Selling your home can feel like a major milestone, but it often comes with a side of stress—particularly when it comes to understanding the taxes involved. Taxes on selling a house can significantly impact your profits, especially if you’re unaware of the rules and strategies that can help you save.

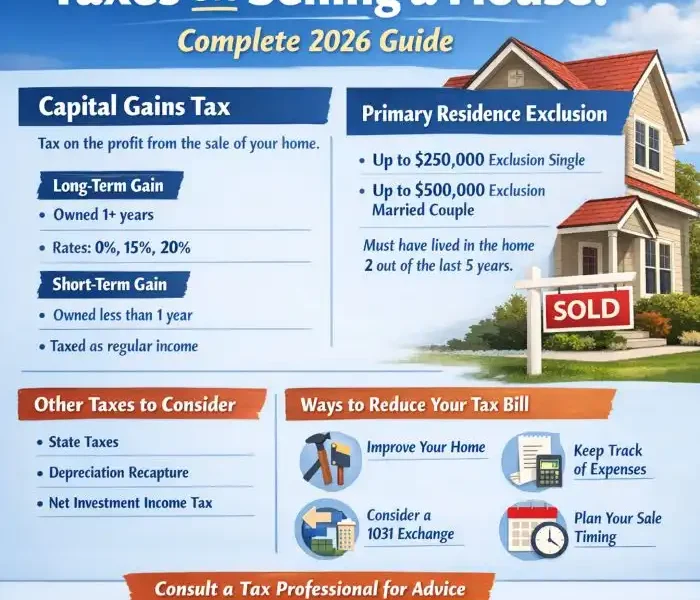

For instance, did you know that under the IRS’s Section 121 exclusion, you could potentially exclude up to $250,000 (or $500,000 for married couples) of your home sale gain from taxes? This guide will walk you through everything you need to know about capital gains tax on home sales, exclusions, rules, exceptions, and strategies to keep as much of your hard-earned money as possible.

Whether you’ve owned your house for years or you’re just beginning to plan your sale, this guide will simplify everything about taxes for you. And remember, if you’re unsure about how these rules apply to your specific situation, consult with a tax professional for personalized advice.

Understanding Capital Gains Tax Basics

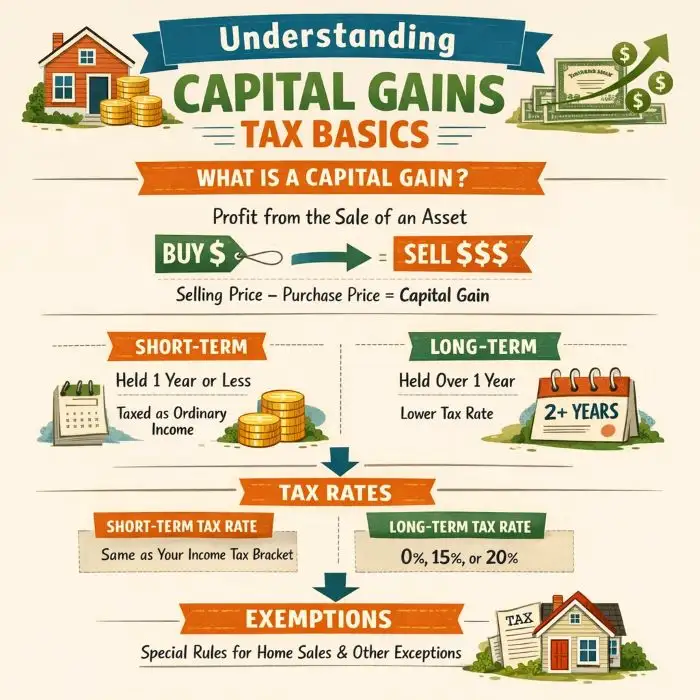

When you sell your home, the IRS is primarily interested in your capital gains—essentially the profit you make from selling your property. Let’s break this down step by step.

What Is Capital Gains Tax?

Capital gains tax applies to the profit you make when selling an asset, such as a home. The formula is fairly straightforward:

The adjusted basis includes what you originally paid for the house, plus certain improvements (e.g., a kitchen remodel) and less depreciation if applicable.

Short-Term vs. Long-Term Gains

The tax rate you pay depends on how long you’ve owned the property:

- Short-term gains (property owned for less than 1 year): Taxed at your ordinary income tax rate (up to 37%).

- Long-term gains (property owned for more than 1 year): Taxed at preferential rates (0%, 15%, or 20%, depending on income).

In 2026, the long-term capital gains tax brackets are as follows:

| Income Level (Single) | Tax Rate | Income Level (Married Filing Jointly) |

|---|---|---|

| Up to $47,000 | 0% | Up to $94,000 |

| $47,001 – $518,000 | 15% | $94,001 – $622,000 |

| Over $518,000 | 20% | Over $622,000 |

State Taxes on Gains

While federal rates are consistent across the country, state taxes on home sales vary widely. Some states, like Florida and Texas, have no state-level capital gains tax, while others like California impose rates as high as 13.3%.

Primary Residence Exclusion Rules

One of the most significant tax breaks available to homeowners is the primary residence exclusion, outlined in IRS Section 121. This exclusion allows you to exclude a substantial portion of your capital gains from taxation.

How the Exclusion Works

If you’ve owned and used your home as your primary residence for at least 2 out of the last 5 years before the sale, you may exclude up to:

- $250,000 of gains if you’re single.

- $500,000 of gains if you’re married and filing jointly.

The 2-year rule doesn’t require the years to be consecutive, as long as you’ve lived in the house for a total of 730 days in the qualifying period.

Examples of Who May Not Qualify

Unfortunately, not everyone qualifies for the full exclusion. Here are some common scenarios where the exclusion might not apply:

- Divorce: If you sell a shared property after separating, only one spouse may meet the use test.

- Inherited Homes: These often qualify for a step-up in basis but not the Section 121 exclusion.

- Rental Properties or Second Homes: If you convert a primary residence to a rental property, your exclusion may be prorated.

Calculating Your Tax Liability Step-by-Step

To determine how much tax you’ll owe when selling your home, follow these simple steps:

Determine the Amount Realized

Subtract selling costs such as realtor commissions, closing fees, and staging expenses from the sale price.

Step 2: Calculate Your Adjusted Basis

Your adjusted basis includes the original purchase price of the home, plus the cost of significant improvements (e.g., adding a deck, new roofing).

Apply the Exclusion

If you qualify for the primary residence exclusion, subtract $250,000 (single) or $500,000 (married) from your gain.

Apply the Correct Tax Rate

If any gain remains taxable, apply the appropriate federal and state tax rates.

Here’s a quick example:

| Sale Price | Adjusted Basis | Selling Costs | Exclusion (Single) | Taxable Gain |

|---|---|---|---|---|

| $600,000 | $300,000 | $40,000 | $250,000 | $10,000 |

In this case, little to no federal tax would be owed since the taxable gain is minimal.

Exceptions and Special Situations

While most home sales follow the standard rules, there are exceptions depending on your specific circumstances.

Inherited Homes

If you inherit a home, the IRS allows for a step-up in basis, which means the property’s value is adjusted to its market value at the time of inheritance. This can significantly reduce taxable gains.

Divorce Sales

When a couple divorces, only one party may meet the 2-year use test. Special considerations apply if the home is sold as part of the divorce settlement.

Rental or Vacation Homes

For properties that were previously rented, depreciation recapture rules apply. This means you’ll pay a 25% tax on any depreciation claimed during the rental period.

Military or Health-Related Moves

If you’re selling your home because of a job relocation, health reasons, or military deployment, you may qualify for a partial exclusion, even if you don’t meet the 2-year residency requirement.

Strategies to Minimize Taxes on Selling a House

Here are some actionable strategies to reduce your tax liability when selling your home:

- Time Your Sale Wisely

If possible, wait until you meet the 2-year primary residence requirement to maximize your exclusion. - Track Improvements

Keep receipts for home improvements, as they increase your adjusted basis and reduce taxable gains. - Leverage Tax-Advantaged Transfers

Consider gifting the property to family members, though be mindful of gift tax limits. - Offset Gains with Losses

If you have other investments that are underperforming, selling them at a loss can offset your taxable home sale gain. - Explore 1031 Exchanges

For rental properties, you can defer taxes by reinvesting the proceeds into a similar property through a 1031 exchange.

Here’s a comparison table showing potential tax savings across scenarios:

| Scenario | Gain | Exclusion | Taxable Gain | Estimated Tax (15%) |

|---|---|---|---|---|

| Single, Qualifies | $400K | $250K | $150K | $22,500 |

| Married, Partial Exclusion | $600K | $300K | $300K | $45,000 |

| Inherited Property | $300K | Step-Up | $50K | $7,500 |

State-Specific Taxes on Home Sales

State tax laws can add a significant layer of complexity when selling your home. For example:

- States like Florida and Texas impose no state-level capital gains taxes, offering a financial advantage.

- High-tax states like California and New York can add up to 13.3% and 8.82%, respectively, to your tax bill.

If you’re planning a move before selling, consider how relocating to a low-tax state might benefit your bottom line.

FAQs

Do I pay taxes on selling a house if I made no profit?

No. Taxes are only levied on gains, not the total sale price.

What happens if I sell before owning the home for 2 years?

You may qualify for a partial exclusion under certain circumstances like job relocations or health issues.

Can I deduct closing costs?

Yes, many closing costs (e.g., realtor fees, title fees) reduce your amount realized and lower your tax liability.

Conclusion

Selling your home doesn’t have to be a taxing experience—literally! By understanding the rules around taxes on selling a house, you can take advantage of exclusions, calculate your liability accurately, and explore strategies to reduce your burden. Planning ahead and consulting with a tax professional can save you thousands.