<p>You’ve found the house you love. Your offer is accepted. The excitement is real.</p>

<p>Then the next question hits you: <strong><a href="https://www.zillow.com/learn/how-long-does-it-take-to-close-on-a-house/">how long does it take to close on a house</a>?</strong></p>

<p>That’s the part many buyers underestimate. You might think once the seller says yes, the hard part is over. In reality, the closing period is where a lot of moving parts come together. The lender reviews your finances. The home gets inspected. The appraisal comes in. Title work gets checked. Legal paperwork gets prepared. Funds get transferred. And if even one piece slows down, the whole timeline can shift.</p>

<p>In most cases, <strong>the time to close on a house is around 30 to 45 days</strong>. But that does not mean every home purchase fits neatly into that window. Some cash deals can close in less than two weeks. Some financed purchases can stretch to 60 days or longer. New construction can take even more time depending on the builder, permits, and completion date.</p>

<p>That is why buyers often feel stressed during this stage. You may be trying to plan your move, lock in your rate, schedule utilities, and coordinate with your current lease or home sale. If the timeline changes, everything else can change with it.</p>

<p>The good news is that the closing process is much easier to manage when you understand what happens at each stage.</p>

<p>In this guide, you’ll learn <strong>how long does it take to close on a house</strong>, what happens from accepted offer to closing day, which delays are most common, and what you can do to keep the process moving.</p>

<h2 id="average-house-closing-timeline-what-most-buyers-should-expect">Average House Closing Timeline: What Most Buyers Should Expect</h2>

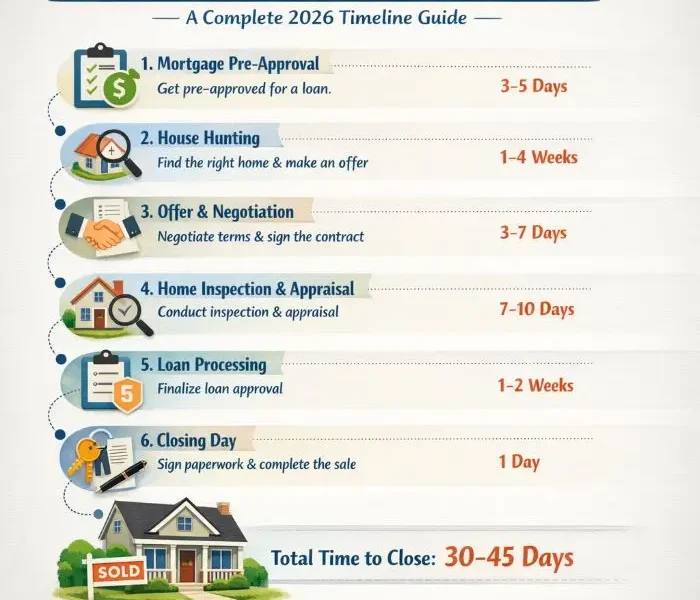

<p><img class="aligncenter wp-image-6950 size-full" src="https://comeawayhome.co.uk/wp-content/uploads/2026/05/749c7381-5db7-422f-b32e-41a1467533c5a-ezgif.com-jpg-to-webp-converter.webp" alt="how long does it take to close on a house" width="700" height="700" /></p>

<p>If you are asking <strong>how long does it take to close on a house</strong>, the short answer is this: <strong>most buyers close in 30 to 45 days</strong>.</p>

<p>That window is common for buyers using a mortgage. It gives enough time for the lender to process the loan, the home to be inspected and appraised, the title work to be completed, and all final paperwork to be prepared. In a normal market, that is the standard <a href="https://comeawayhome.co.uk/how-to-increase-water-pressure-in-house/">house</a> closing timeline many buyers experience.</p>

<p>But let’s make one thing clear. <strong>“Normal” does not always mean “guaranteed.”</strong> Some deals move faster. Others take longer. A simple purchase with a strong borrower, a responsive seller, and a clean property can close quickly. A deal with repair negotiations, title issues, or loan paperwork problems can take much longer.</p>

<p>Cash purchases are the biggest exception. Because there is no mortgage approval involved, buyers can often skip some of the longest parts of the timeline. That means a cash deal may close in <strong>as little as 4 to 10 days</strong>, depending on how quickly the title company, seller, and buyer complete their tasks.</p>

<p>On the other hand, government-backed loans, rural properties, condos with document issues, and new construction homes often take longer than the average time to close on a house. In those cases, the closing process may reach <strong>45 to 60 days or more</strong>.</p>

<p>To make this easier to follow, here is a simple overview.</p>

<table>

<thead>

<tr>

<th><strong>Phase</strong></th>

<th><strong>Typical Timeframe</strong></th>

<th><strong>What Happens</strong></th>

</tr>

</thead>

<tbody>

<tr>

<td>Offer Acceptance</td>

<td>1–3 days</td>

<td>Buyer and seller agree on price, terms, and target closing date</td>

</tr>

<tr>

<td>Inspection & Early Due Diligence</td>

<td>4–10 days</td>

<td>Home inspection is completed, issues are discovered, repair talks may begin</td>

</tr>

<tr>

<td>Appraisal & Loan Processing</td>

<td>11–25 days</td>

<td>Lender orders appraisal, reviews documents, and starts underwriting</td>

</tr>

<tr>

<td>Underwriting & Final Approval</td>

<td>26–40 days</td>

<td>Final checks on credit, income, assets, title, and conditions</td>

</tr>

<tr>

<td>Closing Preparation</td>

<td>41–45 days</td>

<td>Buyer receives closing disclosure, reviews numbers, and gets funds ready</td>

</tr>

<tr>

<td>Closing Day</td>

<td>Around Day 45</td>

<td>Final signing, wire transfer, deed recording, and key handoff</td>

</tr>

</tbody>

</table>

<p>[<strong>Timeline Infographic Placeholder</strong>]</p>

<p>A big reason the process takes this long is that several steps happen both <strong>one after another</strong> and <strong>at the same time</strong>. For example, while you’re booking the inspection, your lender may be collecting your pay stubs and bank statements. While the appraisal is being scheduled, the title company may be researching ownership records. While the underwriter reviews your loan, your agent may still be negotiating repairs.</p>

<p>So when people ask, <strong>how long does it take to close on a house</strong>, they are really asking how long it takes for all these pieces to line up.</p>

<p>A good way to think about it is this:</p>

<ul>

<li><strong>30 days</strong> is possible for a clean, well-prepared file</li>

<li><strong>45 days</strong> is common for a standard financed purchase</li>

<li><strong>60+ days</strong> can happen when problems or extra requirements show up</li>

</ul>

<p>If you are buying soon, it helps to build your moving plans around a little flexibility. A target closing date is important, but it is still a target. The smoother your financing, paperwork, and communication are, the better your chances of hitting it.</p>

<h2 id="step-by-step-closing-process-what-happens-after-your-offer-is-accepted">Step-by-Step Closing Process: What Happens After Your Offer Is Accepted</h2>

<p>Understanding the <strong>closing process steps</strong> makes the whole experience feel less confusing. Instead of thinking of closing as one giant waiting period, it helps to break it into stages.</p>

<p>Below is the full process, from accepted offer to getting your keys.</p>

<h3 id="step-1-offer-negotiation-and-acceptance">Offer Negotiation and Acceptance</h3>

<p>The closing timeline starts when the seller accepts your offer.</p>

<p>This first stage often takes <strong>1 to 3 days</strong>, though it can move faster or slower depending on how much back-and-forth happens. The buyer may make an offer, the seller may counter, and both sides may adjust the price, contingencies, closing date, seller credits, or included items like appliances.</p>

<p>This is also when the expected closing date is usually written into the contract.</p>

<p>That date matters more than many buyers realize. If you ask for a closing date that is too aggressive, you may create pressure before the lender and title company even begin. If you choose a date that is too far out, you may lose momentum and create extra waiting.</p>

<p>A practical move is to request <strong>about 45 days</strong> unless your lender clearly tells you they can close faster.</p>

<p>This stage may feel simple, but it shapes the rest of the house closing timeline. A strong offer with realistic terms can set the deal up for success. A messy contract with unclear repair expectations or tight deadlines can create problems later.</p>

<p><strong>Pro tip:</strong> before you submit the offer, talk to your lender and your real estate agent together. That way, the closing date in the contract matches what is actually realistic.</p>

<h3 id="step-2-open-escrow-and-deposit-earnest-money">Open Escrow and Deposit Earnest Money</h3>

<p>Once the offer is accepted, the transaction usually enters <strong>escrow</strong>.</p>

<p>Escrow is a neutral process where money and documents are held safely until all contract terms are met. This protects both buyer and seller. The buyer typically sends earnest money, sometimes called a good-faith deposit, to the escrow or title company within a few days of the contract being signed.</p>

<p>This part often happens right away, usually in the first <strong>1 to 5 days</strong> after acceptance.</p>

<p>It may sound like a small step, but it is important. If the earnest money deposit is late, that can trigger problems early in the process. It may even put the contract at risk in some cases.</p>

<p>Escrow also becomes the central place where important documents, title work, and closing instructions begin to come together. Think of it as the hub that keeps the deal organized.</p>

<h3 id="step-3-schedule-the-home-inspection">Schedule the Home Inspection</h3>

<p>One of the most important answers to <strong>how long does it take to close on a house</strong> comes from what happens during the inspection period.</p>

<p>The home inspection usually takes place around <strong>Day 4 to Day 10</strong>. Buyers should schedule it as soon as possible after the contract is accepted. Waiting too long can compress the rest of the timeline and leave little room for repair discussions.</p>

<p>During the inspection, a licensed inspector checks the property’s major systems and visible condition. This often includes the roof, plumbing, electrical, HVAC, windows, foundation, attic, appliances, and more.</p>

<p>The inspection can lead to three general outcomes:</p>

<ol>

<li>The home looks good and you move forward</li>

<li>Minor issues show up and you accept them</li>

<li>Major issues are found and you ask for repairs, credits, or a price change</li>

</ol>

<p>This is where delays often begin. If the inspector finds water damage, electrical hazards, mold, foundation concerns, or a failing roof, the buyer and seller may need extra time to negotiate. Contractors may need to provide estimates. In some cases, additional inspections are required.</p>

<p>That can easily add <strong>one to two weeks</strong> to the time to close on a house.</p>

<p>The best way to stay on schedule is simple: <strong>book the inspection immediately</strong> and review the report quickly. The faster you act, the more room you have if surprises come up.</p>

<h3 id="step-4-finalize-the-purchase-agreement-after-inspection">Finalize the Purchase Agreement After Inspection</h3>

<p>After the inspection comes the negotiation stage.</p>

<p>This part often happens around <strong>Days 7 to 10</strong>, though it may stretch if repairs are significant. The buyer may ask the seller to make repairs, offer a credit at closing, reduce the price, or simply leave the home as-is.</p>

<p>At this point, the contract may be updated with addenda that reflect the final agreement.</p>

<p>This step matters because lenders, title companies, and closing attorneys need clean paperwork. If the inspection results lead to changes, those changes must be documented properly. Missing signatures or incomplete repair agreements can hold up final approval later.</p>

<p>This stage may not sound dramatic, but it is one of the most common places where deals lose speed. If both sides respond quickly, it can be handled in a day or two. If either side delays or emotions run high, it can drag on.</p>

<p>The smoother this stage goes, the easier the rest of the closing process steps become.</p>

<h3 id="step-5-submit-and-finalize-your-mortgage-application">Submit and Finalize Your Mortgage Application</h3>

<p>If you are financing the purchase, this is where the lender becomes the center of the transaction.</p>

<p>Mortgage application and document collection often happen in the first <strong>one to two weeks</strong>, even if the pre-approval was done earlier. The lender will ask for updated information such as:</p>

<ul>

<li>Pay stubs</li>

<li>W-2s or tax returns</li>

<li>Bank statements</li>

<li>Photo ID</li>

<li>Employment details</li>

<li>Asset documentation</li>

<li>Gift letters if someone is helping with funds</li>

</ul>

<p>This is not the time to go quiet or delay emails. If your lender asks for a document, send it quickly.</p>

<p>Many buyers are surprised by how detailed this part can be. Even strong borrowers may be asked to explain deposits, verify employment, clarify debts, or re-send documents in a different format. That is normal. It is simply part of verifying the loan.</p>

<p>If you want a better answer to <strong>how long does it take to close on a house</strong>, know this: <strong>loan delays often come from missing or outdated documents</strong>.</p>

<p>A fast buyer responds quickly. A delayed buyer waits three days to upload a bank statement. That difference matters.</p>

<h3 id="step-6-appraisal-of-the-home">Appraisal of the Home</h3>

<p>The appraisal usually happens around <strong>Days 14 to 20</strong>, although the timing depends on appraiser availability and the lender’s schedule.</p>

<p>The lender orders the appraisal to confirm that the home is worth the purchase price. This protects the lender from loaning more than the property is worth.</p>

<p>If the appraisal comes in at value, the deal usually moves ahead without issue.</p>

<p>If the appraisal comes in <strong>below</strong> the contract price, things can get more complicated. The buyer and seller may need to renegotiate. The buyer may need to bring extra cash. The seller may need to lower the price. Or the parties may dispute the valuation and request a reconsideration.</p>

<p>Any of those outcomes can add time.</p>

<p>A low appraisal is one of the biggest factors delaying home closing because it affects financing directly. Until the value issue is resolved, the lender may not fully approve the loan.</p>

<p>If you are a buyer, this is a good reminder to stay financially flexible. Even a solid transaction can hit a bump here.</p>

<p><strong>CTA:</strong> <strong>Need help preparing for a smooth purchase? Download our free home closing checklist and get organized before the deadlines begin.</strong></p>

<h3 id="step-7-underwriting-and-clear-to-close-">Underwriting and “Clear to Close”</h3>

<p>This is often the longest and most stressful part of the process.</p>

<p>Underwriting usually happens between <strong>Days 25 and 45</strong>. During this stage, the lender reviews the full file in detail. The underwriter checks your credit, income, debts, assets, property details, title work, and appraisal. They also confirm that the loan meets all guidelines.</p>

<p>It is common for the underwriter to issue <strong>conditions</strong>. These are follow-up requests the borrower must satisfy before final approval. For example, the underwriter may ask for:</p>

<ul>

<li>An updated pay stub</li>

<li>A letter explaining a credit inquiry</li>

<li>Proof that earnest money cleared the bank</li>

<li>Verification of employment</li>

<li>Clarification of a bank deposit</li>

<li>Proof that a debt was paid off</li>

</ul>

<p>This is why people often feel like the lender keeps asking for “just one more thing.”</p>

<p>The key is not to panic. It is a normal part of the process. But it can absolutely affect how long it takes to close on a house.</p>

<p>If you respond quickly and the file is clean, the lender may issue a <strong>clear to close</strong> on schedule. That means all major loan conditions are satisfied and the closing can be prepared.</p>

<p>If there are issues with income, employment changes, credit changes, or missing paperwork, underwriting can slow down fast.</p>

<p>This is also why buyers should avoid major financial moves during closing. Don’t open new credit cards. Don’t finance furniture. Don’t switch jobs if you can avoid it. Don’t move large amounts of money without being ready to explain it.</p>

<p>A lender wants stability. The more stable your financial picture remains, the faster underwriting tends to move.</p>

<h3 id="step-8-final-walkthrough-and-closing-day">Final Walkthrough and Closing Day</h3>

<p>The final walkthrough usually happens within <strong>24 to 48 hours before closing</strong>.</p>

<p>This is your chance to make sure the home is in the expected condition, any agreed repairs were completed, and nothing major changed since your last visit. You are not doing a new inspection. You are checking that the home is ready to transfer as promised.</p>

<p>Then comes closing day.</p>

<p>This is the moment buyers picture when they first ask, <strong>how long does it take to close on a house</strong>. But by this point, most of the real work has already happened.</p>

<p>On closing day, you will sign a stack of documents, review your final numbers, bring certified funds or confirm your wire transfer, and complete the legal transfer. Once the documents are signed and the deed is recorded, you get the keys.</p>

<p>[<strong>Process Flowchart Placeholder</strong>]</p>

<p>One thing many buyers overlook is that <strong>title issues</strong> can appear late and slow everything down. Problems like unpaid liens, missing signatures, unresolved ownership issues, or recording errors can add unexpected time. Real estate attorneys often warn that title problems can extend a closing by <strong>two to four weeks</strong>, depending on the issue.</p>

<p>That is why the final days matter just as much as the first.</p>

<p>Before closing day, confirm:</p>

<ul>

<li>Your wire instructions directly with the title or closing company</li>

<li>The exact amount of money due</li>

<li>Your ID requirements</li>

<li>The signing time and location</li>

<li>Whether possession happens immediately or later</li>

</ul>

<p>One wrong payment method or a last-minute paperwork problem can delay the finish line.</p>

<h2 id="factors-that-delay-closing-on-a-house">Factors That Delay Closing on a House</h2>

<p>Even if your contract says 30 or 45 days, real life does not always follow the schedule.</p>

<p>If you want to understand <strong>how long does it take to close on a house</strong>, you also need to understand what slows the process down. Most delays are not random. They usually fall into a few common categories.</p>

<p>Here are the biggest ones.</p>

<h3 id="1-inspection-issues">Inspection Issues</h3>

<p>A home inspection can reveal problems that no one expected.</p>

<p>Maybe the roof has hidden damage. Maybe the electrical panel is outdated. Maybe there is mold in the attic or plumbing leaks under the home. When that happens, the buyer and seller need time to decide what to do.</p>

<p>That can mean repair estimates, contractor scheduling, new negotiation, or updated contract terms. Even when both sides want to stay in the deal, this can add <strong>7 to 14 days</strong> or more.</p>

<p>The best way to reduce this risk is to schedule the inspection early and review the report right away.</p>

<h3 id="2-financing-problems">Financing Problems</h3>

<p>Financing is one of the most common reasons a closing gets pushed back.</p>

<p>A lender may ask for more documents. A buyer’s debt-to-income ratio may shift. Employment may need extra verification. Bank statements may raise questions. A credit score may change. Even a small issue can slow underwriting.</p>

<p>This is why buyers should stay financially quiet during the closing period. Don’t make big purchases. Don’t apply for new credit. Don’t move money around carelessly. The cleaner your file stays, the smoother your timeline usually is.</p>

<h3 id="3-title-problems">Title Problems</h3>

<p>Title issues are less exciting than inspections, but they can be even more serious.</p>

<p>The title company or attorney must confirm that the seller has the legal right to transfer the property. If there are liens, ownership disputes, recording mistakes, unpaid taxes, or missing legal documents, the closing may stop until those issues are cleared.</p>

<p>This kind of delay is frustrating because it may have nothing to do with the buyer. But it still affects the house closing timeline.</p>

<h3 id="4-low-appraisal">Low Appraisal</h3>

<p>When the appraisal comes in lower than the agreed purchase price, the lender may not approve the full loan amount.</p>

<p>That puts everyone in negotiation mode.</p>

<p>The buyer may need to increase the down payment. The seller may need to reduce the price. Both sides may need to meet in the middle. In some cases, the deal falls apart. In others, it continues after a delay.</p>

<p>This is one of the most stressful factors delaying home closing because it affects both finances and emotions at the same time.</p>

<h3 id="5-seller-delays">Seller Delays</h3>

<p>Sometimes the buyer is fully ready, but the seller is not.</p>

<p>Maybe the seller still needs to move out. Maybe they are buying another home and their timelines are tied together. Maybe repairs were promised but not finished. Maybe new construction is behind schedule.</p>

<p>This is especially common with builder homes and complex chain transactions. Even if you do everything right, the closing can still be pushed back by the seller’s situation.</p>

<h3 id="6-closing-day-mistakes">Closing Day Mistakes</h3>

<p>Yes, even the last step can go wrong.</p>

<p>Incorrect wiring, missing ID, unsigned documents, delayed funds, and last-minute legal questions can all affect the final handoff. Sometimes the delay is only a few hours. Sometimes it moves the closing to the next day or beyond.</p>

<p>That is why preparation matters all the way to the finish line.</p>

<h3 id="delay-risks-and-simple-fixes">Delay Risks and Simple Fixes</h3>

<table>

<thead>

<tr>

<th><strong>Delay Factor</strong></th>

<th><strong>Average Extra Time</strong></th>

<th><strong>How to Reduce the Risk</strong></th>

</tr>

</thead>

<tbody>

<tr>

<td>Inspection Issues</td>

<td>7–14 days</td>

<td>Schedule inspection immediately and respond fast</td>

</tr>

<tr>

<td>Financing Problems</td>

<td>15–30 days</td>

<td>Get fully pre-approved and submit documents quickly</td>

</tr>

<tr>

<td>Title Issues</td>

<td>7–28 days</td>

<td>Use an experienced title company or real estate attorney</td>

</tr>

<tr>

<td>Low Appraisal</td>

<td>5–15 days</td>

<td>Review comparable sales and keep room for negotiation</td>

</tr>

<tr>

<td>Seller Delays</td>

<td>3–30+ days</td>

<td>Confirm move-out plans and repair deadlines early</td>

</tr>

<tr>

<td>Closing Day Errors</td>

<td>1 day to several days</td>

<td>Double-check funds, ID, and all final instructions</td>

</tr>

</tbody>

</table>

<p>[<strong>Delay Factors Chart Placeholder</strong>]</p>

<p>The main lesson here is simple: <strong>a delayed closing is usually a chain reaction</strong>. One issue causes another step to wait. That is why proactive communication matters so much.</p>

<p>If you stay on top of the process, you cannot eliminate every delay, but you can prevent many of the most common ones.</p>

<h2 id="ways-to-speed-up-closing-on-a-house">Ways to Speed Up Closing on a House</h2>

<p>Now let’s talk solutions.</p>

<p>If you are wondering <strong>how long does it take to close on a house</strong>, you are probably also wondering whether you can shorten the process. In many cases, the answer is yes.</p>

<p>A smooth closing is not only about luck. It is often about preparation, timing, and working with the right people.</p>

<p>Here are some of the best <strong>fast home closing tips</strong>.</p>

<h3 id="get-fully-pre-approved-not-just-pre-qualified">Get Fully Pre-Approved, Not Just Pre-Qualified</h3>

<p>A casual pre-qualification is helpful, but it is not the same as a full pre-approval.</p>

<p>A full pre-approval means the lender has already reviewed your financial documents in detail. That gives you a stronger file and can save valuable time later. If underwriting has less to question, your loan moves more quickly.</p>

<h3 id="order-the-inspection-and-appraisal-early">Order the Inspection and Appraisal Early</h3>

<p>Don’t wait around once the contract is signed.</p>

<p>Book the inspection immediately. Make sure your lender orders the appraisal as soon as allowed. The earlier these two items happen, the more room you have if a problem shows up.</p>

<p>This is one of the easiest ways to shorten the time to close on a house.</p>

<h3 id="send-documents-the-same-day">Send Documents the Same Day</h3>

<p>If your lender or agent asks for something, send it fast.</p>

<p>The people handling your file are often moving dozens of transactions at once. When your documents arrive late, your file can lose momentum. When you respond the same day, your file is easier to keep moving.</p>

<h3 id="avoid-job-credit-and-bank-changes">Avoid Job, Credit, and Bank Changes</h3>

<p>This tip matters more than most buyers think.</p>

<p>Don’t change jobs if you can avoid it. Don’t open a new credit account. Don’t buy a car. Don’t finance furniture before closing. Don’t make unusual deposits without records. Every financial change can trigger new questions.</p>

<p>If you want a fast closing, keep your finances boring.</p>

<h3 id="work-with-experienced-professionals">Work With Experienced Professionals</h3>

<p>A knowledgeable agent, lender, title company, and attorney can make a huge difference.</p>

<p>An experienced team spots issues earlier, communicates better, and knows how to keep deadlines on track. A disorganized team can add stress and wasted days even when the deal itself is solid.</p>

<h3 id="use-digital-tools-when-available">Use Digital Tools When Available</h3>

<p>Many lenders and title companies now use digital document portals, e-signatures for certain forms, text updates, and online status tracking. These tools can cut down on delays caused by printing, scanning, mailing, and back-and-forth confusion.</p>

<p>In 2026, these systems have made faster closings more realistic for many buyers.</p>

<h3 id="stay-reachable-every-day">Stay Reachable Every Day</h3>

<p>During the closing period, treat your phone and email like part of your moving checklist.</p>

<p>If your lender, agent, or title company cannot reach you, deadlines can slip quickly. A missed call can cost a day. A missed email can cost several.</p>

<h3 id="fast-track-vs-standard-track">Fast Track vs. Standard Track</h3>

<p>If you are deciding whether to push for a faster close, here is a simple comparison.</p>

<ul>

<li><strong>Fast closing track</strong>

<ul>

<li>Good for motivated buyers and clean files</li>

<li>Works well with cash or strong financing</li>

<li>Can reduce carrying costs and stress</li>

<li>Leaves less room for mistakes or extra negotiations</li>

</ul>

</li>

<li><strong>Standard closing track</strong>

<ul>

<li>Gives more flexibility for inspections and underwriting</li>

<li>Better for first-time buyers who want breathing room</li>

<li>Easier when the seller needs more time</li>

<li>May feel slower, but often reduces last-minute pressure</li>

</ul>

</li>

</ul>

<p>The right choice depends on your situation. Faster is not always better if it creates avoidable stress. But if your documents are ready and your team is efficient, a quick close can absolutely happen.</p>

<p><strong>CTA:</strong> <strong>Want a smoother closing from start to finish? Contact our real estate experts for personalized closing advice and a strategy that fits your timeline.</strong></p>

<h2 id="how-closing-timelines-change-by-situation">How Closing Timelines Change by Situation</h2>

<p>Not every home purchase follows the same timeline. That is why the answer to <strong>how long does it take to close on a house</strong> depends on the type of deal.</p>

<h3 id="cash-purchase">Cash Purchase</h3>

<p>A cash deal is usually the fastest path.</p>

<p>Without a mortgage, the buyer avoids underwriting, lender conditions, and many of the document requests that slow traditional purchases. In many cases, a cash sale can close in <strong>4 to 10 days</strong>.</p>

<p>That said, cash deals still need title work, a purchase agreement, and closing documents. So “cash” does not mean “instant.” It simply removes one of the largest sources of delay.</p>

<h3 id="conventional-mortgage">Conventional Mortgage</h3>

<p>This is the most common path for many buyers.</p>

<p>A conventional loan often closes in <strong>30 to 45 days</strong>, which is why that range is considered standard. If the borrower is well prepared and the property is straightforward, 30 days is very possible.</p>

<h3 id="fha-or-va-loan">FHA or VA Loan</h3>

<p>Government-backed loans can take a bit longer.</p>

<p>These loans often involve extra documentation, stricter appraisal standards, and added review steps. Many buyers using FHA or VA financing should expect <strong>45 to 60 days</strong>, depending on the lender and property.</p>

<h3 id="new-construction">New Construction</h3>

<p>New builds usually take longer than resale homes.</p>

<p>Even if the financing is ready, construction delays, inspections, permits, weather, materials, or builder scheduling can all change the closing date. Many new construction timelines run <strong>60 to 90 days or more</strong>, especially if the home is not yet finished when the contract is signed.</p>

<h3 id="competitive-markets">Competitive Markets</h3>

<p>In hot markets, closing times may be shorter.</p>

<p>Sellers often favor buyers who can close quickly, especially when multiple offers are involved. That may push buyers to choose lenders known for speed, waive certain contingencies where appropriate, or prepare documents in advance.</p>

<h3 id="regional-differences">Regional Differences</h3>

<p>Where you buy also matters.</p>

<p>Some states rely heavily on attorneys. Others use title companies more directly. Some local markets have faster appraiser availability. Others have county recording delays or local customs that add time.</p>

<p>So while the average time to close on a house gives a useful benchmark, your local market can still shift the reality.</p>

<h2 id="frequently-asked-questions">Frequently Asked Questions</h2>

<h3 id="how-long-does-it-take-to-close-on-a-house-with-cash-">How long does it take to close on a house with cash?</h3>

<p>A cash purchase can often close in <strong>4 to 10 days</strong>. It is faster because there is no mortgage underwriting, but title work and legal paperwork still need to be completed.</p>

<h3 id="what-is-the-fastest-possible-closing-time-on-a-house-">What is the fastest possible closing time on a house?</h3>

<p>In some well-prepared situations, buyers can close in <strong>about 14 days</strong>. This usually requires cash or a highly efficient lender, fast title work, and no major inspection or appraisal issues.</p>

<h3 id="is-closing-in-30-days-realistic-">Is closing in 30 days realistic?</h3>

<p>Yes, <strong>30 days is realistic</strong> for many standard purchases, especially if the buyer is pre-approved, documents are ready, and the property has no major issues.</p>

<h3 id="do-new-construction-homes-take-longer-to-close-">Do new construction homes take longer to close?</h3>

<p>Yes, they usually do. New builds often take <strong>60 to 90 days or more</strong> because builder schedules, permits, and final construction steps can affect the closing date.</p>

<h3 id="what-causes-the-biggest-closing-delays-">What causes the biggest closing delays?</h3>

<p>The most common delays are <strong>inspection problems, financing issues, title defects, low appraisals, seller timing problems, and closing day paperwork mistakes</strong>.</p>

<h3 id="how-can-i-avoid-closing-delays-">How can I avoid closing delays?</h3>

<p>You can reduce delays by getting fully pre-approved, sending documents quickly, scheduling the inspection early, avoiding credit or job changes, and working with experienced professionals.</p>

<h3 id="can-a-lender-delay-closing-at-the-last-minute-">Can a lender delay closing at the last minute?</h3>

<p>Yes, that can happen. If underwriting needs updated documents, if employment needs to be re-verified, or if final loan conditions are incomplete, the lender can delay closing until everything is cleared.</p>

<h2 id="final-thoughts-so-how-long-does-it-take-to-close-on-a-house-">Final Thoughts: So, How Long Does It Take to Close on a House?</h2>

<p>So, <strong>how long does it take to close on a house?</strong></p>

<p>For most buyers, the answer is <strong>30 to 45 days</strong>. That is the standard window for a financed purchase. Cash deals can move much faster, while FHA, VA, and new construction purchases often take longer. The exact timeline depends on the inspection, appraisal, underwriting, title work, and how quickly everyone involved responds.</p>

<p>The key thing to remember is this: closing is not just about waiting. It is about preparation.</p>

<p>When you understand the process, stay organized, and respond quickly, you give yourself the best chance of a smooth, low-stress finish.</p>

<p><a href="https://comeawayhome.co.uk/">House</a></p>

You’ve found the house you love. Your offer is accepted. The excitement is real.

Then the next question hits you: how long does it take to close on a house?

That’s the part many buyers underestimate. You might think once the seller says yes, the hard part is over. In reality, the closing period is where a lot of moving parts come together. The lender reviews your finances. The home gets inspected. The appraisal comes in. Title work gets checked. Legal paperwork gets prepared. Funds get transferred. And if even one piece slows down, the whole timeline can shift.

In most cases, the time to close on a house is around 30 to 45 days. But that does not mean every home purchase fits neatly into that window. Some cash deals can close in less than two weeks. Some financed purchases can stretch to 60 days or longer. New construction can take even more time depending on the builder, permits, and completion date.

That is why buyers often feel stressed during this stage. You may be trying to plan your move, lock in your rate, schedule utilities, and coordinate with your current lease or home sale. If the timeline changes, everything else can change with it.

The good news is that the closing process is much easier to manage when you understand what happens at each stage.

In this guide, you’ll learn how long does it take to close on a house, what happens from accepted offer to closing day, which delays are most common, and what you can do to keep the process moving.

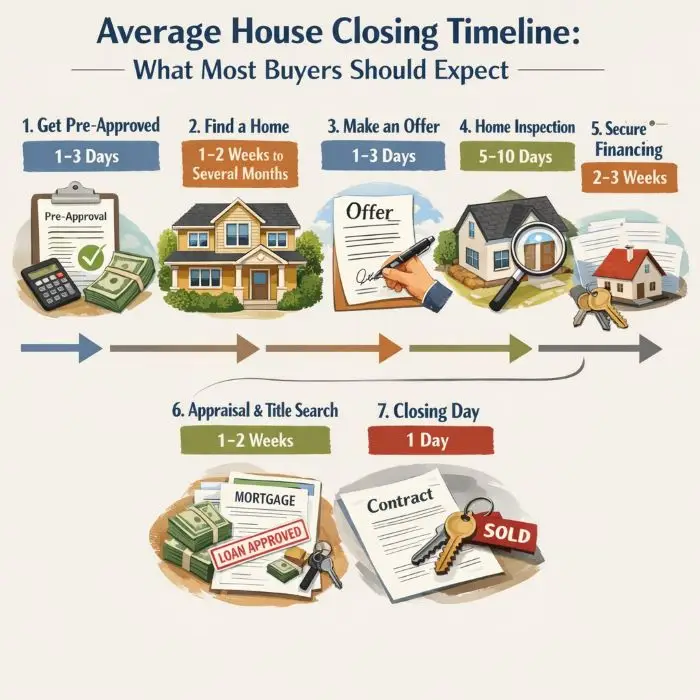

Average House Closing Timeline: What Most Buyers Should Expect

If you are asking how long does it take to close on a house, the short answer is this: most buyers close in 30 to 45 days.

That window is common for buyers using a mortgage. It gives enough time for the lender to process the loan, the home to be inspected and appraised, the title work to be completed, and all final paperwork to be prepared. In a normal market, that is the standard house closing timeline many buyers experience.

But let’s make one thing clear. “Normal” does not always mean “guaranteed.” Some deals move faster. Others take longer. A simple purchase with a strong borrower, a responsive seller, and a clean property can close quickly. A deal with repair negotiations, title issues, or loan paperwork problems can take much longer.

Cash purchases are the biggest exception. Because there is no mortgage approval involved, buyers can often skip some of the longest parts of the timeline. That means a cash deal may close in as little as 4 to 10 days, depending on how quickly the title company, seller, and buyer complete their tasks.

On the other hand, government-backed loans, rural properties, condos with document issues, and new construction homes often take longer than the average time to close on a house. In those cases, the closing process may reach 45 to 60 days or more.

To make this easier to follow, here is a simple overview.

| Phase |

Typical Timeframe |

What Happens |

| Offer Acceptance |

1–3 days |

Buyer and seller agree on price, terms, and target closing date |

| Inspection & Early Due Diligence |

4–10 days |

Home inspection is completed, issues are discovered, repair talks may begin |

| Appraisal & Loan Processing |

11–25 days |

Lender orders appraisal, reviews documents, and starts underwriting |

| Underwriting & Final Approval |

26–40 days |

Final checks on credit, income, assets, title, and conditions |

| Closing Preparation |

41–45 days |

Buyer receives closing disclosure, reviews numbers, and gets funds ready |

| Closing Day |

Around Day 45 |

Final signing, wire transfer, deed recording, and key handoff |

[Timeline Infographic Placeholder]

A big reason the process takes this long is that several steps happen both one after another and at the same time. For example, while you’re booking the inspection, your lender may be collecting your pay stubs and bank statements. While the appraisal is being scheduled, the title company may be researching ownership records. While the underwriter reviews your loan, your agent may still be negotiating repairs.

So when people ask, how long does it take to close on a house, they are really asking how long it takes for all these pieces to line up.

A good way to think about it is this:

- 30 days is possible for a clean, well-prepared file

- 45 days is common for a standard financed purchase

- 60+ days can happen when problems or extra requirements show up

If you are buying soon, it helps to build your moving plans around a little flexibility. A target closing date is important, but it is still a target. The smoother your financing, paperwork, and communication are, the better your chances of hitting it.

Step-by-Step Closing Process: What Happens After Your Offer Is Accepted

Understanding the closing process steps makes the whole experience feel less confusing. Instead of thinking of closing as one giant waiting period, it helps to break it into stages.

Below is the full process, from accepted offer to getting your keys.

Offer Negotiation and Acceptance

The closing timeline starts when the seller accepts your offer.

This first stage often takes 1 to 3 days, though it can move faster or slower depending on how much back-and-forth happens. The buyer may make an offer, the seller may counter, and both sides may adjust the price, contingencies, closing date, seller credits, or included items like appliances.

This is also when the expected closing date is usually written into the contract.

That date matters more than many buyers realize. If you ask for a closing date that is too aggressive, you may create pressure before the lender and title company even begin. If you choose a date that is too far out, you may lose momentum and create extra waiting.

A practical move is to request about 45 days unless your lender clearly tells you they can close faster.

This stage may feel simple, but it shapes the rest of the house closing timeline. A strong offer with realistic terms can set the deal up for success. A messy contract with unclear repair expectations or tight deadlines can create problems later.

Pro tip: before you submit the offer, talk to your lender and your real estate agent together. That way, the closing date in the contract matches what is actually realistic.

Open Escrow and Deposit Earnest Money

Once the offer is accepted, the transaction usually enters escrow.

Escrow is a neutral process where money and documents are held safely until all contract terms are met. This protects both buyer and seller. The buyer typically sends earnest money, sometimes called a good-faith deposit, to the escrow or title company within a few days of the contract being signed.

This part often happens right away, usually in the first 1 to 5 days after acceptance.

It may sound like a small step, but it is important. If the earnest money deposit is late, that can trigger problems early in the process. It may even put the contract at risk in some cases.

Escrow also becomes the central place where important documents, title work, and closing instructions begin to come together. Think of it as the hub that keeps the deal organized.

Schedule the Home Inspection

One of the most important answers to how long does it take to close on a house comes from what happens during the inspection period.

The home inspection usually takes place around Day 4 to Day 10. Buyers should schedule it as soon as possible after the contract is accepted. Waiting too long can compress the rest of the timeline and leave little room for repair discussions.

During the inspection, a licensed inspector checks the property’s major systems and visible condition. This often includes the roof, plumbing, electrical, HVAC, windows, foundation, attic, appliances, and more.

The inspection can lead to three general outcomes:

- The home looks good and you move forward

- Minor issues show up and you accept them

- Major issues are found and you ask for repairs, credits, or a price change

This is where delays often begin. If the inspector finds water damage, electrical hazards, mold, foundation concerns, or a failing roof, the buyer and seller may need extra time to negotiate. Contractors may need to provide estimates. In some cases, additional inspections are required.

That can easily add one to two weeks to the time to close on a house.

The best way to stay on schedule is simple: book the inspection immediately and review the report quickly. The faster you act, the more room you have if surprises come up.

Finalize the Purchase Agreement After Inspection

After the inspection comes the negotiation stage.

This part often happens around Days 7 to 10, though it may stretch if repairs are significant. The buyer may ask the seller to make repairs, offer a credit at closing, reduce the price, or simply leave the home as-is.

At this point, the contract may be updated with addenda that reflect the final agreement.

This step matters because lenders, title companies, and closing attorneys need clean paperwork. If the inspection results lead to changes, those changes must be documented properly. Missing signatures or incomplete repair agreements can hold up final approval later.

This stage may not sound dramatic, but it is one of the most common places where deals lose speed. If both sides respond quickly, it can be handled in a day or two. If either side delays or emotions run high, it can drag on.

The smoother this stage goes, the easier the rest of the closing process steps become.

Submit and Finalize Your Mortgage Application

If you are financing the purchase, this is where the lender becomes the center of the transaction.

Mortgage application and document collection often happen in the first one to two weeks, even if the pre-approval was done earlier. The lender will ask for updated information such as:

- Pay stubs

- W-2s or tax returns

- Bank statements

- Photo ID

- Employment details

- Asset documentation

- Gift letters if someone is helping with funds

This is not the time to go quiet or delay emails. If your lender asks for a document, send it quickly.

Many buyers are surprised by how detailed this part can be. Even strong borrowers may be asked to explain deposits, verify employment, clarify debts, or re-send documents in a different format. That is normal. It is simply part of verifying the loan.

If you want a better answer to how long does it take to close on a house, know this: loan delays often come from missing or outdated documents.

A fast buyer responds quickly. A delayed buyer waits three days to upload a bank statement. That difference matters.

Appraisal of the Home

The appraisal usually happens around Days 14 to 20, although the timing depends on appraiser availability and the lender’s schedule.

The lender orders the appraisal to confirm that the home is worth the purchase price. This protects the lender from loaning more than the property is worth.

If the appraisal comes in at value, the deal usually moves ahead without issue.

If the appraisal comes in below the contract price, things can get more complicated. The buyer and seller may need to renegotiate. The buyer may need to bring extra cash. The seller may need to lower the price. Or the parties may dispute the valuation and request a reconsideration.

Any of those outcomes can add time.

A low appraisal is one of the biggest factors delaying home closing because it affects financing directly. Until the value issue is resolved, the lender may not fully approve the loan.

If you are a buyer, this is a good reminder to stay financially flexible. Even a solid transaction can hit a bump here.

CTA: Need help preparing for a smooth purchase? Download our free home closing checklist and get organized before the deadlines begin.

Underwriting and “Clear to Close”

This is often the longest and most stressful part of the process.

Underwriting usually happens between Days 25 and 45. During this stage, the lender reviews the full file in detail. The underwriter checks your credit, income, debts, assets, property details, title work, and appraisal. They also confirm that the loan meets all guidelines.

It is common for the underwriter to issue conditions. These are follow-up requests the borrower must satisfy before final approval. For example, the underwriter may ask for:

- An updated pay stub

- A letter explaining a credit inquiry

- Proof that earnest money cleared the bank

- Verification of employment

- Clarification of a bank deposit

- Proof that a debt was paid off

This is why people often feel like the lender keeps asking for “just one more thing.”

The key is not to panic. It is a normal part of the process. But it can absolutely affect how long it takes to close on a house.

If you respond quickly and the file is clean, the lender may issue a clear to close on schedule. That means all major loan conditions are satisfied and the closing can be prepared.

If there are issues with income, employment changes, credit changes, or missing paperwork, underwriting can slow down fast.

This is also why buyers should avoid major financial moves during closing. Don’t open new credit cards. Don’t finance furniture. Don’t switch jobs if you can avoid it. Don’t move large amounts of money without being ready to explain it.

A lender wants stability. The more stable your financial picture remains, the faster underwriting tends to move.

Final Walkthrough and Closing Day

The final walkthrough usually happens within 24 to 48 hours before closing.

This is your chance to make sure the home is in the expected condition, any agreed repairs were completed, and nothing major changed since your last visit. You are not doing a new inspection. You are checking that the home is ready to transfer as promised.

Then comes closing day.

This is the moment buyers picture when they first ask, how long does it take to close on a house. But by this point, most of the real work has already happened.

On closing day, you will sign a stack of documents, review your final numbers, bring certified funds or confirm your wire transfer, and complete the legal transfer. Once the documents are signed and the deed is recorded, you get the keys.

[Process Flowchart Placeholder]

One thing many buyers overlook is that title issues can appear late and slow everything down. Problems like unpaid liens, missing signatures, unresolved ownership issues, or recording errors can add unexpected time. Real estate attorneys often warn that title problems can extend a closing by two to four weeks, depending on the issue.

That is why the final days matter just as much as the first.

Before closing day, confirm:

- Your wire instructions directly with the title or closing company

- The exact amount of money due

- Your ID requirements

- The signing time and location

- Whether possession happens immediately or later

One wrong payment method or a last-minute paperwork problem can delay the finish line.

Factors That Delay Closing on a House

Even if your contract says 30 or 45 days, real life does not always follow the schedule.

If you want to understand how long does it take to close on a house, you also need to understand what slows the process down. Most delays are not random. They usually fall into a few common categories.

Here are the biggest ones.

Inspection Issues

A home inspection can reveal problems that no one expected.

Maybe the roof has hidden damage. Maybe the electrical panel is outdated. Maybe there is mold in the attic or plumbing leaks under the home. When that happens, the buyer and seller need time to decide what to do.

That can mean repair estimates, contractor scheduling, new negotiation, or updated contract terms. Even when both sides want to stay in the deal, this can add 7 to 14 days or more.

The best way to reduce this risk is to schedule the inspection early and review the report right away.

Financing Problems

Financing is one of the most common reasons a closing gets pushed back.

A lender may ask for more documents. A buyer’s debt-to-income ratio may shift. Employment may need extra verification. Bank statements may raise questions. A credit score may change. Even a small issue can slow underwriting.

This is why buyers should stay financially quiet during the closing period. Don’t make big purchases. Don’t apply for new credit. Don’t move money around carelessly. The cleaner your file stays, the smoother your timeline usually is.

Title Problems

Title issues are less exciting than inspections, but they can be even more serious.

The title company or attorney must confirm that the seller has the legal right to transfer the property. If there are liens, ownership disputes, recording mistakes, unpaid taxes, or missing legal documents, the closing may stop until those issues are cleared.

This kind of delay is frustrating because it may have nothing to do with the buyer. But it still affects the house closing timeline.

Low Appraisal

When the appraisal comes in lower than the agreed purchase price, the lender may not approve the full loan amount.

That puts everyone in negotiation mode.

The buyer may need to increase the down payment. The seller may need to reduce the price. Both sides may need to meet in the middle. In some cases, the deal falls apart. In others, it continues after a delay.

This is one of the most stressful factors delaying home closing because it affects both finances and emotions at the same time.

Seller Delays

Sometimes the buyer is fully ready, but the seller is not.

Maybe the seller still needs to move out. Maybe they are buying another home and their timelines are tied together. Maybe repairs were promised but not finished. Maybe new construction is behind schedule.

This is especially common with builder homes and complex chain transactions. Even if you do everything right, the closing can still be pushed back by the seller’s situation.

Closing Day Mistakes

Yes, even the last step can go wrong.

Incorrect wiring, missing ID, unsigned documents, delayed funds, and last-minute legal questions can all affect the final handoff. Sometimes the delay is only a few hours. Sometimes it moves the closing to the next day or beyond.

That is why preparation matters all the way to the finish line.

Delay Risks and Simple Fixes

| Delay Factor |

Average Extra Time |

How to Reduce the Risk |

| Inspection Issues |

7–14 days |

Schedule inspection immediately and respond fast |

| Financing Problems |

15–30 days |

Get fully pre-approved and submit documents quickly |

| Title Issues |

7–28 days |

Use an experienced title company or real estate attorney |

| Low Appraisal |

5–15 days |

Review comparable sales and keep room for negotiation |

| Seller Delays |

3–30+ days |

Confirm move-out plans and repair deadlines early |

| Closing Day Errors |

1 day to several days |

Double-check funds, ID, and all final instructions |

[Delay Factors Chart Placeholder]

The main lesson here is simple: a delayed closing is usually a chain reaction. One issue causes another step to wait. That is why proactive communication matters so much.

If you stay on top of the process, you cannot eliminate every delay, but you can prevent many of the most common ones.

Ways to Speed Up Closing on a House

Now let’s talk solutions.

If you are wondering how long does it take to close on a house, you are probably also wondering whether you can shorten the process. In many cases, the answer is yes.

A smooth closing is not only about luck. It is often about preparation, timing, and working with the right people.

Here are some of the best fast home closing tips.

Get Fully Pre-Approved, Not Just Pre-Qualified

A casual pre-qualification is helpful, but it is not the same as a full pre-approval.

A full pre-approval means the lender has already reviewed your financial documents in detail. That gives you a stronger file and can save valuable time later. If underwriting has less to question, your loan moves more quickly.

Order the Inspection and Appraisal Early

Don’t wait around once the contract is signed.

Book the inspection immediately. Make sure your lender orders the appraisal as soon as allowed. The earlier these two items happen, the more room you have if a problem shows up.

This is one of the easiest ways to shorten the time to close on a house.

Send Documents the Same Day

If your lender or agent asks for something, send it fast.

The people handling your file are often moving dozens of transactions at once. When your documents arrive late, your file can lose momentum. When you respond the same day, your file is easier to keep moving.

Avoid Job, Credit, and Bank Changes

This tip matters more than most buyers think.

Don’t change jobs if you can avoid it. Don’t open a new credit account. Don’t buy a car. Don’t finance furniture before closing. Don’t make unusual deposits without records. Every financial change can trigger new questions.

If you want a fast closing, keep your finances boring.

Work With Experienced Professionals

A knowledgeable agent, lender, title company, and attorney can make a huge difference.

An experienced team spots issues earlier, communicates better, and knows how to keep deadlines on track. A disorganized team can add stress and wasted days even when the deal itself is solid.

Many lenders and title companies now use digital document portals, e-signatures for certain forms, text updates, and online status tracking. These tools can cut down on delays caused by printing, scanning, mailing, and back-and-forth confusion.

In 2026, these systems have made faster closings more realistic for many buyers.

Stay Reachable Every Day

During the closing period, treat your phone and email like part of your moving checklist.

If your lender, agent, or title company cannot reach you, deadlines can slip quickly. A missed call can cost a day. A missed email can cost several.

Fast Track vs. Standard Track

If you are deciding whether to push for a faster close, here is a simple comparison.

- Fast closing track

- Good for motivated buyers and clean files

- Works well with cash or strong financing

- Can reduce carrying costs and stress

- Leaves less room for mistakes or extra negotiations

- Standard closing track

- Gives more flexibility for inspections and underwriting

- Better for first-time buyers who want breathing room

- Easier when the seller needs more time

- May feel slower, but often reduces last-minute pressure

The right choice depends on your situation. Faster is not always better if it creates avoidable stress. But if your documents are ready and your team is efficient, a quick close can absolutely happen.

CTA: Want a smoother closing from start to finish? Contact our real estate experts for personalized closing advice and a strategy that fits your timeline.

How Closing Timelines Change by Situation

Not every home purchase follows the same timeline. That is why the answer to how long does it take to close on a house depends on the type of deal.

Cash Purchase

A cash deal is usually the fastest path.

Without a mortgage, the buyer avoids underwriting, lender conditions, and many of the document requests that slow traditional purchases. In many cases, a cash sale can close in 4 to 10 days.

That said, cash deals still need title work, a purchase agreement, and closing documents. So “cash” does not mean “instant.” It simply removes one of the largest sources of delay.

Conventional Mortgage

This is the most common path for many buyers.

A conventional loan often closes in 30 to 45 days, which is why that range is considered standard. If the borrower is well prepared and the property is straightforward, 30 days is very possible.

FHA or VA Loan

Government-backed loans can take a bit longer.

These loans often involve extra documentation, stricter appraisal standards, and added review steps. Many buyers using FHA or VA financing should expect 45 to 60 days, depending on the lender and property.

New Construction

New builds usually take longer than resale homes.

Even if the financing is ready, construction delays, inspections, permits, weather, materials, or builder scheduling can all change the closing date. Many new construction timelines run 60 to 90 days or more, especially if the home is not yet finished when the contract is signed.

Competitive Markets

In hot markets, closing times may be shorter.

Sellers often favor buyers who can close quickly, especially when multiple offers are involved. That may push buyers to choose lenders known for speed, waive certain contingencies where appropriate, or prepare documents in advance.

Regional Differences

Where you buy also matters.

Some states rely heavily on attorneys. Others use title companies more directly. Some local markets have faster appraiser availability. Others have county recording delays or local customs that add time.

So while the average time to close on a house gives a useful benchmark, your local market can still shift the reality.

Frequently Asked Questions

How long does it take to close on a house with cash?

A cash purchase can often close in 4 to 10 days. It is faster because there is no mortgage underwriting, but title work and legal paperwork still need to be completed.

What is the fastest possible closing time on a house?

In some well-prepared situations, buyers can close in about 14 days. This usually requires cash or a highly efficient lender, fast title work, and no major inspection or appraisal issues.

Is closing in 30 days realistic?

Yes, 30 days is realistic for many standard purchases, especially if the buyer is pre-approved, documents are ready, and the property has no major issues.

Do new construction homes take longer to close?

Yes, they usually do. New builds often take 60 to 90 days or more because builder schedules, permits, and final construction steps can affect the closing date.

What causes the biggest closing delays?

The most common delays are inspection problems, financing issues, title defects, low appraisals, seller timing problems, and closing day paperwork mistakes.

How can I avoid closing delays?

You can reduce delays by getting fully pre-approved, sending documents quickly, scheduling the inspection early, avoiding credit or job changes, and working with experienced professionals.

Can a lender delay closing at the last minute?

Yes, that can happen. If underwriting needs updated documents, if employment needs to be re-verified, or if final loan conditions are incomplete, the lender can delay closing until everything is cleared.

Final Thoughts: So, How Long Does It Take to Close on a House?

So, how long does it take to close on a house?

For most buyers, the answer is 30 to 45 days. That is the standard window for a financed purchase. Cash deals can move much faster, while FHA, VA, and new construction purchases often take longer. The exact timeline depends on the inspection, appraisal, underwriting, title work, and how quickly everyone involved responds.

The key thing to remember is this: closing is not just about waiting. It is about preparation.

When you understand the process, stay organized, and respond quickly, you give yourself the best chance of a smooth, low-stress finish.

House