the-need-for-insurance-">Does an LLC eliminate the need for insurance?</h3>

<p>No.</p>

<p>This is a big misconception.</p>

<p>An LLC is not a replacement for <strong>landlord insurance, liability insurance, or umbrella coverage</strong>. It is one layer of protection, not the whole plan. In real estate, strong protection usually comes from using the right legal structure <strong>and</strong> the right insurance.</p>

<h3 id="what-is-the-biggest-reason-investors-buy-property-in-an-llc-">What is the biggest reason investors buy property in an LLC?</h3>

<p>For most investors, the biggest reason is <strong>liability protection</strong>.</p>

<p>The second biggest reason is usually <strong>business organization</strong>. Once you start treating your investments like a business, tracking money, risk, and growth becomes easier.</p>

<h2 id="final-thoughts-should-you-buy-a-house-through-an-llc-">Final Thoughts: Should You Buy a House Through an LLC?</h2>

<p>So, <strong>can an LLC buy a house?</strong></p>

<p><strong>Yes, absolutely.</strong></p>

<p>And for many real estate investors, that choice makes a lot of sense.</p>

<p>If you are buying a <strong>rental property</strong>, a <strong>flip</strong>, or another investment asset, an LLC can help you create a cleaner, safer, more professional structure around the deal. It can support liability protection, simplify business operations, and make it easier to grow over time.</p>

<p>But that does not mean it is the right move in every situation.</p>

<p>If you are buying a <strong>primary residence</strong>, if you need the easiest possible financing, or if the ongoing costs outweigh the benefit, personal ownership may be the better route.</p>

<p>The smartest move is not to follow a trend.</p>

<p>It is to match the structure to the purpose.</p>

<p>If you are serious about real estate, think of the LLC as part of a bigger plan that includes financing, insurance, taxes, and state law. When those pieces work together, you create a stronger foundation for long-term investing.</p>

<p>If you are considering your first property purchase through an LLC, start by reviewing your state rules, your financing options, and your long-term goals. Then talk with a qualified attorney or CPA before you close.</p>

<p>And if you are ready to build a real estate business the right way, this is the perfect time to get your LLC structure in place and use it with intention.</p>

<p><a href="https://comeawayhome.co.uk/">House</a></p>

If you have ever asked, “can an LLC buy a house?”, you are not alone. A lot of real estate investors start with this exact question.

And it makes sense.

Buying property is a big financial move. It can create income, build wealth, and open the door to long-term growth. But it also creates risk. If something goes wrong—a lawsuit, a tenant injury, a debt issue, or a contract dispute—you do not want your personal assets exposed if you can avoid it.

That is why many investors look at using an LLC, or Limited Liability Company, to hold real estate.

For the right person, this setup can offer liability protection, better separation between business and personal finances, and more flexibility as your portfolio grows. But it is not a perfect fit for every situation. It can also create challenges with financing, ongoing fees, paperwork, and certain tax or homeowner benefits.

In this guide, you will learn how buying a house through an LLC works, when it makes sense, when it does not, and what steps you need to follow if you want to do it the right way.

If you are thinking about protecting your rentals or building a real estate business, this article will help you make a more confident decision.

What Is an LLC?

Definition and Basic Purpose

An LLC, short for Limited Liability Company, is a legal business structure that sits somewhere between a corporation and a sole proprietorship.

In simple terms, it gives you a way to run a business while creating some legal separation between you and the business.

That separation matters.

If an LLC owns a property and the property becomes part of a lawsuit or debt issue, the goal is to keep the problem inside the LLC rather than letting it spill over into your personal life. That means your personal bank account, car, or other assets may be better protected—assuming you set everything up correctly and keep the business separate from your personal finances.

That is one of the biggest reasons real estate investors like LLCs.

Another reason is flexibility. LLCs are usually easier to manage than corporations. They often have fewer formal rules, and they can work well for one owner or several partners.

So if you want to buy a rental home, hold a flip project, or build a small portfolio of income properties, an LLC can be a very practical tool.

Who Owns an LLC?

The owners of an LLC are called members.

A single-member LLC has one owner. A multi-member LLC has two or more owners.

The LLC can also be managed in different ways. In some cases, the members manage it themselves. In other cases, they appoint a manager to run the business side.

This matters when buying a house because the LLC—not you personally—will be listed as the buyer. An authorized person signs on the LLC’s behalf.

Why Investors Use LLCs for Real Estate

Real estate creates both opportunity and exposure.

Let’s say you own a rental property in your personal name. A tenant sues after an accident on the property. In that case, your personal ownership can make things more complicated and risky.

Now imagine the same rental is owned by a properly formed LLC with separate bank accounts, clear records, and business insurance. That setup may provide a stronger layer of protection.

That is why LLCs are often used for:

- Rental houses

- Vacation rentals

- Fix-and-flip projects

- Small multifamily properties

- Commercial real estate

LLC vs. Personal Ownership

When you buy in your personal name, the transaction is usually simpler. Mortgage options are often better. You may qualify more easily. And if the home is your primary residence, you may keep certain homeowner protections and tax benefits.

But simple does not always mean safest.

When you buy through an LLC, you add a layer of business structure. That can help with risk management, but it also adds paperwork and cost.

So the real question is not just can an LLC buy a house.

The better question is this:

Should your LLC buy this specific house for this specific goal?

That is where strategy comes in.

Can an LLC Buy a House? Legality Explained

Yes, an LLC Can Buy a House

Let’s answer the main question clearly.

Yes, an LLC can buy a house.

In general, an LLC can own real estate just like an individual can. That includes many types of property, such as single-family homes, small rental properties, multifamily buildings, land, and even commercial spaces.

From a legal standpoint, an LLC is allowed to enter contracts, hold title, open bank accounts, borrow money, and own assets. Real estate falls under that umbrella.

So if you are wondering whether an LLC can be listed on a purchase contract and deed, the answer is yes.

Why This Matters

This matters because ownership affects everything that comes after the purchase.

It affects:

- Who signs the deal

- Who receives rent

- Who gets sued if a claim happens

- How income and expenses are reported

- How the property is financed

- How the property may be transferred later

In other words, the name on the deed is not just a detail. It shapes the legal and financial structure around the property.

The Rule for All 50 States

Broadly speaking, LLCs can purchase property in all U.S. states. But the way LLCs are formed, maintained, and regulated can vary by state.

That means the basic answer is yes, but the costs, filing requirements, privacy rules, annual reports, and fees may differ depending on where the LLC is formed and where the property is located.

This is especially important if you plan to form an LLC in one state and buy property in another. In that case, you may need to register as a foreign LLC in the state where the property sits.

That extra step can add complexity and cost.

Primary Residence vs. Investment Property

Here is where many people get tripped up.

Just because an LLC can buy a house does not mean it should buy every kind of house.

For investment property, LLC ownership often makes sense.

For a primary residence, it is usually less attractive.

Why? Because putting your main home in an LLC may create downsides such as:

- Harder mortgage approval

- Higher interest rates

- Loss of some homeowner protections

- Possible loss of homestead benefits in some states

- Insurance complications if the home is owner-occupied

So while an LLC is often a strong move for a rental house, it is usually not the best structure for the home you live in every day.

Best Use Cases for LLC Ownership

If you are buying a property mainly to produce income or build a real estate business, LLC ownership often fits well.

Here is a simple breakdown:

| Property Type |

LLC Suitability |

Main Advantage |

| Rental House |

High |

Liability protection and business separation |

| Vacation Rental |

High |

Easier to treat as a business asset |

| Flip Project |

High |

Clean structure for buying, renovating, and selling |

| Small Commercial Property |

High |

Useful for business operations and scaling |

| Primary Residence |

Low |

May reduce personal homeowner benefits |

The takeaway is simple: LLCs are generally best for business or investment real estate, not personal homeownership.

Step-by-Step: How to Buy a House With an LLC

If you want to move forward, you need to do more than just create an LLC name and start shopping.

You need a clean process.

Here is the big-picture roadmap:

- Form the LLC

- Get an EIN and business documents in place

- Open a business bank account

- Secure financing or prepare cash

- Make the offer in the LLC’s name

- Complete due diligence

- Close with the LLC on the deed

- Maintain the LLC properly after closing

Now let’s walk through each step in detail.

Before the LLC can buy property, the LLC has to legally exist.

That starts with filing formation documents with the state. In most states, this means filing Articles of Organization or a similarly named form.

Once the state approves the filing, your LLC becomes a legal entity.

At this stage, you should also choose:

- The official LLC name

- The registered agent

- Whether it is member-managed or manager-managed

- Who the members are

- What the business purpose will be

If you plan to use the LLC for real estate, make sure the business purpose allows for property ownership and related activities.

Create an Operating Agreement

Even if your state does not require it, you should have an Operating Agreement.

This document explains how the LLC works.

It can cover things like:

- Ownership percentages

- Voting rights

- Profit distributions

- Who can sign contracts

- What happens if a member leaves

- How major decisions are made

If you are the only owner, this still matters. It helps show that the LLC is a real business structure and not just a name on paper.

That can be important for legal protection and for dealing with lenders, title companies, or attorneys.

Get an EIN

An EIN, or Employer Identification Number, works like a tax ID number for your business.

You may need it to:

- Open a business bank account

- Apply for financing

- File taxes

- Set up vendor accounts

- Show that the LLC operates as a separate entity

Even a single-member LLC often gets an EIN for practical business purposes.

Open a Business Bank Account

This is one of the most important steps.

If you want the LLC to protect you, you need to treat it like a real business.

That means keeping business money separate from personal money.

Open a bank account in the LLC’s name and use it for:

- Down payments

- Closing costs

- Repair expenses

- Rent deposits

- Insurance payments

- Contractor bills

- Property taxes

- Mortgage payments, if applicable

When owners mix business funds with personal funds, they can weaken the LLC’s legal shield. This is sometimes called piercing the corporate veil, even though an LLC is not a corporation in the strict sense.

The message is simple: separate means separate.

Plan Your Financing

This is where many buyers hit their first real obstacle.

It is often easier to get a mortgage in your personal name than in an LLC’s name.

That is because many traditional home loans are designed for owner-occupied residential property—not for business entities.

If your LLC is buying the house, your financing may come from:

- Commercial lenders

- Portfolio lenders

- Private lenders

- Hard money lenders

- Seller financing

- Cash

In many cases, lenders want:

- A larger down payment

- A higher interest rate

- Strong cash reserves

- A personal guarantee from the LLC owner

- Proof the LLC is active and in good standing

So yes, an LLC can buy a house with financing, but the process is often less friendly than a standard mortgage for a personal residence.

If you already own the property personally and want to transfer it to an LLC later, be careful. Some mortgages include a due-on-sale clause, which can allow the lender to call the loan due if ownership changes. That does not always happen in practice, but it is a real risk that you should not ignore.

Search for the Right Property

Once your LLC is active and your financing plan is clear, you can begin searching for the property itself.

At this point, it helps to think like a business owner, not just a buyer.

Ask questions such as:

- Will this property cash flow?

- What is the repair budget?

- What insurance will I need?

- Are there local rental rules?

- Does the neighborhood support my strategy?

- Will this property fit inside the long-term goals of the LLC?

This step matters because the LLC structure is only part of the equation. The property still needs to be a sound investment.

Make the Offer in the LLC’s Name

When you are ready to buy, the purchase contract should list the LLC as the buyer.

That sounds simple, but it matters a lot.

If you sign the contract in your personal name and try to swap in the LLC later, that can create title, lending, or closing issues.

The cleaner approach is to buy in the LLC’s name from the start whenever possible.

The person signing should sign as an authorized representative, such as:

ABC Property Holdings, LLC, by Jane Smith, Member

That wording helps make it clear that the business—not the individual—is the purchaser.

Complete Due Diligence

Before closing, do your normal property checks.

That may include:

- Home inspection

- Appraisal

- Title review

- Survey

- Insurance quote

- Repair estimates

- Lease review if tenants are in place

- Zoning or permit review if needed

Try to keep these documents in the LLC’s file and complete them in the LLC’s name when practical.

You want a clean paper trail that supports the business structure.

Close Properly

At closing, the final deed should transfer title to the LLC.

Double-check that:

- The LLC name is correct

- The signer is properly authorized

- The closing documents match the contract

- The insurance policy reflects LLC ownership

- The funds come from the LLC account when possible

- The LLC is in good standing if the title company requires proof

After closing, store all records carefully. That includes the settlement statement, deed, insurance, loan documents, and organizational documents.

Maintain the LLC After Purchase

This is the part people forget.

Buying the house through an LLC is not a one-time trick. It is an ongoing business structure.

You need to maintain it.

That means filing annual reports, paying state fees, keeping records, renewing business licenses if needed, and continuing to use the LLC bank account for LLC business.

If you stop treating it like a business, you weaken the very protection you created it for.

Pro tip: If privacy is a concern, some investors look at states that offer more anonymity. But remember, the best state for formation is not always the best state for ownership. If your property is in another state, extra registration may still be required.

Pros and Cons of LLC House Ownership

Buying real estate through an LLC can be smart. But it is not automatically smart.

You need to look at both sides.

Key Benefits of Buying a House Through an LLC

Liability Protection

This is the headline benefit.

If the property is owned by the LLC and a tenant, contractor, guest, or vendor brings a claim tied to that property, the LLC may help shield your personal assets.

That does not make you untouchable. But it may help limit the damage to the assets inside the business structure.

For many investors, that protection alone is the reason they choose this path.

Cleaner Separation Between Business and Personal Life

Real estate investing becomes easier to manage when you stop mixing it with your personal finances.

An LLC gives you a natural framework for that separation.

You can collect rent into the LLC account, pay repairs from the LLC account, track expenses more clearly, and create cleaner records for taxes, partners, and future deals.

That kind of organization becomes more valuable as your portfolio grows.

Tax Flexibility

An LLC is often a pass-through entity by default. That means the profits and losses usually pass through to the owner’s personal tax return rather than being taxed at the entity level in the same way a traditional corporation might be.

This can keep the tax side simpler for many investors.

Also, investment properties may allow deductions for common business expenses, which can improve your overall numbers.

Privacy in Some Cases

In some states, LLC ownership can offer more privacy than personal ownership.

That does not mean invisible ownership. But it may reduce how directly your personal name appears in public property records, depending on the structure and the state.

For some investors, that added layer of privacy is appealing.

Easier Portfolio Growth

If you plan to buy several properties, an LLC can make your investing feel more like a real business.

That can help with:

- Bringing in partners

- Assigning ownership percentages

- Tracking profits

- Creating management systems

- Selling membership interests later in some cases

This is one reason more serious investors tend to think in terms of entities, not just individual properties.

Major Drawbacks of Buying a House Through an LLC

Financing Can Be Harder

This is the biggest downside for many buyers.

Traditional residential mortgages are often built for individuals, especially owner-occupants. Once an LLC enters the picture, the lender may treat the deal differently.

That can mean:

- Higher rates

- Bigger down payments

- More paperwork

- Fewer lender choices

- A required personal guarantee

So even though an LLC can buy a house, the money side may be less convenient.

An LLC is not free to create or maintain.

You may face:

- Formation fees

- Annual report fees

- Franchise taxes in some states

- Registered agent fees

- Accounting costs

- Legal setup costs

If you own just one modest property, these extra costs may not feel worth it.

More Administrative Work

LLCs come with responsibility.

You need to maintain records, keep accounts separate, sign documents correctly, and stay compliant with state rules.

If you are not willing to handle that, or pay someone to help, the LLC may become more of a headache than a benefit.

Potential Loss of Personal Homeowner Benefits

If you put a primary residence into an LLC, you may give up important benefits depending on state law and lender rules.

These may include:

- Homestead protections

- Owner-occupied mortgage options

- Certain tax advantages

- Easier insurance arrangements

This is why LLC ownership is usually stronger for investment property than for a home you live in.

Loan Transfer Risks

If you already own a house personally and want to move it into an LLC, do not assume you can do that without consequences.

Your mortgage documents may restrict transfers. Title changes can also affect insurance and tax treatment.

That does not mean it is impossible. It means you need to review the situation carefully before acting.

Pros vs. Cons at a Glance

| Pros |

Cons |

| Liability protection for investment activities |

Financing is often tougher |

| Better separation of business and personal money |

Formation fees and annual costs |

| Tax flexibility for many investors |

More paperwork and compliance |

| Helpful for portfolio growth |

May lose personal homeowner benefits |

| Potential privacy advantages in some states |

Existing mortgages can complicate transfers |

The bottom line is simple: an LLC can be powerful, but only if the property and your goals justify the extra structure.

Tax Implications of Buying a House Through an LLC

Pass-Through Taxation

In many cases, an LLC does not pay tax as a separate entity by default.

Instead, income and losses usually pass through to the owner or owners. For a single-member LLC, that often means the activity is reported on the owner’s tax return. For a multi-member LLC, a partnership-style return may apply.

This setup is one reason LLCs are popular.

It can offer flexibility without forcing you into the full structure of a corporation.

Common Real Estate Deductions

If the property is held as an investment, the LLC may allow you to track and claim legitimate business expenses more cleanly.

Those may include things like:

- Mortgage interest

- Property taxes

- Insurance

- Repairs and maintenance

- Property management fees

- Legal and accounting fees

- Utilities paid by the owner

- Advertising for tenants

- Depreciation

Depreciation is a major concept in real estate because it allows owners to deduct a portion of a property’s value over time, subject to tax rules.

This can significantly affect your taxable income.

Transfer Taxes and Re-Titling Issues

If you already own a property personally and then transfer it into an LLC, you may trigger more than just loan issues.

Depending on where the property is located, you may also face:

- Transfer taxes

- Recording fees

- Reassessment concerns

- Insurance changes

That is why transferring a property after purchase should be reviewed carefully rather than done casually.

Keep Good Records

No matter how simple or complex your LLC is, strong records matter.

Track:

- Rent received

- Security deposits

- Repairs

- Capital improvements

- Loan interest

- Travel and management costs if applicable

- Year-end statements

The cleaner your records, the easier your tax filing becomes.

Why a CPA Matters

Real estate taxes can get complicated fast.

This is especially true if you are dealing with:

- Multiple members

- Short-term rentals

- Cost segregation

- 1031 exchanges

- Refinancing

- Depreciation recapture

- A mix of personal and business use

A CPA who understands real estate can help you avoid expensive mistakes and find deductions you might miss.

State-Specific Rules You Should Know

Not Every State Treats LLCs the Same

The broad answer to can an LLC buy a house is yes.

But the practical experience depends a lot on the state.

Some states are known for higher fees. Others are known for stronger privacy. Some are more investor-friendly in general. And some give homeowners protections that may not apply once a property is held in an LLC.

That is why state law matters.

States With Higher Costs

Some states have relatively high filing fees, annual fees, or franchise taxes for LLCs.

If your property is small or your margins are thin, those recurring costs can reduce the value of the LLC structure.

That does not mean you should avoid those states. It just means you need to run the numbers honestly.

Privacy-Friendly States

Some investors prefer states that offer more owner privacy or more flexible business laws.

That can sound attractive, and in some cases it helps.

But remember: if the property is in another state, you may still need to register there and comply with local rules. So forming in a privacy-friendly state does not automatically remove all exposure or paperwork.

Homestead and Investor Considerations

States also differ when it comes to:

- Homestead rights

- Creditor protection rules

- Property tax treatment

- Landlord-tenant laws

- Recording and transfer rules

If the house is a rental, landlord-tenant law may be just as important as LLC law.

If the house is your primary residence, homestead rules may matter even more.

The lesson here is simple: state details can change the strategy, even when the overall answer stays yes.

Common Mistakes and How to Avoid Them

A lot of people set up an LLC because they want protection. Then they accidentally weaken that protection by how they operate.

Here are some of the most common mistakes:

- Mixing personal and business funds

- Buying in a personal name and trying to fix it later

- Skipping the Operating Agreement

- Ignoring annual reports and state filings

- Using the wrong insurance setup

- Assuming an existing mortgage can be transferred safely

- Putting a primary residence into an LLC without understanding the trade-offs

- Failing to document member decisions

- Treating the LLC like a nickname instead of a real business

- Not getting legal or tax advice for a complex deal

Why Mixing Funds Is So Dangerous

This one deserves special attention.

If your rent goes into your personal account, repairs get paid from your personal debit card, and the LLC exists only on paper, you are creating a problem.

Courts and creditors look at behavior, not just documents.

If you do not respect the separation, others may argue that the LLC should not be respected either.

The Best Way to Avoid Problems

The safest path is usually the simplest one:

Set up the LLC correctly, buy in the LLC’s name from the beginning, keep the money separate, maintain the records, and ask professionals when the deal gets complicated.

That approach is not flashy. But it works.

Frequently Asked Questions

Can an LLC buy a house with a mortgage?

Yes, an LLC can buy a house with a mortgage.

But the loan is often not the same as a standard personal home loan. Many LLC buyers use commercial, portfolio, or investor-focused lenders. Expect more scrutiny, larger down payments, and sometimes a personal guarantee.

Can I transfer my personal house into an LLC?

Yes, in many cases you can transfer a house into an LLC.

But that does not mean you should do it without review. The transfer may affect your mortgage, insurance, taxes, and legal protections. If the house has an existing loan, check the loan documents before making any move.

Is it smart to put my primary residence in an LLC?

Usually, no, or at least not without very careful planning.

For most people, an LLC is a better fit for investment property than for a primary home. A personal residence often comes with benefits that may be reduced or lost in an LLC structure.

Is one LLC enough for multiple properties?

Sometimes yes, sometimes no.

A single LLC can hold multiple properties. That is simple and cheap. But it also means the properties may share risk inside the same entity.

Some investors prefer one LLC per property or one LLC per small group of properties. That costs more, but it can improve asset separation.

What if I am the only owner?

That is completely normal.

A single-member LLC can still buy and own a house. Many investors start that way. You still need to keep records, separate funds, and operate properly.

Does an LLC eliminate the need for insurance?

No.

This is a big misconception.

An LLC is not a replacement for landlord insurance, liability insurance, or umbrella coverage. It is one layer of protection, not the whole plan. In real estate, strong protection usually comes from using the right legal structure and the right insurance.

What is the biggest reason investors buy property in an LLC?

For most investors, the biggest reason is liability protection.

The second biggest reason is usually business organization. Once you start treating your investments like a business, tracking money, risk, and growth becomes easier.

Final Thoughts: Should You Buy a House Through an LLC?

So, can an LLC buy a house?

Yes, absolutely.

And for many real estate investors, that choice makes a lot of sense.

If you are buying a rental property, a flip, or another investment asset, an LLC can help you create a cleaner, safer, more professional structure around the deal. It can support liability protection, simplify business operations, and make it easier to grow over time.

But that does not mean it is the right move in every situation.

If you are buying a primary residence, if you need the easiest possible financing, or if the ongoing costs outweigh the benefit, personal ownership may be the better route.

The smartest move is not to follow a trend.

It is to match the structure to the purpose.

If you are serious about real estate, think of the LLC as part of a bigger plan that includes financing, insurance, taxes, and state law. When those pieces work together, you create a stronger foundation for long-term investing.

If you are considering your first property purchase through an LLC, start by reviewing your state rules, your financing options, and your long-term goals. Then talk with a qualified attorney or CPA before you close.

And if you are ready to build a real estate business the right way, this is the perfect time to get your LLC structure in place and use it with intention.

House