<p>You sign the papers, move the money, get the keys, and finally move on with your life. But real estate deals do not always move in a straight line. A buyer may find a major repair issue during inspection. A lender may need more documents. A title problem may show up at the last minute. A seller may need extra time because their next home is not ready yet.</p>

<p>That is why so many buyers and sellers ask the same question: <strong>how long can you delay closing on a house</strong> without putting the deal at risk?</p>

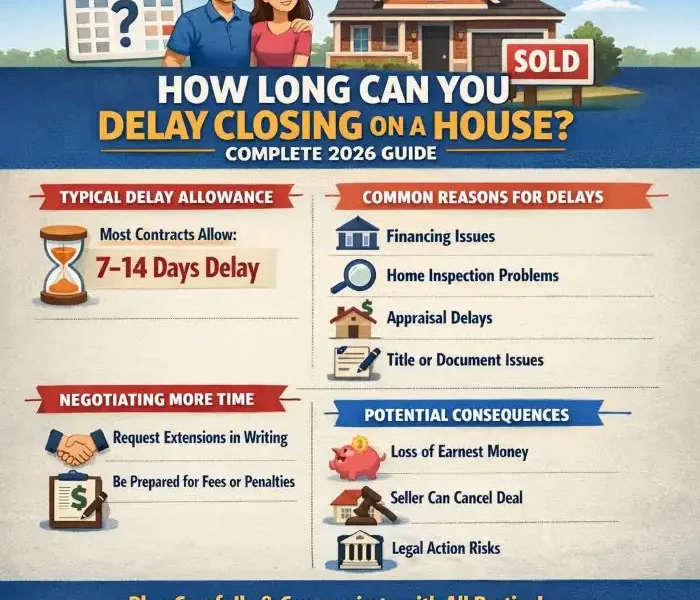

<p>The short answer is this: <strong>most delays are possible for 10 to 30 days</strong>, and sometimes longer, but only if the contract allows it or both sides agree in writing. In many markets, <strong>roughly 10% to 15% of home sales</strong> do not close on the original date. Some are fixed in a few days. Others turn into longer extensions that cost money, create stress, and sometimes cause the deal to fall apart.</p>

<p>If you are buying, selling, or investing, you need to know what is normal, what is risky, and what you can do before the closing date slips away. That is especially important in 2026, when lending standards, insurance issues, and repair negotiations can still slow deals down.</p>

<p>In this guide, you will learn the usual closing timelines, the legal rules behind delays, the most common reasons closings get pushed back, the real costs of waiting, and the smartest ways to ask for more time without losing leverage. You will also see practical alternatives that can save the deal when a full delay is not the best option.</p>

<h2 id="standard-closing-timeline">Standard Closing Timeline</h2>

<h4 id="what-is-the-typical-closing-period-">What Is the Typical Closing Period?</h4>

<p>Before you can understand a delay, you need to understand what a <strong>normal closing timeline</strong> looks like.</p>

<p>In most home sales, the closing period begins once the seller accepts the offer. From there, both sides work through inspections, financing, title work, paperwork, insurance, and final approval. The exact timeline depends on the deal type, the lender, the market, and how quickly everyone responds.</p>

<p>Cash deals are usually the fastest. Because there is no mortgage underwriting, these deals can close in as little as <strong>7 to 30 days</strong>. Even then, they still need title work, transfer documents, and often an inspection period.</p>

<p>Mortgage deals usually take longer. A conventional loan often closes in <strong>30 to 45 days</strong>. FHA and VA loans often take <strong>45 to 60 days</strong>, and sometimes a little longer, because they may require extra underwriting steps, property checks, and stricter documentation.</p>

<p>Here is a simple view of the average timeline:</p>

<table>

<thead>

<tr>

<th>Deal Type</th>

<th>Average Timeline</th>

<th>Key Delays</th>

</tr>

</thead>

<tbody>

<tr>

<td>Cash Purchase</td>

<td>7–30 days</td>

<td>Title issues, document coordination</td>

</tr>

<tr>

<td>Conventional Loan</td>

<td>30–45 days</td>

<td>Appraisal, underwriting, credit review</td>

</tr>

<tr>

<td>FHA/VA Loan</td>

<td>45–60 days</td>

<td>Government-backed underwriting, property conditions</td>

</tr>

</tbody>

</table>

<p>Several moving parts shape the timeline.</p>

<p>The <strong>inspection period</strong> often takes about a week, though repair negotiations can stretch it. The <strong>appraisal</strong> can take 1 to 3 weeks depending on the lender and local demand. The <strong>title search</strong> may take 1 to 2 weeks, but longer if there are liens, name mistakes, missing releases, or ownership disputes. On top of that, your lender may ask for updated pay stubs, bank statements, tax returns, or proof that large deposits in your account are legitimate.</p>

<p>This is why a closing date is not just a date on paper. It is a target built on many steps happening on time.</p>

<p>If everything runs smoothly, the process feels simple. But if even one piece slows down, the entire timeline shifts. A delayed appraisal can hold up underwriting. A title issue can stop the lender from giving final approval. A repair request can push back the final walk-through.</p>

<p>So, <strong>how long can you delay closing on a <a href="https://comeawayhome.co.uk/taxes-on-selling-a-house/">house</a></strong> under a normal transaction timeline? In many cases, the first delay is minor, often <strong>a few days to two weeks</strong>. That kind of extension is common when the issue is paperwork, scheduling, or one unresolved condition. Bigger delays usually happen when financing, repairs, or title problems take more time than expected.</p>

<p>The key thing for you to remember is this: <strong>a standard closing window already has pressure built into it</strong>. That is why smart buyers and sellers do not wait until the last minute to solve problems.</p>

<h4 id="regional-variations-in-closing-delays">Regional Variations in Closing Delays</h4>

<p>Not every market moves at the same speed.</p>

<p>In some U.S. states, closings happen relatively fast because local systems are efficient, title companies are used to high volume, and agents push hard to keep timelines tight. In other places, delays are more common because of court-related procedures, local filing backlogs, insurance challenges, or slow municipal responses.</p>

<p>For example, some fast-moving markets can often close in about <strong>30 days</strong>, especially when buyers are pre-approved and title work starts immediately. In more complicated markets, closing may lean closer to <strong>45 to 60 days</strong> even when no one is doing anything wrong. Local norms matter.</p>

<p>There are also differences in how title companies, escrow agents, and attorneys handle the process. In some areas, the file moves mostly through an escrow or title office. In others, attorneys control large parts of the closing process. That changes the pace.</p>

<p>Outside the U.S., timelines can be even longer. In some countries, registry systems, land record verification, tax clearances, and transfer approvals add weeks or months to the process. In cities where development authorities or land offices handle parts of the transfer, a closing can stretch to <strong>60 to 90 days or more</strong>.</p>

<p>That matters if you are an investor, a business owner, or someone flipping property. A delay is not just an inconvenience. It affects carrying costs, contractor schedules, resale timing, and expected profit. If you planned to close, renovate, and relist within a certain quarter, even a short delay can shift your whole business plan.</p>

<p>So when you ask <strong>how long can you delay closing on a house</strong>, the real answer depends partly on your contract and partly on <strong>where the property is located</strong>. A five-day delay in one market may seem minor. In another market, it may signal a bigger problem that could take weeks to fix.</p>

<h2 id="legal-limits-on-delays">Legal Limits on Delays</h2>

<h4 id="how-long-can-you-delay-closing-on-a-house-legally-">How Long Can You Delay Closing on a House Legally?</h4>

<p>This is the part many people misunderstand.</p>

<p>There is <strong>no single legal rule</strong> that says every buyer or seller gets a certain number of extra days. The real answer is usually found in the <strong>purchase agreement</strong>. That contract controls the timeline, the contingency deadlines, the remedies, and what happens if one side cannot close on time.</p>

<p>In many real estate contracts, the original closing date is firm, but extensions are possible if both parties agree in writing. A common extension length is <strong>10 to 30 days</strong>. In some cases, the contract itself allows one or two short extensions under specific conditions. In other cases, there is no automatic extension at all.</p>

<p>This is where contract language matters.</p>

<p>If your agreement includes a <strong>“time is of the essence”</strong> clause, the closing date becomes much more important. That phrase means deadlines are strict. If one side misses the date without a valid excuse or signed extension, the other side may have the right to cancel the deal, keep the earnest money, or pursue damages depending on the contract and local law.</p>

<p>Contingencies also play a major role.</p>

<p>A financing contingency may give the buyer a set number of days to secure final loan approval. An inspection contingency may allow a certain window to request repairs or walk away. An appraisal contingency may protect the buyer if the home value comes in low. These timelines matter because they can create room for delay, but only within the limits written into the deal.</p>

<p>If those deadlines pass and no extension is signed, the buyer may lose important protections.</p>

<p>That is why the best answer to <strong>how long can you delay closing on a house legally</strong> is this: <strong>you can usually delay as long as the contract allows, or as long as the other side agrees in writing</strong>. In practice, that often means <strong>up to 30 days</strong>, though some deals go beyond that when the parties are motivated to keep the transaction alive.</p>

<p>Beyond a certain point, the risk rises fast.</p>

<p>A long delay can trigger claims of breach of contract. The seller may threaten to relist the property. The buyer may lose a rate lock. Earnest money may be at risk if the buyer no longer has a valid contingency to protect them. Some contracts include liquidated damages language, which means the buyer’s deposit may serve as the seller’s agreed remedy if the buyer defaults.</p>

<p>That does not mean every missed date leads to disaster.</p>

<p>Real estate deals are negotiated deals. If both sides still want the transaction to close, they often sign an addendum and move forward. But the key phrase there is <strong>“sign an addendum.”</strong> Verbal promises, text messages, and vague assumptions are not enough. If the closing date changes, it should be documented clearly.</p>

<p>You should also know that lenders, title companies, and insurers may need the updated date too. A contract extension by itself does not automatically fix every other part of the transaction. You may also need updated loan documents, revised disclosures, or extended insurance coverage dates.</p>

<p>So if you are wondering how long you can push the closing back, do not rely on guesswork. <strong>Read the contract, check the contingency deadlines, and get every extension in writing.</strong></p>

<h4 id="seller-s-rights-vs-buyer-s-rights">Seller’s Rights vs. Buyer’s Rights</h4>

<p>Both sides have rights, but those rights are not identical.</p>

<p>A <strong>seller</strong> usually has the right to expect performance by the closing date. If the buyer misses that date without a valid contingency or signed extension, the seller may be able to cancel the contract and keep the earnest money, depending on the agreement. In some cases, the seller can also issue a formal notice to perform, giving the buyer a final short period to close.</p>

<p>A <strong>buyer</strong>, on the other hand, may have more flexibility if the contract includes financing, appraisal, title, or inspection contingencies that have not expired. Those protections can buy time. For example, a financing contingency may effectively allow a buyer to delay closing while the lender completes its work, especially if the buyer has acted in good faith and met document requests on time.</p>

<p>Still, buyers do not have unlimited freedom.</p>

<p>If the buyer caused the delay by failing to provide documents, changing jobs, making a major purchase, or missing lender deadlines, the seller may push back hard. Sellers may agree to an extension, but they often want something in return. That could mean a higher deposit, a per diem fee, or reduced negotiation power on repairs.</p>

<p>Sellers can face delays too. If the seller cannot provide clear title, finish agreed repairs, or vacate on time, the buyer may have the right to delay closing, demand performance, or even cancel in serious cases.</p>

<p>This matters more in changing markets. In a buyer-friendly market, sellers may be more willing to grant extra time because they do not want to start over. In a strong seller’s market, they may be less patient. During periods of rising rates, many buyers ask for extensions because monthly payments change quickly. During slower periods, sellers often work harder to keep existing deals together.</p>

<p>The practical lesson is simple: <strong>rights come from the contract, but leverage comes from the market.</strong> If you understand both, you can negotiate a better outcome.</p>

<h2 id="common-reasons-for-closing-delays">Common Reasons for Closing Delays</h2>

<p><img class="aligncenter wp-image-6913 size-full" src="https://comeawayhome.co.uk/wp-content/uploads/2026/05/d6a6a74a-5c17-4120-9322-a67498c5367dS-ezgif.com-jpg-to-webp-converter.webp" alt="how long can you delay closing on a house" width="700" height="700" /></p>

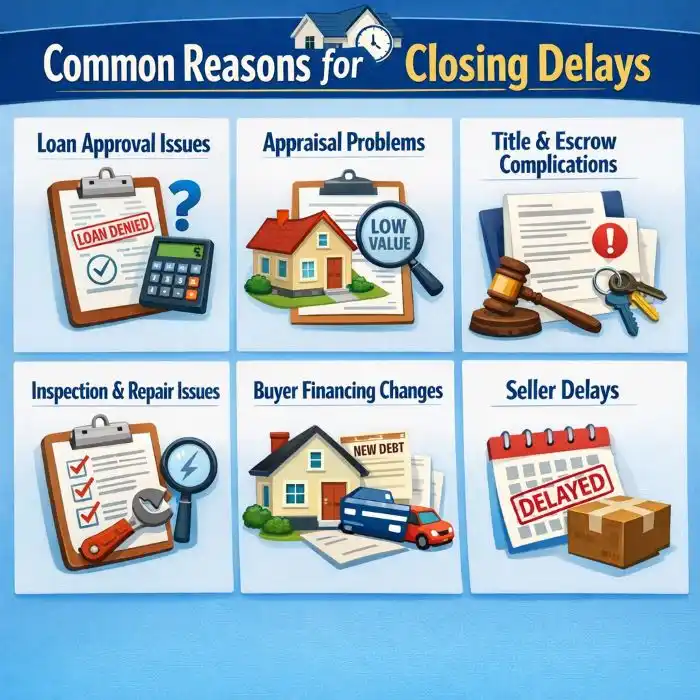

<h4 id="top-7-reasons-buyers-delay-closing">Top 7 Reasons Buyers Delay Closing</h4>

<p>Most delays happen for predictable reasons. If you know them in advance, you can often prevent them.</p>

<ol>

<li><strong>Financing problems</strong><br />

This is the biggest reason closings get pushed back. The lender may ask for updated income records, explanations for bank deposits, proof of assets, or corrected paperwork. Sometimes the buyer changes jobs, opens a new credit account, or makes a large purchase before closing. That can force the lender to re-check the file. If the issue is serious, final approval gets delayed.</li>

<li><strong>Appraisal comes in low</strong><br />

If the appraised value is below the purchase price, the lender may refuse to finance the full amount. Then the buyer and seller have to renegotiate. The buyer may need more cash, the seller may lower the price, or both sides may challenge the appraisal. All of that takes time.</li>

<li><strong>Inspection repairs take longer than expected</strong><br />

A home inspection may uncover roof damage, plumbing leaks, electrical issues, foundation cracks, or mold concerns. If the seller agrees to make repairs, contractors must be scheduled, work must be completed, and receipts may need to be provided before closing. That can add days or weeks.</li>

<li><strong>Title problems</strong><br />

Unpaid liens, missing signatures, old mortgages that were never properly released, boundary disputes, or probate issues can block closing. Title issues are often fixable, but some take time to research and clear.</li>

<li><strong>Insurance or HOA issues</strong><br />

In some areas, insurance has become harder to secure quickly, especially for older homes or high-risk locations. HOA documents can also slow the process if disclosures, fees, approvals, or resale certificates are delayed.</li>

<li><strong>Buyer life changes</strong><br />

Job loss, relocation problems, divorce, illness, or a moving schedule that falls apart can all cause a buyer to ask for more time. Even if the contract does not excuse the delay automatically, these events are common in real life.</li>

<li><strong>Document and communication breakdowns</strong><br />

Sometimes the delay is not dramatic at all. It is just slow responses. One missing bank statement, one unsigned form, one late payoff letter, or one person ignoring email for three days can push the closing date back.</li>

</ol>

<p>A very common question is: <strong>how long can you delay closing on a house for financing?</strong></p>

<p>In many cases, financing-related extensions last <strong>7 to 21 days</strong>, though some can run longer if underwriting is close to final approval and the seller believes the deal will still close. If the buyer is making steady progress and the lender confirms the file is active, sellers are often willing to allow a short extension. If the financing looks shaky, sellers become much less patient.</p>

<p>The biggest mistake buyers make is waiting too long to speak up.</p>

<p>If you know financing is slipping, tell your lender and your agent immediately. Waiting until the day before closing makes the problem harder to solve and weakens your negotiating position.</p>

<h4 id="seller-initiated-delays">Seller-Initiated Delays</h4>

<p>Buyers are not the only ones who delay closings.</p>

<p>Sellers often ask for more time because their next home is not ready, their movers are delayed, a repair is unfinished, or they need extra time to clear the property. This is especially common when the seller is buying and selling at the same time.</p>

<p>One common issue is the <strong>double closing problem</strong>. The seller plans to use money from the current sale to buy the next home. If that next transaction gets delayed, the seller may ask to push back your closing too.</p>

<p>New construction can create another seller-side delay. If a seller is moving into a newly built home, weather, permits, labor shortages, or inspection sign-offs may postpone their move-in date.</p>

<p>When that happens, buyers have a few choices. They can agree to a short extension, ask for compensation, or explore alternatives like a <strong>post-closing occupancy agreement</strong>, often called a rent-back. That allows the sale to close on time while the seller remains in the home for a limited period, often <strong>30 to 60 days</strong>.</p>

<p>This can be a smart compromise when the paperwork is ready but the move-out schedule is not.</p>

<h2 id="costs-and-penalties-of-delays">Costs and Penalties of Delays</h2>

<h4 id="financial-impact-fees-carry-costs-and-lost-time">Financial Impact: Fees, Carry Costs, and Lost Time</h4>

<p>A delayed closing is not just a scheduling issue. It can be expensive.</p>

<p>For buyers, the first cost may be a <strong>rate lock extension</strong>. If your mortgage rate was locked for a set period and closing moves beyond that date, the lender may charge a fee. Buyers may also face extra rent, temporary storage, hotel costs, utility overlap, or per diem charges negotiated with the seller.</p>

<p>For sellers, the costs can be even larger. A seller may keep paying a mortgage, taxes, insurance, utilities, HOA dues, and maintenance expenses while waiting for closing. If they already planned a move, they might also pay storage or temporary housing costs.</p>

<p>Here is a simple estimate of how delay costs can grow:</p>

<table>

<thead>

<tr>

<th>Delay Length</th>

<th>Buyer Cost Estimate</th>

<th>Seller Cost Estimate</th>

</tr>

</thead>

<tbody>

<tr>

<td>1–2 weeks</td>

<td>$700–$2,800</td>

<td>$1,000–$4,000</td>

</tr>

<tr>

<td>30+ days</td>

<td>$5,000+</td>

<td>$10,000+</td>

</tr>

</tbody>

</table>

<p>Those numbers vary by price range, market, and financing terms, but the point is clear: <strong>time costs money</strong>.</p>

<p>Some common delay-related expenses include:</p>

<ul>

<li><strong>Rate lock extension fees</strong></li>

<li><strong>Per diem interest or lender charges</strong></li>

<li><strong>Extra rent or mortgage overlap</strong></li>

<li><strong>Storage and moving rescheduling</strong></li>

<li><strong>Additional utility, tax, and insurance payments</strong></li>

<li><strong>Legal review or addendum preparation</strong></li>

<li><strong>Lost opportunity cost</strong></li>

</ul>

<p>That last one is easy to miss.</p>

<p>If you are a seller and market conditions improve, a delay might not look terrible at first. But if prices soften, rates rise, or your replacement property becomes unavailable, the delay can hurt you financially. If you are an investor, every extra week eats into your margin.</p>

<p>There is also the cost of uncertainty.</p>

<p>A delayed closing can keep your cash tied up. It can postpone renovations, move-ins, lease start dates, or business plans. Even when a deal eventually closes, the delay may still leave both sides feeling frustrated and financially stretched.</p>

<h2 id="how-to-request-a-closing-extension">How to Request a Closing Extension</h2>

<h4 id="step-by-step-guide-to-extend-closing">Step-by-Step Guide to Extend Closing</h4>

<p>If you need extra time, do not panic. Handle it early and professionally.</p>

<p>Here is the best way to request a closing extension:</p>

<ol>

<li><strong>Review the contract immediately</strong><br />

Check the closing date, contingency deadlines, default terms, and any clause dealing with extensions. You need to know whether you still have contractual protection or whether you are asking for a favor.</li>

<li><strong>Notify your agent and the other side in writing</strong><br />

Do this as soon as the delay becomes likely. Do not wait for the deadline. A simple written notice should explain the reason for the delay, the number of extra days requested, and the steps already being taken to resolve the issue.</li>

<li><strong>Provide evidence when possible</strong><br />

If the delay is financing-related, a lender update helps. If repairs are the issue, share contractor scheduling details. If title work is delayed, ask the title company for a written status note. The other side is more likely to cooperate when the problem is specific and documented.</li>

<li><strong>Offer a reasonable concession if needed</strong><br />

Sometimes an extension is granted more easily when you offer something in return. That might be a higher earnest money deposit, a per diem payment, a shortened inspection negotiation period, or flexibility on possession timing.</li>

<li><strong>Get the extension signed by all parties</strong><br />

The new date should be placed in a formal addendum. Make sure the lender, escrow officer, title company, and anyone else involved has the updated timeline too.</li>

</ol>

<p>Timing matters here.</p>

<p>The best time to ask is usually <strong>10 to 14 days before closing</strong>, or the moment you know the deal may not close on time. If you wait until the final day, the other side may assume the transaction is unstable and refuse.</p>

<p>A simple extension request can sound like this in plain language:</p>

<p><strong>“We are requesting a 10-day extension to complete final loan approval. The lender has confirmed the file is in process and only updated employment verification remains. We remain committed to closing and are prepared to sign an addendum immediately.”</strong></p>

<p>That kind of message is calm, clear, and solution-focused.</p>

<p>In many cases, extensions succeed because the parties still want the same thing: <strong>to close the deal</strong>. Good communication often matters as much as the actual reason for the delay.</p>

<h4 id="negotiation-tactics-that-improve-your-chances">Negotiation Tactics That Improve Your Chances</h4>

<p>If you need an extension, do not just ask for time. Build a case.</p>

<p>Be specific. Asking for “a little more time” sounds vague and risky. Asking for <strong>seven extra days to clear title</strong> sounds manageable.</p>

<p>Keep your request realistic. If the issue will take three weeks, do not ask for three days and then come back again. Repeated short extensions can wear out goodwill.</p>

<p>Understand market leverage. In a slower market, sellers may work harder to keep a committed buyer. In a hot market, they may be more likely to move on if they think another buyer is available.</p>

<p>Most importantly, show progress. If you can prove the deal is still alive and close to completion, the other side is far more likely to cooperate.</p>

<h2 id="alternatives-to-delaying-closing">Alternatives to Delaying Closing</h2>

<h4 id="5-smart-workarounds-when-a-full-delay-is-not-ideal">5 Smart Workarounds When a Full Delay Is Not Ideal</h4>

<p>Sometimes the best answer is not to delay the closing at all.</p>

<p>A <strong>rent-back agreement</strong> can help when the seller needs extra time in the property after closing. The sale closes on schedule, but the seller stays for a short period and pays rent or occupancy fees based on the agreement.</p>

<p>A <strong>bridge loan</strong> can help a seller or buyer who needs temporary funds to move forward without waiting on the full transaction chain to line up perfectly. It is not right for everyone, but it can solve timing problems.</p>

<p>A <strong>postponed possession agreement</strong> works when ownership transfers on time, but the physical move-in happens later. This is similar to a rent-back in some deals, though the exact structure varies.</p>

<p>An <strong>assignment or substitute transaction structure</strong> may help investors in certain deals, especially when timing around closing and resale is tight. This only works in specific contract situations, and legal review is wise.</p>

<p>A <strong>reworked earnest money or contingency schedule</strong> can also save the deal. Instead of moving the entire closing date far into the future, the parties may adjust one key timeline to give the transaction room to breathe.</p>

<p>These options can preserve momentum, reduce conflict, and limit carrying costs. If a full extension creates too much risk, think creatively. There is often more than one way to solve a timing problem.</p>

<h2 id="expert-tips-to-avoid-delays">Expert Tips to Avoid Delays</h2>

<h4 id="preventive-strategies-for-a-smooth-closing">Preventive Strategies for a Smooth Closing</h4>

<p>The best delay is the one that never happens.</p>

<p>If you are a buyer, get <strong>fully pre-approved</strong>, not just casually pre-qualified. Submit your documents early. Respond to lender requests the same day if possible. Avoid opening new credit accounts or making big purchases before closing.</p>

<p>If you are a seller, order documents early, disclose issues honestly, and handle known title or repair problems before listing if you can. If you know your move-out plan is tight, discuss that upfront instead of surprising the buyer later.</p>

<p>For both sides, choose professionals who communicate well. A responsive lender, careful agent, organized title company, and proactive attorney can save you days or weeks.</p>

<p>Give yourself buffer time too.</p>

<p>If your ideal move requires a certain date, try not to build your whole life around the exact closing day. Add breathing room for movers, utility transfers, school schedules, or contractor starts. In real estate, a small buffer protects your sanity.</p>

<p>If you are an investor or business owner, build delays into your numbers. A flip that only works if everything happens perfectly is a risky deal. Add margin for financing hiccups, repair negotiations, and title problems.</p>

<p>The smoother your preparation, the less likely you are to ask, <strong>how long can you delay closing on a house</strong>, because you may not need to delay it at all.</p>

<h2 id="faqs-how-long-can-you-delay-closing-on-a-house-">FAQs: How Long Can You Delay Closing on a House?</h2>

<h4 id="1-how-long-can-you-delay-closing-on-a-house-with-a-contingency-">1. How long can you delay closing on a house with a contingency?</h4>

<p>Usually <strong>21 to 45 days</strong>, depending on the type of contingency and the exact contract deadlines. The protection only lasts as long as the contingency remains active.</p>

<h4 id="2-can-a-seller-refuse-to-extend-the-closing-date-">2. Can a seller refuse to extend the closing date?</h4>

<p>Yes. Unless the contract gives you an automatic right to extend, the seller can refuse.</p>

<h4 id="3-can-a-buyer-lose-earnest-money-because-of-a-delay-">3. Can a buyer lose earnest money because of a delay?</h4>

<p>Yes. If the buyer misses the closing date without valid contractual protection, the earnest money may be at risk.</p>

<h4 id="4-how-long-can-you-delay-closing-on-a-house-for-financing-">4. How long can you delay closing on a house for financing?</h4>

<p>Often <strong>7 to 21 days</strong>, sometimes longer if the seller believes approval is close and the extension is documented.</p>

<h4 id="5-what-if-the-appraisal-delays-closing-">5. What if the appraisal delays closing?</h4>

<p>The parties can extend the closing date, renegotiate the price, challenge the appraisal, or end the deal if the contract allows.</p>

<h4 id="6-can-sellers-charge-per-diem-for-a-delay-">6. Can sellers charge per diem for a delay?</h4>

<p>Yes. A daily fee can be negotiated as part of an extension.</p>

<h4 id="7-what-happens-if-title-issues-are-found-">7. What happens if title issues are found?</h4>

<p>Closing usually pauses until the issue is cleared, waived, or otherwise resolved.</p>

<h4 id="8-can-you-move-the-possession-date-without-moving-closing-">8. Can you move the possession date without moving closing?</h4>

<p>Yes. A rent-back or delayed possession agreement can do that.</p>

<h4 id="9-is-a-verbal-extension-enough-">9. Is a verbal extension enough?</h4>

<p>No. You should always get the extension in writing and signed.</p>

<h4 id="10-should-you-talk-to-a-real-estate-attorney-">10. Should you talk to a real estate attorney?</h4>

<p>If the delay is serious, the contract is strict, or large money is involved, <strong>yes</strong>. It is a smart step.</p>

<h2 id="conclusion">Conclusion</h2>

<p>So, <strong>how long can you delay closing on a house</strong>?</p>

<p>In most cases, <strong>10 to 30 days is common</strong>, and some deals stretch longer when both sides agree and the problem is being actively solved. But there is no universal deadline that applies to every transaction. The contract, the contingencies, the local market, and the reason for the delay all matter.</p>

<p>If you need more time, act early, communicate clearly, and get everything in writing. If you want to avoid delays altogether, prepare your financing, paperwork, repairs, and move-out plan before the pressure builds.</p>

<p>A delayed closing does not always kill a deal. But the longer it drags on, the more the risks and costs grow. If your transaction is getting complicated, speak with your agent, lender, title company, or a real estate attorney right away.</p>

<p><a href="https://comeawayhome.co.uk/">House</a></p>

You sign the papers, move the money, get the keys, and finally move on with your life. But real estate deals do not always move in a straight line. A buyer may find a major repair issue during inspection. A lender may need more documents. A title problem may show up at the last minute. A seller may need extra time because their next home is not ready yet.

That is why so many buyers and sellers ask the same question: how long can you delay closing on a house without putting the deal at risk?

The short answer is this: most delays are possible for 10 to 30 days, and sometimes longer, but only if the contract allows it or both sides agree in writing. In many markets, roughly 10% to 15% of home sales do not close on the original date. Some are fixed in a few days. Others turn into longer extensions that cost money, create stress, and sometimes cause the deal to fall apart.

If you are buying, selling, or investing, you need to know what is normal, what is risky, and what you can do before the closing date slips away. That is especially important in 2026, when lending standards, insurance issues, and repair negotiations can still slow deals down.

In this guide, you will learn the usual closing timelines, the legal rules behind delays, the most common reasons closings get pushed back, the real costs of waiting, and the smartest ways to ask for more time without losing leverage. You will also see practical alternatives that can save the deal when a full delay is not the best option.

Standard Closing Timeline

What Is the Typical Closing Period?

Before you can understand a delay, you need to understand what a normal closing timeline looks like.

In most home sales, the closing period begins once the seller accepts the offer. From there, both sides work through inspections, financing, title work, paperwork, insurance, and final approval. The exact timeline depends on the deal type, the lender, the market, and how quickly everyone responds.

Cash deals are usually the fastest. Because there is no mortgage underwriting, these deals can close in as little as 7 to 30 days. Even then, they still need title work, transfer documents, and often an inspection period.

Mortgage deals usually take longer. A conventional loan often closes in 30 to 45 days. FHA and VA loans often take 45 to 60 days, and sometimes a little longer, because they may require extra underwriting steps, property checks, and stricter documentation.

Here is a simple view of the average timeline:

| Deal Type |

Average Timeline |

Key Delays |

| Cash Purchase |

7–30 days |

Title issues, document coordination |

| Conventional Loan |

30–45 days |

Appraisal, underwriting, credit review |

| FHA/VA Loan |

45–60 days |

Government-backed underwriting, property conditions |

Several moving parts shape the timeline.

The inspection period often takes about a week, though repair negotiations can stretch it. The appraisal can take 1 to 3 weeks depending on the lender and local demand. The title search may take 1 to 2 weeks, but longer if there are liens, name mistakes, missing releases, or ownership disputes. On top of that, your lender may ask for updated pay stubs, bank statements, tax returns, or proof that large deposits in your account are legitimate.

This is why a closing date is not just a date on paper. It is a target built on many steps happening on time.

If everything runs smoothly, the process feels simple. But if even one piece slows down, the entire timeline shifts. A delayed appraisal can hold up underwriting. A title issue can stop the lender from giving final approval. A repair request can push back the final walk-through.

So, how long can you delay closing on a house under a normal transaction timeline? In many cases, the first delay is minor, often a few days to two weeks. That kind of extension is common when the issue is paperwork, scheduling, or one unresolved condition. Bigger delays usually happen when financing, repairs, or title problems take more time than expected.

The key thing for you to remember is this: a standard closing window already has pressure built into it. That is why smart buyers and sellers do not wait until the last minute to solve problems.

Regional Variations in Closing Delays

Not every market moves at the same speed.

In some U.S. states, closings happen relatively fast because local systems are efficient, title companies are used to high volume, and agents push hard to keep timelines tight. In other places, delays are more common because of court-related procedures, local filing backlogs, insurance challenges, or slow municipal responses.

For example, some fast-moving markets can often close in about 30 days, especially when buyers are pre-approved and title work starts immediately. In more complicated markets, closing may lean closer to 45 to 60 days even when no one is doing anything wrong. Local norms matter.

There are also differences in how title companies, escrow agents, and attorneys handle the process. In some areas, the file moves mostly through an escrow or title office. In others, attorneys control large parts of the closing process. That changes the pace.

Outside the U.S., timelines can be even longer. In some countries, registry systems, land record verification, tax clearances, and transfer approvals add weeks or months to the process. In cities where development authorities or land offices handle parts of the transfer, a closing can stretch to 60 to 90 days or more.

That matters if you are an investor, a business owner, or someone flipping property. A delay is not just an inconvenience. It affects carrying costs, contractor schedules, resale timing, and expected profit. If you planned to close, renovate, and relist within a certain quarter, even a short delay can shift your whole business plan.

So when you ask how long can you delay closing on a house, the real answer depends partly on your contract and partly on where the property is located. A five-day delay in one market may seem minor. In another market, it may signal a bigger problem that could take weeks to fix.

Legal Limits on Delays

How Long Can You Delay Closing on a House Legally?

This is the part many people misunderstand.

There is no single legal rule that says every buyer or seller gets a certain number of extra days. The real answer is usually found in the purchase agreement. That contract controls the timeline, the contingency deadlines, the remedies, and what happens if one side cannot close on time.

In many real estate contracts, the original closing date is firm, but extensions are possible if both parties agree in writing. A common extension length is 10 to 30 days. In some cases, the contract itself allows one or two short extensions under specific conditions. In other cases, there is no automatic extension at all.

This is where contract language matters.

If your agreement includes a “time is of the essence” clause, the closing date becomes much more important. That phrase means deadlines are strict. If one side misses the date without a valid excuse or signed extension, the other side may have the right to cancel the deal, keep the earnest money, or pursue damages depending on the contract and local law.

Contingencies also play a major role.

A financing contingency may give the buyer a set number of days to secure final loan approval. An inspection contingency may allow a certain window to request repairs or walk away. An appraisal contingency may protect the buyer if the home value comes in low. These timelines matter because they can create room for delay, but only within the limits written into the deal.

If those deadlines pass and no extension is signed, the buyer may lose important protections.

That is why the best answer to how long can you delay closing on a house legally is this: you can usually delay as long as the contract allows, or as long as the other side agrees in writing. In practice, that often means up to 30 days, though some deals go beyond that when the parties are motivated to keep the transaction alive.

Beyond a certain point, the risk rises fast.

A long delay can trigger claims of breach of contract. The seller may threaten to relist the property. The buyer may lose a rate lock. Earnest money may be at risk if the buyer no longer has a valid contingency to protect them. Some contracts include liquidated damages language, which means the buyer’s deposit may serve as the seller’s agreed remedy if the buyer defaults.

That does not mean every missed date leads to disaster.

Real estate deals are negotiated deals. If both sides still want the transaction to close, they often sign an addendum and move forward. But the key phrase there is “sign an addendum.” Verbal promises, text messages, and vague assumptions are not enough. If the closing date changes, it should be documented clearly.

You should also know that lenders, title companies, and insurers may need the updated date too. A contract extension by itself does not automatically fix every other part of the transaction. You may also need updated loan documents, revised disclosures, or extended insurance coverage dates.

So if you are wondering how long you can push the closing back, do not rely on guesswork. Read the contract, check the contingency deadlines, and get every extension in writing.

Seller’s Rights vs. Buyer’s Rights

Both sides have rights, but those rights are not identical.

A seller usually has the right to expect performance by the closing date. If the buyer misses that date without a valid contingency or signed extension, the seller may be able to cancel the contract and keep the earnest money, depending on the agreement. In some cases, the seller can also issue a formal notice to perform, giving the buyer a final short period to close.

A buyer, on the other hand, may have more flexibility if the contract includes financing, appraisal, title, or inspection contingencies that have not expired. Those protections can buy time. For example, a financing contingency may effectively allow a buyer to delay closing while the lender completes its work, especially if the buyer has acted in good faith and met document requests on time.

Still, buyers do not have unlimited freedom.

If the buyer caused the delay by failing to provide documents, changing jobs, making a major purchase, or missing lender deadlines, the seller may push back hard. Sellers may agree to an extension, but they often want something in return. That could mean a higher deposit, a per diem fee, or reduced negotiation power on repairs.

Sellers can face delays too. If the seller cannot provide clear title, finish agreed repairs, or vacate on time, the buyer may have the right to delay closing, demand performance, or even cancel in serious cases.

This matters more in changing markets. In a buyer-friendly market, sellers may be more willing to grant extra time because they do not want to start over. In a strong seller’s market, they may be less patient. During periods of rising rates, many buyers ask for extensions because monthly payments change quickly. During slower periods, sellers often work harder to keep existing deals together.

The practical lesson is simple: rights come from the contract, but leverage comes from the market. If you understand both, you can negotiate a better outcome.

Common Reasons for Closing Delays

Top 7 Reasons Buyers Delay Closing

Most delays happen for predictable reasons. If you know them in advance, you can often prevent them.

- Financing problems

This is the biggest reason closings get pushed back. The lender may ask for updated income records, explanations for bank deposits, proof of assets, or corrected paperwork. Sometimes the buyer changes jobs, opens a new credit account, or makes a large purchase before closing. That can force the lender to re-check the file. If the issue is serious, final approval gets delayed.

- Appraisal comes in low

If the appraised value is below the purchase price, the lender may refuse to finance the full amount. Then the buyer and seller have to renegotiate. The buyer may need more cash, the seller may lower the price, or both sides may challenge the appraisal. All of that takes time.

- Inspection repairs take longer than expected

A home inspection may uncover roof damage, plumbing leaks, electrical issues, foundation cracks, or mold concerns. If the seller agrees to make repairs, contractors must be scheduled, work must be completed, and receipts may need to be provided before closing. That can add days or weeks.

- Title problems

Unpaid liens, missing signatures, old mortgages that were never properly released, boundary disputes, or probate issues can block closing. Title issues are often fixable, but some take time to research and clear.

- Insurance or HOA issues

In some areas, insurance has become harder to secure quickly, especially for older homes or high-risk locations. HOA documents can also slow the process if disclosures, fees, approvals, or resale certificates are delayed.

- Buyer life changes

Job loss, relocation problems, divorce, illness, or a moving schedule that falls apart can all cause a buyer to ask for more time. Even if the contract does not excuse the delay automatically, these events are common in real life.

- Document and communication breakdowns

Sometimes the delay is not dramatic at all. It is just slow responses. One missing bank statement, one unsigned form, one late payoff letter, or one person ignoring email for three days can push the closing date back.

A very common question is: how long can you delay closing on a house for financing?

In many cases, financing-related extensions last 7 to 21 days, though some can run longer if underwriting is close to final approval and the seller believes the deal will still close. If the buyer is making steady progress and the lender confirms the file is active, sellers are often willing to allow a short extension. If the financing looks shaky, sellers become much less patient.

The biggest mistake buyers make is waiting too long to speak up.

If you know financing is slipping, tell your lender and your agent immediately. Waiting until the day before closing makes the problem harder to solve and weakens your negotiating position.

Seller-Initiated Delays

Buyers are not the only ones who delay closings.

Sellers often ask for more time because their next home is not ready, their movers are delayed, a repair is unfinished, or they need extra time to clear the property. This is especially common when the seller is buying and selling at the same time.

One common issue is the double closing problem. The seller plans to use money from the current sale to buy the next home. If that next transaction gets delayed, the seller may ask to push back your closing too.

New construction can create another seller-side delay. If a seller is moving into a newly built home, weather, permits, labor shortages, or inspection sign-offs may postpone their move-in date.

When that happens, buyers have a few choices. They can agree to a short extension, ask for compensation, or explore alternatives like a post-closing occupancy agreement, often called a rent-back. That allows the sale to close on time while the seller remains in the home for a limited period, often 30 to 60 days.

This can be a smart compromise when the paperwork is ready but the move-out schedule is not.

Costs and Penalties of Delays

Financial Impact: Fees, Carry Costs, and Lost Time

A delayed closing is not just a scheduling issue. It can be expensive.

For buyers, the first cost may be a rate lock extension. If your mortgage rate was locked for a set period and closing moves beyond that date, the lender may charge a fee. Buyers may also face extra rent, temporary storage, hotel costs, utility overlap, or per diem charges negotiated with the seller.

For sellers, the costs can be even larger. A seller may keep paying a mortgage, taxes, insurance, utilities, HOA dues, and maintenance expenses while waiting for closing. If they already planned a move, they might also pay storage or temporary housing costs.

Here is a simple estimate of how delay costs can grow:

| Delay Length |

Buyer Cost Estimate |

Seller Cost Estimate |

| 1–2 weeks |

$700–$2,800 |

$1,000–$4,000 |

| 30+ days |

$5,000+ |

$10,000+ |

Those numbers vary by price range, market, and financing terms, but the point is clear: time costs money.

Some common delay-related expenses include:

- Rate lock extension fees

- Per diem interest or lender charges

- Extra rent or mortgage overlap

- Storage and moving rescheduling

- Additional utility, tax, and insurance payments

- Legal review or addendum preparation

- Lost opportunity cost

That last one is easy to miss.

If you are a seller and market conditions improve, a delay might not look terrible at first. But if prices soften, rates rise, or your replacement property becomes unavailable, the delay can hurt you financially. If you are an investor, every extra week eats into your margin.

There is also the cost of uncertainty.

A delayed closing can keep your cash tied up. It can postpone renovations, move-ins, lease start dates, or business plans. Even when a deal eventually closes, the delay may still leave both sides feeling frustrated and financially stretched.

How to Request a Closing Extension

Step-by-Step Guide to Extend Closing

If you need extra time, do not panic. Handle it early and professionally.

Here is the best way to request a closing extension:

- Review the contract immediately

Check the closing date, contingency deadlines, default terms, and any clause dealing with extensions. You need to know whether you still have contractual protection or whether you are asking for a favor.

- Notify your agent and the other side in writing

Do this as soon as the delay becomes likely. Do not wait for the deadline. A simple written notice should explain the reason for the delay, the number of extra days requested, and the steps already being taken to resolve the issue.

- Provide evidence when possible

If the delay is financing-related, a lender update helps. If repairs are the issue, share contractor scheduling details. If title work is delayed, ask the title company for a written status note. The other side is more likely to cooperate when the problem is specific and documented.

- Offer a reasonable concession if needed

Sometimes an extension is granted more easily when you offer something in return. That might be a higher earnest money deposit, a per diem payment, a shortened inspection negotiation period, or flexibility on possession timing.

- Get the extension signed by all parties

The new date should be placed in a formal addendum. Make sure the lender, escrow officer, title company, and anyone else involved has the updated timeline too.

Timing matters here.

The best time to ask is usually 10 to 14 days before closing, or the moment you know the deal may not close on time. If you wait until the final day, the other side may assume the transaction is unstable and refuse.

A simple extension request can sound like this in plain language:

“We are requesting a 10-day extension to complete final loan approval. The lender has confirmed the file is in process and only updated employment verification remains. We remain committed to closing and are prepared to sign an addendum immediately.”

That kind of message is calm, clear, and solution-focused.

In many cases, extensions succeed because the parties still want the same thing: to close the deal. Good communication often matters as much as the actual reason for the delay.

Negotiation Tactics That Improve Your Chances

If you need an extension, do not just ask for time. Build a case.

Be specific. Asking for “a little more time” sounds vague and risky. Asking for seven extra days to clear title sounds manageable.

Keep your request realistic. If the issue will take three weeks, do not ask for three days and then come back again. Repeated short extensions can wear out goodwill.

Understand market leverage. In a slower market, sellers may work harder to keep a committed buyer. In a hot market, they may be more likely to move on if they think another buyer is available.

Most importantly, show progress. If you can prove the deal is still alive and close to completion, the other side is far more likely to cooperate.

Alternatives to Delaying Closing

5 Smart Workarounds When a Full Delay Is Not Ideal

Sometimes the best answer is not to delay the closing at all.

A rent-back agreement can help when the seller needs extra time in the property after closing. The sale closes on schedule, but the seller stays for a short period and pays rent or occupancy fees based on the agreement.

A bridge loan can help a seller or buyer who needs temporary funds to move forward without waiting on the full transaction chain to line up perfectly. It is not right for everyone, but it can solve timing problems.

A postponed possession agreement works when ownership transfers on time, but the physical move-in happens later. This is similar to a rent-back in some deals, though the exact structure varies.

An assignment or substitute transaction structure may help investors in certain deals, especially when timing around closing and resale is tight. This only works in specific contract situations, and legal review is wise.

A reworked earnest money or contingency schedule can also save the deal. Instead of moving the entire closing date far into the future, the parties may adjust one key timeline to give the transaction room to breathe.

These options can preserve momentum, reduce conflict, and limit carrying costs. If a full extension creates too much risk, think creatively. There is often more than one way to solve a timing problem.

Expert Tips to Avoid Delays

Preventive Strategies for a Smooth Closing

The best delay is the one that never happens.

If you are a buyer, get fully pre-approved, not just casually pre-qualified. Submit your documents early. Respond to lender requests the same day if possible. Avoid opening new credit accounts or making big purchases before closing.

If you are a seller, order documents early, disclose issues honestly, and handle known title or repair problems before listing if you can. If you know your move-out plan is tight, discuss that upfront instead of surprising the buyer later.

For both sides, choose professionals who communicate well. A responsive lender, careful agent, organized title company, and proactive attorney can save you days or weeks.

Give yourself buffer time too.

If your ideal move requires a certain date, try not to build your whole life around the exact closing day. Add breathing room for movers, utility transfers, school schedules, or contractor starts. In real estate, a small buffer protects your sanity.

If you are an investor or business owner, build delays into your numbers. A flip that only works if everything happens perfectly is a risky deal. Add margin for financing hiccups, repair negotiations, and title problems.

The smoother your preparation, the less likely you are to ask, how long can you delay closing on a house, because you may not need to delay it at all.

FAQs: How Long Can You Delay Closing on a House?

1. How long can you delay closing on a house with a contingency?

Usually 21 to 45 days, depending on the type of contingency and the exact contract deadlines. The protection only lasts as long as the contingency remains active.

2. Can a seller refuse to extend the closing date?

Yes. Unless the contract gives you an automatic right to extend, the seller can refuse.

3. Can a buyer lose earnest money because of a delay?

Yes. If the buyer misses the closing date without valid contractual protection, the earnest money may be at risk.

4. How long can you delay closing on a house for financing?

Often 7 to 21 days, sometimes longer if the seller believes approval is close and the extension is documented.

5. What if the appraisal delays closing?

The parties can extend the closing date, renegotiate the price, challenge the appraisal, or end the deal if the contract allows.

6. Can sellers charge per diem for a delay?

Yes. A daily fee can be negotiated as part of an extension.

7. What happens if title issues are found?

Closing usually pauses until the issue is cleared, waived, or otherwise resolved.

8. Can you move the possession date without moving closing?

Yes. A rent-back or delayed possession agreement can do that.

9. Is a verbal extension enough?

No. You should always get the extension in writing and signed.

10. Should you talk to a real estate attorney?

If the delay is serious, the contract is strict, or large money is involved, yes. It is a smart step.

Conclusion

So, how long can you delay closing on a house?

In most cases, 10 to 30 days is common, and some deals stretch longer when both sides agree and the problem is being actively solved. But there is no universal deadline that applies to every transaction. The contract, the contingencies, the local market, and the reason for the delay all matter.

If you need more time, act early, communicate clearly, and get everything in writing. If you want to avoid delays altogether, prepare your financing, paperwork, repairs, and move-out plan before the pressure builds.

A delayed closing does not always kill a deal. But the longer it drags on, the more the risks and costs grow. If your transaction is getting complicated, speak with your agent, lender, title company, or a real estate attorney right away.

House