<p>If you have been asking <a href="https://www.reddit.com/r/RealEstate/comments/zigsdk/how_long_does_it_take_on_average_to_buy_a_house/"><strong>how long does it take to buy a house</strong></a>, the honest answer is this: it can take <strong>a few weeks to several months</strong>, depending on your finances, the market, and whether you need to sell a home first. Some buyers move fast and close in about 30 days. Others need more time to search, compare options, get financing ready, and work through inspections and underwriting.</p>

<p>That may sound vague, but there is a good reason for it. Buying a home is not one single task. It is a chain of steps, and each step can move quickly or slowly depending on the situation. A buyer with a strong credit profile, a clear budget, and a responsive lender will usually move faster than someone still sorting out documents or waiting on a sale to finish.</p>

<p>In this guide, you will get a <strong>clear timeline</strong> for every major stage of the home-buying process. You will also see what usually slows buyers down, what can speed things up, and how the timeline changes in real life. We will walk through preapproval, home search, offers, inspections, underwriting, and closing in simple language.</p>

<p>If you want to plan ahead with confidence, this article will give you a practical <strong>home buying timeline</strong> you can actually use.</p>

<h2 id="what-how-long-does-it-take-to-buy-a-house-really-means">What “How Long Does It Take to Buy a House” Really Means</h2>

<p><img class="aligncenter wp-image-7135 size-full" src="https://comeawayhome.co.uk/wp-content/uploads/2026/05/ed33e595-d1a2-41b0-88dd-cb864bc54bdf-ezgif.com-jpg-to-webp-converter.webp" alt="how long does it take to buy a house" width="700" height="700" /></p>

<p>The phrase <strong>how long does it take to buy a house</strong> can mean different things to different people. That is why you may hear very different answers online. One person may be talking about the time it takes to find the right home. Another may mean the time from an accepted offer to closing. Someone else may be asking about the full process, including mortgage preapproval and selling their current home.</p>

<p>That difference matters. A buyer who already has financing ready may only need to focus on search, offer, and closing. A first-time buyer may need extra time for budgeting, document gathering, and lender review. If you are selling a home too, your timeline can stretch even more.</p>

<p>Here is a simple way to think about it.</p>

<table>

<thead>

<tr>

<th>What the timeline means</th>

<th>Typical time range</th>

<th>What it includes</th>

</tr>

</thead>

<tbody>

<tr>

<td><strong>Searching only</strong></td>

<td>2–12+ weeks</td>

<td>Browsing homes, touring, comparing neighborhoods, and choosing a property</td>

</tr>

<tr>

<td><strong>Offer to close</strong></td>

<td>30–45 days on average</td>

<td>Offer, negotiation, inspection, appraisal, underwriting, and closing</td>

</tr>

<tr>

<td><strong>Full buying process</strong></td>

<td>6–16+ weeks</td>

<td>Finances, preapproval, search, offer, mortgage approval, and closing</td>

</tr>

<tr>

<td><strong>Buying while selling</strong></td>

<td>3–6 months total</td>

<td>Listing your current home, finding a buyer, and coordinating both deals</td>

</tr>

</tbody>

</table>

<p>So when someone asks about the timeline, the best answer is usually, <strong>“It depends on which part of the process you mean.”</strong> That is the most useful way to look at it.</p>

<h2 id="typical-timeline-step-by-step">Typical Timeline: Step-by-Step</h2>

<p>The averages below reflect a fairly typical market. In a hot market, things can move faster. In a slower market or a more complicated loan scenario, the process can take longer.</p>

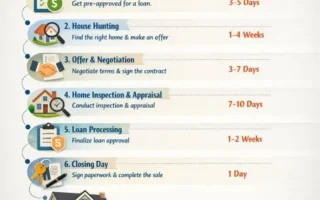

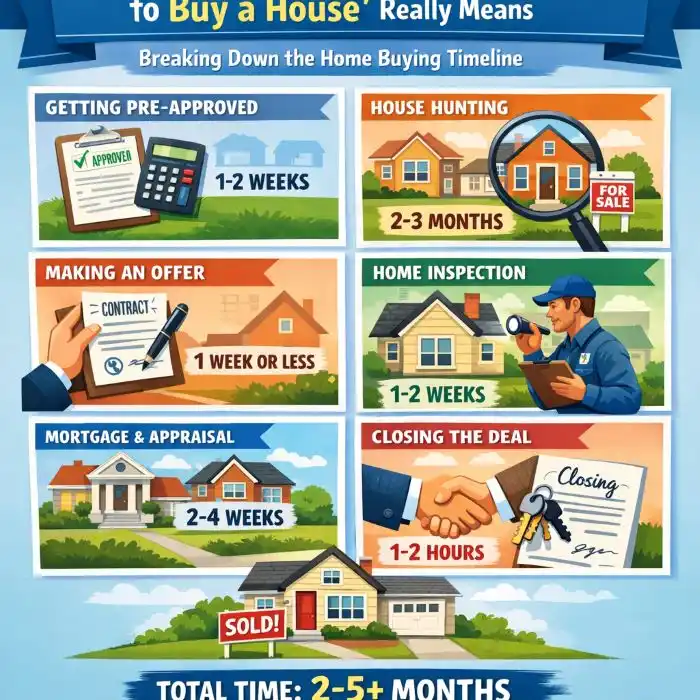

<h3 id="step-a-financial-prep-and-mortgage-preapproval">Financial Prep and Mortgage Preapproval</h3>

<p>Before you start touring homes, you need a clear picture of what you can afford. This stage usually includes checking your credit, setting a budget, estimating your down payment, and gathering documents like pay stubs, tax returns, bank statements, and ID.</p>

<p>A strong <strong>preapproval</strong> is more than a rough estimate. It tells sellers and agents that a lender has reviewed your finances and believes you are qualified for a certain loan amount. That can make your offer stronger later.</p>

<p>Typical time: <strong>1–3 weeks</strong></p>

<p>If you already have your paperwork ready, this stage can move quickly. If you have credit issues, inconsistent income, or missing records, it can take longer. This is also a good time to use a mortgage calculator or an internal financing guide on your site to help readers estimate their monthly payment and price range.</p>

<p>A simple rule is this: the better prepared you are now, the smoother the rest of the <strong>timeline</strong> becomes.</p>

<h3 id="step-b-home-search">Home Search</h3>

<p>Once your finances are ready, the search begins. This is often the most flexible part of the process because it depends on your priorities, your market, and how fast you make decisions. Some buyers find a home in a weekend. Others take months because they are waiting for the right neighborhood, layout, or price.</p>

<p>During this stage, you may look at neighborhoods, school zones, commute times, and property conditions. You may tour homes in person, use virtual tours, and compare features with your must-have list. A good agent can save time here by filtering out homes that do not fit your budget or goals.</p>

<p>Typical time: <strong>2–12+ weeks</strong></p>

<p>A few ways to shorten the search:</p>

<ul>

<li>Decide what you <strong>must have</strong> versus what is only nice to have.</li>

<li>Set up nightly property alerts so new listings reach you fast.</li>

<li>Be ready to tour quickly when a strong match appears.</li>

<li>Keep your budget realistic so you do not waste time on homes that are out of reach.</li>

</ul>

<p>This stage is where many buyers either gain momentum or lose it. Clear priorities make a big difference.</p>

<h3 id="step-c-making-an-offer-and-negotiation">Making an Offer and Negotiation</h3>

<p>Once you find the right property, the next step is the offer. Your agent will usually help you look at recent comparable sales, or comps, to decide on a fair price. You may also choose contingencies, such as financing, inspection, or appraisal protections.</p>

<p>In a competitive market, buyers may use stronger offers, shorter deadlines, or even escalation clauses. In a slower market, you may have more room to negotiate on price or repairs.</p>

<p>Typical time: <strong>1–7 days</strong></p>

<p>This part can move fast, especially if there are multiple offers. Sometimes the seller responds in hours. Other times there is back-and-forth over price, repairs, or closing terms.</p>

<p>The important thing is to stay focused. A good offer is not just about the number. It is also about the <strong>terms</strong>, because those terms can make your deal more appealing and help you move through the process more quickly.</p>

<h3 id="step-d-inspections-appraisal-and-contingencies">Inspections, Appraisal, and Contingencies</h3>

<p>After your offer is accepted, the home usually goes through inspection and appraisal. The inspection helps you understand the condition of the property. The appraisal helps the lender confirm the home is worth the loan amount.</p>

<p>If the inspection reveals problems, you may negotiate repairs, request credits, or walk away if your contract allows it. If the appraisal comes in low, you may need to renegotiate the price or cover the difference with cash.</p>

<p>Typical time: <strong>1–3 weeks</strong></p>

<p>This stage can feel like a pause, but it is one of the most important parts of the process. It protects you from overpaying and helps you avoid major surprises later.</p>

<p>Delays here are often caused by inspector availability, repair scheduling, or slow responses during negotiation. If you want to keep the deal moving, be quick about reviewing reports and making decisions.</p>

<h3 id="step-e-mortgage-underwriting-and-final-loan-approval">Mortgage Underwriting and Final Loan Approval</h3>

<p>Underwriting is where the lender reviews your file in detail. They check your income, assets, employment, debt, credit, and the property itself. They may ask for extra documents or conditions before giving final approval.</p>

<p>Typical time: <strong>2–6 weeks</strong></p>

<p>This stage can be very quick if your paperwork is clean and your lender is organized. It can take longer if the lender needs updated pay stubs, explanations for bank deposits, or more information about your employment.</p>

<p>A lot of buyers think preapproval is the finish line. It is not. The lender still has to finalize the loan after the home is under contract. That is why staying responsive during underwriting matters so much.</p>

<h3 id="step-f-closing-and-possession">Closing and Possession</h3>

<p>Closing is the final step. You review and sign the paperwork, the lender funds the loan, and ownership transfers to you. In many cases, the final stretch moves fast once the lender clears all conditions.</p>

<p>Typical time: <strong>1–3 days to close once cleared</strong></p>

<p>The actual closing date is often set about <strong>30–45 days after the accepted offer</strong>, though shorter or longer timelines are possible. After that, you get the keys and take possession, either the same day or shortly after depending on the contract.</p>

<p>At this point, the long <strong>timeline</strong> turns into something real: your new home.</p>

<h3 id="visual-timeline-suggestion">Visual Timeline Suggestion</h3>

<p>A horizontal timeline graphic works very well here. Show the process from <strong>preapproval → search → offer → inspection/appraisal → underwriting → closing</strong> with average time ranges below each step. That makes the process easy to scan and easy to understand.</p>

<h2 id="market-and-personal-factors-that-change-the-timeline">Market and Personal Factors That Change the Timeline</h2>

<p>No two buyers follow the exact same path. Your <strong>timeline</strong> depends on both market conditions and personal circumstances. That is why some purchases feel quick and smooth, while others take much longer than expected.</p>

<p>Here are the biggest factors that can change the pace:</p>

<ul>

<li><strong>Seller timeline:</strong> If the seller needs extra time to move, your closing may be delayed.</li>

<li><strong>Local market speed:</strong> Hot markets move fast, while buyer’s markets often give you more time.</li>

<li><strong>Mortgage type:</strong> Government-backed loans like FHA or VA can involve extra steps compared with some conventional loans.</li>

<li><strong>Inspection and appraisal delays:</strong> Busy inspectors, appraisers, or repair contractors can slow the process.</li>

<li><strong>Title issues:</strong> Old liens, ownership questions, or paperwork problems can hold things up.</li>

<li><strong>Financing contingencies:</strong> Strong contingencies protect you, but they can also add more steps and waiting.</li>

<li><strong>Selling your current home:</strong> If you need to sell first, your timeline becomes more complex.</li>

<li><strong>Seasonal effects:</strong> Spring and summer often bring more buyers, more competition, and sometimes more scheduling delays.</li>

</ul>

<h4 id="geographic-differences-matter-too">Geographic Differences Matter Too</h4>

<p>The timeline can also shift depending on where you buy. In large cities, homes may sell fast and lenders may be busier. In rural areas, you may have fewer options, but you might also face longer travel times for inspections or fewer appraisers in the area. Local demand matters just as much as the property itself.</p>

<h4 id="legal-and-administrative-differences-by-region">Legal and Administrative Differences by Region</h4>

<p>Different states and regions also have different rules, closing customs, and required documents. In some places, attorneys play a larger role. In others, title companies handle much of the paperwork. Those differences can affect the <strong>time to close on a house</strong>, especially if you are buying across state lines or entering a market you do not know well.</p>

<h2 id="how-to-speed-up-buying-a-house">How to Speed Up Buying a House</h2>

<p>If your goal is to move faster, the best approach is preparation. Speed comes from making fewer decisions under pressure and reducing back-and-forth once you are under contract.</p>

<p>Here are the most effective ways to shorten your <strong>home buying timeline</strong>:</p>

<ul>

<li><strong>Get preapproved, not just prequalified.</strong><br />

Preapproval gives you a stronger starting point because a lender has reviewed your finances more carefully.</li>

<li><strong>Keep your documents ready.</strong><br />

Save pay stubs, tax returns, bank statements, and ID in one place so you can respond fast when the lender asks.</li>

<li><strong>Work with an experienced local agent and lender.</strong><br />

A strong local team knows the market, knows the process, and can help you avoid delays.</li>

<li><strong>Narrow your search criteria.</strong><br />

If you know your must-haves, you can skip homes that do not fit and focus on the right ones.</li>

<li><strong>Use saved searches and alerts.</strong><br />

The fastest buyers are usually the ones who see good listings early.</li>

<li><strong>Be flexible on closing dates when possible.</strong><br />

Small changes in your timing can make your offer more attractive.</li>

<li><strong>Order inspections quickly and stay ready for repairs.</strong><br />

If you already have contractor contacts, you can make faster decisions after the inspection report.</li>

<li><strong>Consider bridge options if you are selling first.</strong><br />

These can help you manage timing between selling one home and buying another.</li>

</ul>

<p>A helpful content upgrade here is a <strong>downloadable checklist</strong> with all the steps buyers should complete before making an offer. That can turn a complicated process into a simple action plan.</p>

<p><strong>Inline CTA suggestion:</strong> If you want to stay organized, download the free home-buying timeline checklist or book a consultation to estimate your move-in date.</p>

<h2 id="common-delays-and-how-to-avoid-them">Common Delays and How to Avoid Them</h2>

<p>Even a well-planned purchase can slow down. The key is not to expect perfection. The key is to know where delays usually happen and how to reduce the risk.</p>

<h3 id="1-mortgage-underwriting-conditions">Mortgage Underwriting Conditions</h3>

<p>Underwriters may ask for more documents after reviewing your file. This can slow the deal if you respond late.</p>

<p><strong>How to avoid it:</strong> Send documents quickly, keep your financial records clean, and avoid major financial changes during the process.</p>

<h3 id="2-appraisal-gaps">Appraisal Gaps</h3>

<p>If the appraised value comes in lower than the purchase price, the lender may not approve the full loan amount.</p>

<p><strong>How to avoid it:</strong> Work with an agent who knows local pricing and prepare for possible negotiation if the appraisal is low.</p>

<h3 id="3-inspection-surprises">Inspection Surprises</h3>

<p>Inspections can uncover leaks, roof problems, electrical issues, or other repairs.</p>

<p><strong>How to avoid it:</strong> Do not skip the inspection unless you fully understand the risk. Read the report carefully and respond quickly.</p>

<h3 id="4-title-issues">Title Issues</h3>

<p>A title problem can stop closing until ownership questions or liens are resolved.</p>

<p><strong>How to avoid it:</strong> Use a reputable title company and let the title search happen as early as possible.</p>

<h3 id="5-seller-delays">Seller Delays</h3>

<p>Sometimes the seller needs more time because they have not found their next home yet.</p>

<p><strong>How to avoid it:</strong> Be open to flexible closing terms and ask your agent to understand the seller’s timeline before you offer.</p>

<h3 id="6-legal-or-administrative-issues">Legal or Administrative Issues</h3>

<p>Paperwork mistakes, missing signatures, or regional legal requirements can add time.</p>

<p><strong>How to avoid it:</strong> Double-check every document and work with professionals who know your local process.</p>

<p>Most delays do not come from one big disaster. They come from small slowdowns that stack up. A smart buyer stays organized and communicates often.</p>

<h2 id="real-world-example-timelines">Real-World Example Timelines</h2>

<p>Here are three simple examples to help you picture how the process can actually unfold.</p>

<h3 id="scenario-1-smooth-well-prepared-buyer-in-a-balanced-market">Scenario 1: Smooth, Well-Prepared Buyer in a Balanced Market</h3>

<p>This buyer has stable income, a strong credit score, and a full preapproval ready before the search begins. They tour homes for about three weeks, make one offer, and move into underwriting without major issues.</p>

<p><strong>Estimated total timeline:</strong> <strong>6–10 weeks</strong></p>

<p>This is one of the most realistic “smooth purchase” timelines. It works best when the buyer is decisive, the lender is responsive, and the seller does not need special timing.</p>

<h3 id="scenario-2-competitive-market-with-bidding-pressure">Competitive Market with Bidding Pressure</h3>

<p>This buyer finds homes quickly but faces multiple offers on several properties. They may need to move faster on decisions, shorten contingency periods, or offer more flexible terms to stay competitive.</p>

<p><strong>Estimated timeline:</strong> <strong>4–6 weeks from offer to close</strong>, though the search itself could be short or long depending on competition.</p>

<p>In this case, the offer stage is more intense, but the actual closing can still happen on a normal schedule if everything lines up.</p>

<h3 id="scenario-3-selling-and-buying-at-the-same-time">Selling and Buying at the Same Time</h3>

<p>This buyer must sell their current home before or around the same time they buy the next one. That means they may need to coordinate showings, offers, inspections, and closing dates for two properties.</p>

<p><strong>Estimated total timeline:</strong> <strong>3–6 months</strong></p>

<p>This scenario usually takes longer because there are more moving pieces. Buyers often use a sale contingency, rent-back agreement, or bridge solution to keep the process manageable.</p>

<p>If you are in this situation, your timeline is not just about the new home. It is about the <strong>whole transition</strong>.</p>

<h2 id="cost-and-timeline-trade-offs">Cost and Timeline Trade-Offs</h2>

<p>In real estate, saving time often costs more money. That does not always mean the extra cost is not worth it. It just means you need to know what you are paying for.</p>

<p>For example, you may pay for:</p>

<ul>

<li>An <strong>appraisal rush fee</strong></li>

<li>A more expensive but faster local lender</li>

<li>Faster inspection scheduling</li>

<li>Extra services that help your file move more smoothly</li>

</ul>

<p>Some buyers also choose appraisal waivers or stronger offers that reduce delays. Those choices may help speed up the process, but they can also reduce your leverage or increase your risk.</p>

<p>That is the trade-off. If you rush too much, you may miss inspection issues, overpay, or accept weak terms. If you move too slowly, you may lose the home you want.</p>

<p>The best approach is to balance speed with caution. A good buyer is not only fast. A good buyer is also prepared, careful, and informed.</p>

<h2 id="checklist-week-by-week-guide-for-a-10-week-buy">Checklist: Week-by-Week Guide for a 10-Week Buy</h2>

<p>If you want a simple planning tool, here is a practical <strong>10-week home buying timeline</strong>.</p>

<h3 id="week-1-2-finances-and-preapproval">Week 1–2: Finances and Preapproval</h3>

<ul>

<li>Review your budget</li>

<li>Check your credit</li>

<li>Gather financial documents</li>

<li>Get preapproved</li>

<li>Choose your agent and lender</li>

</ul>

<h3 id="week-3-4-active-search-begins">Week 3–4: Active Search Begins</h3>

<ul>

<li>Set search alerts</li>

<li>Tour homes</li>

<li>Compare neighborhoods</li>

<li>Refine your must-have list</li>

<li>Adjust your budget if needed</li>

</ul>

<h3 id="week-5-6-offers-and-negotiation">Week 5–6: Offers and Negotiation</h3>

<ul>

<li>Review comps</li>

<li>Write and submit offers</li>

<li>Respond to counteroffers</li>

<li>Finalize contract terms</li>

<li>Stay ready with backup choices</li>

</ul>

<h3 id="week-7-8-inspection-appraisal-and-underwriting">Week 7–8: Inspection, Appraisal, and Underwriting</h3>

<ul>

<li>Schedule inspection</li>

<li>Review the report</li>

<li>Request repairs or credits if needed</li>

<li>Submit lender documents</li>

<li>Track underwriting conditions</li>

</ul>

<h3 id="week-9-10-closing-and-move-planning">Week 9–10: Closing and Move Planning</h3>

<ul>

<li>Complete final walkthrough</li>

<li>Review closing disclosure</li>

<li>Transfer funds</li>

<li>Sign final paperwork</li>

<li>Arrange movers and utilities</li>

</ul>

<p>This simple plan works well as a printable checklist or downloadable PDF. It also helps buyers understand that the process is a series of small actions, not one giant event.</p>

<h2 id="faq">FAQ</h2>

<h3 id="how-long-does-it-take-to-buy-a-house-from-searching-to-keys-">How long does it take to buy a house from searching to keys?</h3>

<p>Most buyers take <strong>6–16 weeks</strong> from active search to getting the keys, but it can be faster or slower depending on the market and financing.</p>

<h3 id="how-long-does-mortgage-approval-take-">How long does mortgage approval take?</h3>

<p>Mortgage approval usually takes <strong>2–6 weeks</strong> after your offer is accepted, though preapproval before <a href="https://comeawayhome.co.uk/can-i-afford-a-500k-house/">house</a> hunting can happen much sooner.</p>

<h3 id="can-i-close-in-2-weeks-">Can I close in 2 weeks?</h3>

<p>Yes, but it is not common. A two-week closing is more realistic if you have strong finances, a simple loan, a fast lender, and a seller who wants a quick deal.</p>

<h3 id="does-getting-preapproved-speed-up-closing-">Does getting preapproved speed up closing?</h3>

<p>Yes. <strong>Preapproval</strong> helps speed things up because the lender has already reviewed your finances, so there is less to do after you go under contract.</p>

<h3 id="what-causes-the-biggest-delays-when-buying-a-house-">What causes the biggest delays when buying a house?</h3>

<p>The biggest delays usually come from <strong>underwriting conditions, appraisal gaps, inspection issues, title problems, and seller timing</strong>.</p>

<h3 id="how-long-after-acceptance-do-i-get-the-keys-">How long after acceptance do I get the keys?</h3>

<p>In many cases, you get the keys <strong>30–45 days after acceptance</strong>, though some closings happen sooner and some take longer.</p>

<h3 id="how-long-does-it-take-to-buy-a-house-with-a-mortgage-">How long does it take to buy a house with a mortgage?</h3>

<p>With a mortgage, the process often takes <strong>30–60 days after an accepted offer</strong>, plus extra time for searching and preparation before that.</p>

<h3 id="how-long-does-it-take-to-buy-a-house-if-you-have-to-sell-yours-">How long does it take to buy a house if you have to sell yours?</h3>

<p>If you need to sell first, expect the full process to take <strong>3–6 months</strong>, depending on how quickly your current home sells and how the two closings are coordinated.</p>

<h2 id="internal-and-external-link-recommendations">Internal and External Link Recommendations</h2>

<p>Since this article should stay clean and helpful, use <strong>internal links</strong> where they naturally support the reader’s next step. Good internal link ideas include:</p>

<ul>

<li>A <strong>mortgage calculator</strong></li>

<li>A guide on <strong>how to get mortgage preapproval</strong></li>

<li>A page on <strong>home-buying services</strong></li>

<li>Neighborhood or city guides</li>

<li>Seller services if readers need to sell first</li>

<li>Related articles on closing costs, inspection tips, or first-time buyer programs</li>

</ul>

<p>For <strong>external links</strong>, use authoritative sources only, such as:</p>

<ul>

<li>Government housing resources</li>

<li>Major lender education pages</li>

<li>Local real estate board guidance</li>

<li>State or regional housing agencies</li>

</ul>

<p><strong>Anchor text examples:</strong></p>

<ul>

<li>“mortgage calculator”</li>

<li>“how to get mortgage preapproval”</li>

<li>“first-time buyer guide”</li>

<li>“home inspection checklist”</li>

<li>“local neighborhood guide”</li>

</ul>

<h2 id="images-charts-and-ctas">Images, Charts, and CTAs</h2>

<p>This article will perform better if you add a few strong visuals. A <strong>timeline infographic</strong> is the best choice because it makes the buying process easy to scan. You can also add:</p>

<ul>

<li>A checklist image</li>

<li>A redacted sample preapproval document</li>

<li>A sample inspection checklist</li>

<li>A comparison table image showing timeline ranges by stage</li>

</ul>

<p>A stacked bar chart or timeline graphic can show the average time spent in each stage of the purchase. That makes the article feel practical and polished.</p>

<p>For CTAs, consider these options:</p>

<ul>

<li><strong>Get the free timeline checklist</strong></li>

<li><strong>Book a consultation</strong></li>

<li><strong>Calculate your mortgage timeline</strong></li>

<li><strong>Sign up for property alerts</strong></li>

</ul>

<p>A strong placement is right after the “How to speed up buying a house” section, when the reader is ready to act. Another good spot is just before the FAQ, where readers often pause and want a next step.</p>

<h2 id="author-notes-and-quoting-experts">Author Notes and Quoting Experts</h2>

<p>If you want to strengthen trust, interview a <strong>local lender</strong> and a <strong>top real estate agent</strong>. A short quote from each one can make the article feel more grounded and current.</p>

<p>You can ask them for:</p>

<ul>

<li>Average local days to close</li>

<li>Common underwriting delays</li>

<li>How often appraisal problems come up</li>

<li>Whether buyers in your market are closing faster or slower this year</li>

</ul>

<p>If you cite timing data, use local MLS figures or lender reports when possible. That adds credibility and helps readers understand the <strong>real</strong> timeline in their area, not just a national average.</p>

<h2 id="final-takeaway">Final Takeaway</h2>

<p>So, <strong>how long does it take to buy a house</strong>? The short answer is that it usually takes <strong>weeks to months</strong>, not days. The exact timing depends on how ready you are, how competitive your market is, and how smooth the financing and closing stages go.</p>

<p>If you prepare early, stay organized, and work with the right team, you can move through the process much faster and with less stress. The goal is not just to buy quickly. The goal is to buy smart, stay in control, and feel confident at every step.</p>

<p><a href="https://comeawayhome.co.uk/">House</a></p>

If you have been asking how long does it take to buy a house, the honest answer is this: it can take a few weeks to several months, depending on your finances, the market, and whether you need to sell a home first. Some buyers move fast and close in about 30 days. Others need more time to search, compare options, get financing ready, and work through inspections and underwriting.

That may sound vague, but there is a good reason for it. Buying a home is not one single task. It is a chain of steps, and each step can move quickly or slowly depending on the situation. A buyer with a strong credit profile, a clear budget, and a responsive lender will usually move faster than someone still sorting out documents or waiting on a sale to finish.

In this guide, you will get a clear timeline for every major stage of the home-buying process. You will also see what usually slows buyers down, what can speed things up, and how the timeline changes in real life. We will walk through preapproval, home search, offers, inspections, underwriting, and closing in simple language.

If you want to plan ahead with confidence, this article will give you a practical home buying timeline you can actually use.

What “How Long Does It Take to Buy a House” Really Means

The phrase how long does it take to buy a house can mean different things to different people. That is why you may hear very different answers online. One person may be talking about the time it takes to find the right home. Another may mean the time from an accepted offer to closing. Someone else may be asking about the full process, including mortgage preapproval and selling their current home.

That difference matters. A buyer who already has financing ready may only need to focus on search, offer, and closing. A first-time buyer may need extra time for budgeting, document gathering, and lender review. If you are selling a home too, your timeline can stretch even more.

Here is a simple way to think about it.

| What the timeline means |

Typical time range |

What it includes |

| Searching only |

2–12+ weeks |

Browsing homes, touring, comparing neighborhoods, and choosing a property |

| Offer to close |

30–45 days on average |

Offer, negotiation, inspection, appraisal, underwriting, and closing |

| Full buying process |

6–16+ weeks |

Finances, preapproval, search, offer, mortgage approval, and closing |

| Buying while selling |

3–6 months total |

Listing your current home, finding a buyer, and coordinating both deals |

So when someone asks about the timeline, the best answer is usually, “It depends on which part of the process you mean.” That is the most useful way to look at it.

Typical Timeline: Step-by-Step

The averages below reflect a fairly typical market. In a hot market, things can move faster. In a slower market or a more complicated loan scenario, the process can take longer.

Financial Prep and Mortgage Preapproval

Before you start touring homes, you need a clear picture of what you can afford. This stage usually includes checking your credit, setting a budget, estimating your down payment, and gathering documents like pay stubs, tax returns, bank statements, and ID.

A strong preapproval is more than a rough estimate. It tells sellers and agents that a lender has reviewed your finances and believes you are qualified for a certain loan amount. That can make your offer stronger later.

Typical time: 1–3 weeks

If you already have your paperwork ready, this stage can move quickly. If you have credit issues, inconsistent income, or missing records, it can take longer. This is also a good time to use a mortgage calculator or an internal financing guide on your site to help readers estimate their monthly payment and price range.

A simple rule is this: the better prepared you are now, the smoother the rest of the timeline becomes.

Home Search

Once your finances are ready, the search begins. This is often the most flexible part of the process because it depends on your priorities, your market, and how fast you make decisions. Some buyers find a home in a weekend. Others take months because they are waiting for the right neighborhood, layout, or price.

During this stage, you may look at neighborhoods, school zones, commute times, and property conditions. You may tour homes in person, use virtual tours, and compare features with your must-have list. A good agent can save time here by filtering out homes that do not fit your budget or goals.

Typical time: 2–12+ weeks

A few ways to shorten the search:

- Decide what you must have versus what is only nice to have.

- Set up nightly property alerts so new listings reach you fast.

- Be ready to tour quickly when a strong match appears.

- Keep your budget realistic so you do not waste time on homes that are out of reach.

This stage is where many buyers either gain momentum or lose it. Clear priorities make a big difference.

Making an Offer and Negotiation

Once you find the right property, the next step is the offer. Your agent will usually help you look at recent comparable sales, or comps, to decide on a fair price. You may also choose contingencies, such as financing, inspection, or appraisal protections.

In a competitive market, buyers may use stronger offers, shorter deadlines, or even escalation clauses. In a slower market, you may have more room to negotiate on price or repairs.

Typical time: 1–7 days

This part can move fast, especially if there are multiple offers. Sometimes the seller responds in hours. Other times there is back-and-forth over price, repairs, or closing terms.

The important thing is to stay focused. A good offer is not just about the number. It is also about the terms, because those terms can make your deal more appealing and help you move through the process more quickly.

Inspections, Appraisal, and Contingencies

After your offer is accepted, the home usually goes through inspection and appraisal. The inspection helps you understand the condition of the property. The appraisal helps the lender confirm the home is worth the loan amount.

If the inspection reveals problems, you may negotiate repairs, request credits, or walk away if your contract allows it. If the appraisal comes in low, you may need to renegotiate the price or cover the difference with cash.

Typical time: 1–3 weeks

This stage can feel like a pause, but it is one of the most important parts of the process. It protects you from overpaying and helps you avoid major surprises later.

Delays here are often caused by inspector availability, repair scheduling, or slow responses during negotiation. If you want to keep the deal moving, be quick about reviewing reports and making decisions.

Mortgage Underwriting and Final Loan Approval

Underwriting is where the lender reviews your file in detail. They check your income, assets, employment, debt, credit, and the property itself. They may ask for extra documents or conditions before giving final approval.

Typical time: 2–6 weeks

This stage can be very quick if your paperwork is clean and your lender is organized. It can take longer if the lender needs updated pay stubs, explanations for bank deposits, or more information about your employment.

A lot of buyers think preapproval is the finish line. It is not. The lender still has to finalize the loan after the home is under contract. That is why staying responsive during underwriting matters so much.

Closing and Possession

Closing is the final step. You review and sign the paperwork, the lender funds the loan, and ownership transfers to you. In many cases, the final stretch moves fast once the lender clears all conditions.

Typical time: 1–3 days to close once cleared

The actual closing date is often set about 30–45 days after the accepted offer, though shorter or longer timelines are possible. After that, you get the keys and take possession, either the same day or shortly after depending on the contract.

At this point, the long timeline turns into something real: your new home.

Visual Timeline Suggestion

A horizontal timeline graphic works very well here. Show the process from preapproval → search → offer → inspection/appraisal → underwriting → closing with average time ranges below each step. That makes the process easy to scan and easy to understand.

Market and Personal Factors That Change the Timeline

No two buyers follow the exact same path. Your timeline depends on both market conditions and personal circumstances. That is why some purchases feel quick and smooth, while others take much longer than expected.

Here are the biggest factors that can change the pace:

- Seller timeline: If the seller needs extra time to move, your closing may be delayed.

- Local market speed: Hot markets move fast, while buyer’s markets often give you more time.

- Mortgage type: Government-backed loans like FHA or VA can involve extra steps compared with some conventional loans.

- Inspection and appraisal delays: Busy inspectors, appraisers, or repair contractors can slow the process.

- Title issues: Old liens, ownership questions, or paperwork problems can hold things up.

- Financing contingencies: Strong contingencies protect you, but they can also add more steps and waiting.

- Selling your current home: If you need to sell first, your timeline becomes more complex.

- Seasonal effects: Spring and summer often bring more buyers, more competition, and sometimes more scheduling delays.

Geographic Differences Matter Too

The timeline can also shift depending on where you buy. In large cities, homes may sell fast and lenders may be busier. In rural areas, you may have fewer options, but you might also face longer travel times for inspections or fewer appraisers in the area. Local demand matters just as much as the property itself.

Legal and Administrative Differences by Region

Different states and regions also have different rules, closing customs, and required documents. In some places, attorneys play a larger role. In others, title companies handle much of the paperwork. Those differences can affect the time to close on a house, especially if you are buying across state lines or entering a market you do not know well.

How to Speed Up Buying a House

If your goal is to move faster, the best approach is preparation. Speed comes from making fewer decisions under pressure and reducing back-and-forth once you are under contract.

Here are the most effective ways to shorten your home buying timeline:

- Get preapproved, not just prequalified.

Preapproval gives you a stronger starting point because a lender has reviewed your finances more carefully.

- Keep your documents ready.

Save pay stubs, tax returns, bank statements, and ID in one place so you can respond fast when the lender asks.

- Work with an experienced local agent and lender.

A strong local team knows the market, knows the process, and can help you avoid delays.

- Narrow your search criteria.

If you know your must-haves, you can skip homes that do not fit and focus on the right ones.

- Use saved searches and alerts.

The fastest buyers are usually the ones who see good listings early.

- Be flexible on closing dates when possible.

Small changes in your timing can make your offer more attractive.

- Order inspections quickly and stay ready for repairs.

If you already have contractor contacts, you can make faster decisions after the inspection report.

- Consider bridge options if you are selling first.

These can help you manage timing between selling one home and buying another.

A helpful content upgrade here is a downloadable checklist with all the steps buyers should complete before making an offer. That can turn a complicated process into a simple action plan.

Inline CTA suggestion: If you want to stay organized, download the free home-buying timeline checklist or book a consultation to estimate your move-in date.

Common Delays and How to Avoid Them

Even a well-planned purchase can slow down. The key is not to expect perfection. The key is to know where delays usually happen and how to reduce the risk.

Mortgage Underwriting Conditions

Underwriters may ask for more documents after reviewing your file. This can slow the deal if you respond late.

How to avoid it: Send documents quickly, keep your financial records clean, and avoid major financial changes during the process.

Appraisal Gaps

If the appraised value comes in lower than the purchase price, the lender may not approve the full loan amount.

How to avoid it: Work with an agent who knows local pricing and prepare for possible negotiation if the appraisal is low.

Inspection Surprises

Inspections can uncover leaks, roof problems, electrical issues, or other repairs.

How to avoid it: Do not skip the inspection unless you fully understand the risk. Read the report carefully and respond quickly.

Title Issues

A title problem can stop closing until ownership questions or liens are resolved.

How to avoid it: Use a reputable title company and let the title search happen as early as possible.

Seller Delays

Sometimes the seller needs more time because they have not found their next home yet.

How to avoid it: Be open to flexible closing terms and ask your agent to understand the seller’s timeline before you offer.

Legal or Administrative Issues

Paperwork mistakes, missing signatures, or regional legal requirements can add time.

How to avoid it: Double-check every document and work with professionals who know your local process.

Most delays do not come from one big disaster. They come from small slowdowns that stack up. A smart buyer stays organized and communicates often.

Real-World Example Timelines

Here are three simple examples to help you picture how the process can actually unfold.

Scenario 1: Smooth, Well-Prepared Buyer in a Balanced Market

This buyer has stable income, a strong credit score, and a full preapproval ready before the search begins. They tour homes for about three weeks, make one offer, and move into underwriting without major issues.

Estimated total timeline: 6–10 weeks

This is one of the most realistic “smooth purchase” timelines. It works best when the buyer is decisive, the lender is responsive, and the seller does not need special timing.

Competitive Market with Bidding Pressure

This buyer finds homes quickly but faces multiple offers on several properties. They may need to move faster on decisions, shorten contingency periods, or offer more flexible terms to stay competitive.

Estimated timeline: 4–6 weeks from offer to close, though the search itself could be short or long depending on competition.

In this case, the offer stage is more intense, but the actual closing can still happen on a normal schedule if everything lines up.

Selling and Buying at the Same Time

This buyer must sell their current home before or around the same time they buy the next one. That means they may need to coordinate showings, offers, inspections, and closing dates for two properties.

Estimated total timeline: 3–6 months

This scenario usually takes longer because there are more moving pieces. Buyers often use a sale contingency, rent-back agreement, or bridge solution to keep the process manageable.

If you are in this situation, your timeline is not just about the new home. It is about the whole transition.

Cost and Timeline Trade-Offs

In real estate, saving time often costs more money. That does not always mean the extra cost is not worth it. It just means you need to know what you are paying for.

For example, you may pay for:

- An appraisal rush fee

- A more expensive but faster local lender

- Faster inspection scheduling

- Extra services that help your file move more smoothly

Some buyers also choose appraisal waivers or stronger offers that reduce delays. Those choices may help speed up the process, but they can also reduce your leverage or increase your risk.

That is the trade-off. If you rush too much, you may miss inspection issues, overpay, or accept weak terms. If you move too slowly, you may lose the home you want.

The best approach is to balance speed with caution. A good buyer is not only fast. A good buyer is also prepared, careful, and informed.

Checklist: Week-by-Week Guide for a 10-Week Buy

If you want a simple planning tool, here is a practical 10-week home buying timeline.

Week 1–2: Finances and Preapproval

- Review your budget

- Check your credit

- Gather financial documents

- Get preapproved

- Choose your agent and lender

Week 3–4: Active Search Begins

- Set search alerts

- Tour homes

- Compare neighborhoods

- Refine your must-have list

- Adjust your budget if needed

Week 5–6: Offers and Negotiation

- Review comps

- Write and submit offers

- Respond to counteroffers

- Finalize contract terms

- Stay ready with backup choices

Week 7–8: Inspection, Appraisal, and Underwriting

- Schedule inspection

- Review the report

- Request repairs or credits if needed

- Submit lender documents

- Track underwriting conditions

Week 9–10: Closing and Move Planning

- Complete final walkthrough

- Review closing disclosure

- Transfer funds

- Sign final paperwork

- Arrange movers and utilities

This simple plan works well as a printable checklist or downloadable PDF. It also helps buyers understand that the process is a series of small actions, not one giant event.

FAQ

How long does it take to buy a house from searching to keys?

Most buyers take 6–16 weeks from active search to getting the keys, but it can be faster or slower depending on the market and financing.

How long does mortgage approval take?

Mortgage approval usually takes 2–6 weeks after your offer is accepted, though preapproval before house hunting can happen much sooner.

Can I close in 2 weeks?

Yes, but it is not common. A two-week closing is more realistic if you have strong finances, a simple loan, a fast lender, and a seller who wants a quick deal.

Does getting preapproved speed up closing?

Yes. Preapproval helps speed things up because the lender has already reviewed your finances, so there is less to do after you go under contract.

What causes the biggest delays when buying a house?

The biggest delays usually come from underwriting conditions, appraisal gaps, inspection issues, title problems, and seller timing.

How long after acceptance do I get the keys?

In many cases, you get the keys 30–45 days after acceptance, though some closings happen sooner and some take longer.

How long does it take to buy a house with a mortgage?

With a mortgage, the process often takes 30–60 days after an accepted offer, plus extra time for searching and preparation before that.

How long does it take to buy a house if you have to sell yours?

If you need to sell first, expect the full process to take 3–6 months, depending on how quickly your current home sells and how the two closings are coordinated.

Internal and External Link Recommendations

Since this article should stay clean and helpful, use internal links where they naturally support the reader’s next step. Good internal link ideas include:

- A mortgage calculator

- A guide on how to get mortgage preapproval

- A page on home-buying services

- Neighborhood or city guides

- Seller services if readers need to sell first

- Related articles on closing costs, inspection tips, or first-time buyer programs

For external links, use authoritative sources only, such as:

- Government housing resources

- Major lender education pages

- Local real estate board guidance

- State or regional housing agencies

Anchor text examples:

- “mortgage calculator”

- “how to get mortgage preapproval”

- “first-time buyer guide”

- “home inspection checklist”

- “local neighborhood guide”

Images, Charts, and CTAs

This article will perform better if you add a few strong visuals. A timeline infographic is the best choice because it makes the buying process easy to scan. You can also add:

- A checklist image

- A redacted sample preapproval document

- A sample inspection checklist

- A comparison table image showing timeline ranges by stage

A stacked bar chart or timeline graphic can show the average time spent in each stage of the purchase. That makes the article feel practical and polished.

For CTAs, consider these options:

- Get the free timeline checklist

- Book a consultation

- Calculate your mortgage timeline

- Sign up for property alerts

A strong placement is right after the “How to speed up buying a house” section, when the reader is ready to act. Another good spot is just before the FAQ, where readers often pause and want a next step.

Author Notes and Quoting Experts

If you want to strengthen trust, interview a local lender and a top real estate agent. A short quote from each one can make the article feel more grounded and current.

You can ask them for:

- Average local days to close

- Common underwriting delays

- How often appraisal problems come up

- Whether buyers in your market are closing faster or slower this year

If you cite timing data, use local MLS figures or lender reports when possible. That adds credibility and helps readers understand the real timeline in their area, not just a national average.

Final Takeaway

So, how long does it take to buy a house? The short answer is that it usually takes weeks to months, not days. The exact timing depends on how ready you are, how competitive your market is, and how smooth the financing and closing stages go.

If you prepare early, stay organized, and work with the right team, you can move through the process much faster and with less stress. The goal is not just to buy quickly. The goal is to buy smart, stay in control, and feel confident at every step.

House