<p>If you are asking <a href="https://www.reddit.com/r/FinancialPlanning/comments/13nxg9e/can_i_afford_a_500k_house/"><strong>can i afford a 500k house</strong></a>, you are already thinking the right way. A house price is only the starting point. The real question is whether the <strong>monthly payment</strong>, your <strong>upfront cash</strong>, and your <strong>overall budget</strong> all fit together without putting pressure on the rest of your life.</p>

<p>This guide breaks everything down in simple terms. You will learn how to estimate the monthly payment, how much cash you need before closing, how taxes and insurance change the real cost, and how lenders decide whether you qualify. If you are a first-time buyer, moving up to a larger home, or planning a purchase in 2026, this article will help you run the numbers with more confidence.</p>

<h4 id="quick-answer-can-i-afford-a-500k-house-">Can I afford a $500K house?</h4>

<p>The short answer is: <strong>maybe, but it depends on your income, debts, down payment, and the local cost of owning the home</strong>.</p>

<p>A $500,000 house can be affordable for one household and too expensive for another. A buyer with a strong income, low debt, and a healthy down payment may feel comfortable. A buyer with student loans, car payments, credit card balances, or little savings may feel squeezed even if the house looks manageable on paper.</p>

<p>So, if you are wondering <strong>can i afford a 500k house</strong>, the best approach is to look at the full picture:</p>

<ul>

<li><strong>Monthly principal and interest</strong></li>

<li><strong>Property taxes</strong></li>

<li><strong>Homeowners insurance</strong></li>

<li><strong>HOA fees</strong></li>

<li><strong>Private mortgage insurance, if needed</strong></li>

<li><strong>Upfront cash for the down payment and closing costs</strong></li>

<li><strong>Your debt-to-income ratio</strong></li>

<li><strong>Your emergency savings</strong></li>

</ul>

<p>Read on, and we will walk through each part step by step.</p>

<h2 id="how-mortgage-pricing-works-principal-interest-and-time">How mortgage pricing works: principal, interest, and time</h2>

<p>When you buy a home with a mortgage, you borrow money from a lender and pay it back over time. That payment has two main parts:</p>

<ul>

<li><strong>Principal</strong>: the amount you borrowed</li>

<li><strong>Interest</strong>: the cost of borrowing that money</li>

</ul>

<p>At the start of the loan, a larger share of your payment goes toward interest. Over time, more of it goes toward principal. This is called <strong>amortization</strong>. It is one reason a 30-year mortgage feels very different from a 15-year mortgage.</p>

<h3 id="the-basic-idea-behind-a-mortgage-for-a-500k-house">The basic idea behind a mortgage for a $500K house</h3>

<p>If you buy a <strong>$500k house</strong>, your mortgage amount depends on how much you put down.</p>

<p>For example:</p>

<ul>

<li><strong>20% down</strong> on $500,000 = <strong>$100,000 down payment</strong></li>

<li>Loan amount = <strong>$400,000</strong></li>

<li><strong>10% down</strong> = <strong>$50,000 down payment</strong></li>

<li>Loan amount = <strong>$450,000</strong></li>

<li><strong>3% down</strong> = <strong>$15,000 down payment</strong></li>

<li>Loan amount = <strong>$485,000</strong></li>

</ul>

<p>The more you put down, the less you borrow. That usually lowers your monthly payment and can reduce or eliminate PMI.</p>

<h3 id="30-year-mortgage-vs-15-year-mortgage">30-year mortgage vs. 15-year mortgage</h3>

<p>A <strong>30-year mortgage</strong> usually gives you the lowest monthly payment, which is why it is the most common choice for many buyers. A <strong>15-year mortgage</strong> has a much higher monthly payment, but you pay off the home faster and usually pay less interest overall.</p>

<p>Here is the tradeoff in plain language:</p>

<ul>

<li><strong>30-year loan</strong>: easier on monthly cash flow, more total interest over time</li>

<li><strong>15-year loan</strong>: higher monthly payment, less total interest, faster payoff</li>

</ul>

<p>For many buyers asking <strong>can i afford a 500k house</strong>, the 30-year option is the more realistic starting point because it creates more breathing room.</p>

<h3 id="why-interest-rates-matter-so-much">Why interest rates matter so much</h3>

<p>Even a small rate change can make a big difference. In a high-rate environment, your monthly payment can jump quickly. As of <strong>May 2026</strong>, many buyers are still seeing mortgage rates that vary based on credit score, loan type, and market conditions. Instead of focusing on one exact number, it is smarter to run a few scenarios.</p>

<p>That is why a <strong>500k house mortgage calculator</strong> is so useful. It lets you compare payments at different rates and down payments before you make a big decision.</p>

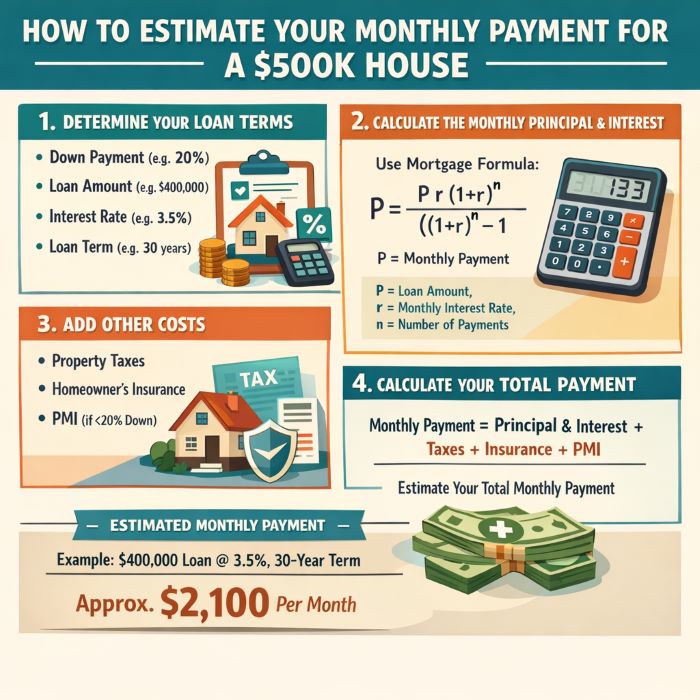

<h2 id="how-to-estimate-your-monthly-payment-for-a-500k-house">How to estimate your monthly payment for a $500K house</h2>

<p><img class="aligncenter wp-image-7131 size-full" src="https://comeawayhome.co.uk/wp-content/uploads/2026/05/0a6b0b74-4c85-4a15-83eb-61148f832658.jpg" alt="can i afford a 500k house" width="700" height="700" /></p>

<p>A home’s sticker price is not your monthly payment. To estimate what you will really pay each month, work through these steps:</p>

<ol>

<li><strong>Start with the purchase price</strong></li>

<li><strong>Subtract your down payment</strong></li>

<li><strong>Find the loan amount</strong></li>

<li><strong>Choose an interest rate</strong></li>

<li><strong>Choose a loan term</strong></li>

<li><strong>Add taxes, insurance, PMI, and HOA fees</strong></li>

</ol>

<p>Let us look at the most important part first: the mortgage payment itself.</p>

<h3 id="step-1-estimate-principal-and-interest">Estimate principal and interest</h3>

<p>The mortgage payment for a <strong>$500k <a href="https://comeawayhome.co.uk/how-to-set-thermostat-for-2-story-house-in-winter/">house</a></strong> depends heavily on your loan size and rate. Below are rough examples for a 30-year fixed mortgage. These numbers are <strong>approximate</strong> and meant for planning, not final underwriting.</p>

<h4 id="example-1-20-down">Example 1: 20% down</h4>

<ul>

<li>Purchase price: <strong>$500,000</strong></li>

<li>Down payment: <strong>$100,000</strong></li>

<li>Loan amount: <strong>$400,000</strong></li>

<li>Interest rate: <strong>6.0%</strong></li>

<li>Loan term: <strong>30 years</strong></li>

<li>Approximate principal and interest: <strong>$2,398 per month</strong></li>

</ul>

<h4 id="example-2-10-down">Example 2: 10% down</h4>

<ul>

<li>Purchase price: <strong>$500,000</strong></li>

<li>Down payment: <strong>$50,000</strong></li>

<li>Loan amount: <strong>$450,000</strong></li>

<li>Interest rate: <strong>6.0%</strong></li>

<li>Loan term: <strong>30 years</strong></li>

<li>Approximate principal and interest: <strong>$2,697 per month</strong></li>

</ul>

<h4 id="example-3-3-down">Example 3: 3% down</h4>

<ul>

<li>Purchase price: <strong>$500,000</strong></li>

<li>Down payment: <strong>$15,000</strong></li>

<li>Loan amount: <strong>$485,000</strong></li>

<li>Interest rate: <strong>6.0%</strong></li>

<li>Loan term: <strong>30 years</strong></li>

<li>Approximate principal and interest: <strong>$2,907 per month</strong></li>

</ul>

<h3 id="step-2-use-ranges-not-just-one-number">Use ranges, not just one number</h3>

<p>Rates move. Fees move. Insurance and taxes change by location. That is why it helps to think in ranges.</p>

<p>For a <strong>30-year mortgage on a $500k home</strong>, a common planning range for principal and interest might look something like this:</p>

<ul>

<li><strong>Lower end</strong>: around <strong>$2,300 to $2,600</strong></li>

<li><strong>Middle range</strong>: around <strong>$2,600 to $3,100</strong></li>

<li><strong>Higher end</strong>: above <strong>$3,100</strong> if rates are higher or the loan amount is larger</li>

</ul>

<p>If you want to answer <strong>can i afford a 500k house</strong> with confidence, you should use a mortgage calculator and test at least three different scenarios:</p>

<ul>

<li>a lower rate</li>

<li>a middle rate</li>

<li>a higher rate</li>

</ul>

<p>That way, you do not build your budget around the best-case outcome only.</p>

<h3 id="step-3-do-not-stop-at-principal-and-interest">Do not stop at principal and interest</h3>

<p>Many buyers focus on the mortgage payment and forget the rest. That can create a nasty surprise later. A home payment includes much more than the loan itself, and those extra costs can change the answer fast.</p>

<h2 id="add-recurring-housing-costs-taxes-insurance-hoa-and-pmi">Add recurring housing costs: taxes, insurance, HOA, and PMI</h2>

<p>When people ask <strong>how much is the monthly payment for a 500k house</strong>, they often mean the full housing cost, not just the loan.</p>

<p>Let us break down the costs that show up again and again.</p>

<h3 id="property-taxes">Property taxes</h3>

<p>Property taxes depend on your state, county, and city. In many places, they fall somewhere between <strong>0.7% and 2.0% of the home value per year</strong>.</p>

<p>For a <strong>$500,000 home</strong>, that could mean:</p>

<ul>

<li><strong>0.7%</strong> = <strong>$3,500 per year</strong> or about <strong>$292 per month</strong></li>

<li><strong>1.0%</strong> = <strong>$5,000 per year</strong> or about <strong>$417 per month</strong></li>

<li><strong>2.0%</strong> = <strong>$10,000 per year</strong> or about <strong>$833 per month</strong></li>

</ul>

<p>That is a huge difference. A house that looks affordable in one county may feel much more expensive in another simply because of taxes.</p>

<h3 id="homeowners-insurance">Homeowners insurance</h3>

<p>Homeowners insurance protects you against damage, theft, and certain disasters. Costs vary based on location, home age, coverage level, and risk factors like wind or fire exposure.</p>

<p>A rough planning range for a $500,000 home might be:</p>

<ul>

<li><strong>$100 to $250 per month</strong> in many areas</li>

<li>More in high-risk or high-cost areas</li>

</ul>

<p>If the home is older, in a storm-prone region, or has special coverage needs, insurance can run even higher.</p>

<h3 id="hoa-fees">HOA fees</h3>

<p>If the home is part of a homeowners association, you may owe HOA dues every month or quarter. These fees can be small or surprisingly large.</p>

<p>Common HOA ranges include:</p>

<ul>

<li><strong>$50 to $150 per month</strong> for a modest community</li>

<li><strong>$200 to $500+ per month</strong> for communities with more amenities</li>

</ul>

<p>HOA dues matter because they reduce how much room you have in your monthly budget. Two houses with the same price can have very different real costs if one has a high HOA and the other does not.</p>

<h3 id="pmi-private-mortgage-insurance">PMI: private mortgage insurance</h3>

<p>If you put down less than <strong>20%</strong>, you may need <strong>PMI</strong>. This protects the lender, not you. It often adds to your monthly payment until you build enough equity.</p>

<p>PMI cost varies, but a simple planning range could be:</p>

<ul>

<li><strong>$100 to $350 per month</strong></li>

<li>Sometimes more for smaller down payments or lower credit scores</li>

</ul>

<p>The exact cost depends on loan size, credit profile, and down payment amount.</p>

<h3 id="a-sample-total-monthly-housing-cost">A sample total monthly housing cost</h3>

<p>Here is what a full monthly picture might look like on a $500k home.</p>

<h4 id="example-total">Example total</h4>

<ul>

<li>Principal and interest: <strong>$2,398</strong></li>

<li>Property taxes: <strong>$417</strong></li>

<li>Homeowners insurance: <strong>$150</strong></li>

<li>HOA fee: <strong>$100</strong></li>

<li>PMI: <strong>$0</strong> if 20% down, or added if down payment is lower</li>

</ul>

<p>That gives you a total of about <strong>$3,065 per month</strong> with 20% down and no PMI.</p>

<p>If you had a smaller down payment and PMI, that same home could easily move closer to <strong>$3,200 to $3,500+ per month</strong>.</p>

<p>This is why the question <strong>can i afford a 500k house</strong> is never just about the sale price. It is about the full monthly burden.</p>

<h2 id="upfront-costs-to-buy-a-500k-house">Upfront costs to buy a $500K house</h2>

<p>A home purchase also requires cash before you even move in. Many buyers are surprised by how much they need beyond the down payment.</p>

<h3 id="down-payment">Down payment</h3>

<p>Your down payment is the chunk you pay upfront toward the purchase price.</p>

<p>Common options include:</p>

<ul>

<li><strong>20% down</strong>: avoids PMI in many cases and lowers your loan amount</li>

<li><strong>10% down</strong>: more accessible, but often includes PMI</li>

<li><strong>3% to 5% down</strong>: possible with certain loan programs, but monthly costs are usually higher</li>

</ul>

<p>For a <strong>$500k house</strong>, the down payment amounts look like this:</p>

<ul>

<li><strong>20%</strong> = <strong>$100,000</strong></li>

<li><strong>10%</strong> = <strong>$50,000</strong></li>

<li><strong>5%</strong> = <strong>$25,000</strong></li>

<li><strong>3%</strong> = <strong>$15,000</strong></li>

</ul>

<p>If you are trying to decide whether you can afford it, this is your first cash test. Just because you can qualify for a loan does not mean you can comfortably write the down payment check.</p>

<h3 id="closing-costs">Closing costs</h3>

<p>Closing costs are the fees you pay to finalize the purchase. They often include lender fees, title fees, appraisal costs, attorney fees in some states, and prepaid items.</p>

<p>A common range is <strong>2% to 5% of the purchase price</strong>.</p>

<p>For a <strong>$500,000 home</strong>, that means roughly:</p>

<ul>

<li><strong>2%</strong> = <strong>$10,000</strong></li>

<li><strong>3%</strong> = <strong>$15,000</strong></li>

<li><strong>5%</strong> = <strong>$25,000</strong></li>

</ul>

<p>That is a big number, and it sits on top of your down payment.</p>

<h3 id="prepaids-and-reserves">Prepaids and reserves</h3>

<p>You may also need money for:</p>

<ul>

<li><strong>Initial escrow deposits</strong></li>

<li><strong>Prepaid property taxes</strong></li>

<li><strong>Prepaid insurance premiums</strong></li>

<li><strong>Inspection fees</strong></li>

<li><strong>Appraisal fees</strong></li>

<li><strong>Moving costs</strong></li>

<li><strong>Small repairs or immediate improvements</strong></li>

</ul>

<p>These items may not feel as important as the down payment, but they can be the difference between a smooth closing and a stressful one.</p>

<h3 id="a-realistic-cash-to-close-example">A realistic cash-to-close example</h3>

<p>Let us say you buy a $500k house with 10% down.</p>

<ul>

<li>Down payment: <strong>$50,000</strong></li>

<li>Closing costs: <strong>$15,000</strong></li>

<li>Prepaids and escrow: <strong>$3,000 to $7,000</strong></li>

<li>Inspection and appraisal: <strong>$800 to $1,500</strong></li>

<li>Moving and immediate fixes: <strong>$2,000 to $5,000</strong></li>

</ul>

<p>Your total cash need could easily land around <strong>$70,000 or more</strong>.</p>

<p>That is why many buyers discover that the real challenge is not just qualifying for the mortgage. It is having enough <strong>liquid cash</strong> to close the deal safely.</p>

<h2 id="affordability-rules-and-qualifying-measures-dti-income-and-savings">Affordability rules and qualifying measures: DTI, income, and savings</h2>

<p>Lenders do not just look at the house price. They look at your ability to carry the payment without too much risk. The main tool they use is your <strong>debt-to-income ratio</strong>, often called <strong>DTI</strong>.</p>

<h3 id="what-is-debt-to-income-ratio-">What is debt-to-income ratio?</h3>

<p>DTI compares your monthly debt payments to your gross monthly income.</p>

<p>There are two common versions:</p>

<ul>

<li><strong>Front-end ratio</strong>: housing costs only</li>

<li><strong>Back-end ratio</strong>: housing costs plus all other monthly debts</li>

</ul>

<p>A lender may look at both, but the back-end ratio is usually the bigger one.</p>

<p>Common benchmarks include:</p>

<ul>

<li><strong>28% front-end</strong>: housing payment should stay near or below 28% of gross monthly income</li>

<li><strong>36% back-end</strong>: a conservative target</li>

<li><strong>43% to 45% back-end</strong>: often the upper range for many loan programs, depending on the file</li>

</ul>

<h3 id="how-to-estimate-the-income-you-need">How to estimate the income you need</h3>

<p>Let us say your total monthly housing cost is <strong>$3,100</strong>.</p>

<p>If a lender uses a <strong>28% front-end ratio</strong>, then:</p>

<ul>

<li>$3,100 ÷ 0.28 = <strong>$11,071 gross monthly income</strong></li>

<li>That is about <strong>$132,850 gross annual income</strong></li>

</ul>

<p>If the lender uses a more flexible back-end rule and you have other debts, the income target may need to be even higher.</p>

<h3 id="why-other-debts-matter-so-much">Why other debts matter so much</h3>

<p>If you also have:</p>

<ul>

<li>a car loan</li>

<li>student loans</li>

<li>credit card minimum payments</li>

<li>personal loans</li>

</ul>

<p>then your qualifying room shrinks fast.</p>

<p>For example, if your housing payment is manageable but your total monthly debt load is too high, the lender may still say no.</p>

<p>This is why the phrase <strong>debt-to-income ratio</strong> matters so much when you ask <strong>can i afford a 500k house</strong>. You may feel ready, but the lender still has to see enough room in your budget.</p>

<h3 id="savings-and-reserve-requirements">Savings and reserve requirements</h3>

<p>Even if you qualify on paper, lenders may want to see that you have savings left after closing.</p>

<p>That means:</p>

<ul>

<li>an emergency fund</li>

<li>cash reserves for repairs</li>

<li>money for job disruptions</li>

<li>funds for maintenance and appliance replacement</li>

</ul>

<p>A house is not just a payment. It is also a system that can break, leak, and need care. If your savings are thin, a $500k home can become stressful very quickly.</p>

<h2 id="real-examples-income-scenarios-that-can-afford-500k">Real examples: income scenarios that can afford $500K</h2>

<p>Let us make this practical. The table below shows three buyer profiles and how a $500k home might fit into each one.</p>

<table>

<thead>

<tr>

<th>Profile</th>

<th>Gross Annual Income</th>

<th>Down Payment</th>

<th>Monthly Debts</th>

<th>Estimated Housing Payment</th>

<th>DTI Result</th>

<th>Likely Outcome</th>

</tr>

</thead>

<tbody>

<tr>

<td><strong>A: Dual-income young family</strong></td>

<td>$180,000</td>

<td>20% ($100,000)</td>

<td>$900</td>

<td>$3,050</td>

<td>About 26% housing / 32% back-end</td>

<td><strong>Likely affordable</strong></td>

</tr>

<tr>

<td><strong>B: Single buyer with student loans</strong></td>

<td>$110,000</td>

<td>10% ($50,000)</td>

<td>$850</td>

<td>$3,250</td>

<td>About 35% housing / 44% back-end</td>

<td><strong>Tight, but possible</strong></td>

</tr>

<tr>

<td><strong>C: High-earning professional</strong></td>

<td>$220,000</td>

<td>5% ($25,000)</td>

<td>$1,200</td>

<td>$3,450</td>

<td>About 19% housing / 26% back-end</td>

<td><strong>Likely affordable</strong></td>

</tr>

</tbody>

</table>

<h3 id="profile-a-dual-income-young-family">Profile A: Dual-income young family</h3>

<p>This couple earns a strong combined income and puts <strong>20% down</strong>. Their loan is smaller, they avoid PMI, and their total monthly payment stays more controlled.</p>

<p>They likely qualify comfortably if their other debt is moderate and their savings remain healthy after closing.</p>

<p><strong>Best fit:</strong> good option if they want stability and can handle a larger upfront cash commitment.</p>

<h3 id="profile-b-single-buyer-with-moderate-student-loans">Profile B: Single buyer with moderate student loans</h3>

<p>This buyer may be able to qualify, but the payment could stretch the budget. The lower down payment means PMI might apply, and the student loan adds pressure to the DTI ratio.</p>

<p>This buyer may still succeed if they keep other spending low and have enough savings. But this is the kind of case where asking <strong>can i afford a 500k house</strong> is especially important. The answer may be yes on paper, but tight in real life.</p>

<p><strong>Best fit:</strong> possible with careful budgeting, but a larger down payment or lower purchase price would reduce stress.</p>

<h3 id="profile-c-high-earning-professional">Profile C: High-earning professional</h3>

<p>This buyer has strong income and more room in the budget. Even with a lower down payment, the payment may still fit comfortably because the income cushion is larger.</p>

<p>That said, a low down payment can still mean PMI and less flexibility at closing.</p>

<p><strong>Best fit:</strong> financially capable, but should still keep a reserve fund and avoid overbuying just because approval is available.</p>

<h3 id="what-these-examples-show">What these examples show</h3>

<p>A <strong>$500k house</strong> does not automatically require a huge salary, but it does require the right mix of income, debt, and savings. Two buyers can make very different decisions based on the same home because their financial lives are not the same.</p>

<h2 id="ways-to-make-a-500k-house-more-affordable">Ways to make a $500K house more affordable</h2>

<p>If the home feels close but not quite comfortable, there are several ways to improve the numbers.</p>

<h3 id="1-put-more-money-down">Put more money down</h3>

<p>A bigger down payment can:</p>

<ul>

<li>reduce your loan amount</li>

<li>lower your monthly payment</li>

<li>remove PMI</li>

<li>make your offer stronger in competitive markets</li>

</ul>

<h3 id="2-reduce-other-debts-first">Reduce other debts first</h3>

<p>Paying down a car loan, credit cards, or personal loans can improve your DTI and make it easier to qualify.</p>

<h3 id="3-shop-rates-carefully">Shop rates carefully</h3>

<p>Even a small rate difference can save a lot over 30 years. Compare offers and do not assume the first quote is the best one.</p>

<h3 id="4-consider-lender-credits-or-points">Consider lender credits or points</h3>

<p>You may be able to pay points upfront to lower the rate, or accept a slightly higher rate in exchange for lower closing costs.</p>

<h3 id="5-look-at-lower-tax-areas">Look at lower-tax areas</h3>

<p>A nearby neighborhood with lower property taxes or a smaller HOA can make a big difference in monthly cost.</p>

<h3 id="6-explore-assistance-programs">Explore assistance programs</h3>

<p>Depending on where you live, you may find:</p>

<ul>

<li><strong>down payment assistance</strong></li>

<li><strong>FHA loans</strong></li>

<li><strong>VA loans</strong></li>

<li><strong>USDA loans</strong></li>

<li>state or local homebuyer programs</li>

</ul>

<p>These programs can help lower the cash needed to close, which may be the missing piece.</p>

<h3 id="7-consider-a-different-property-type">Consider a different property type</h3>

<p>A condo, townhouse, or smaller single-family home may give you a lower entry price and lower overall monthly cost.</p>

<p>If you want practical <strong>afford 500k house tips</strong>, the biggest one is this: do not only focus on the purchase price. Focus on the total monthly burden and the cash you need on day one.</p>

<h2 id="when-a-500k-house-is-not-affordable">When a $500K house is NOT affordable</h2>

<p>Sometimes the smartest answer is to wait.</p>

<p>A $500k house may not be the right choice if:</p>

<ul>

<li>your <strong>DTI is too high</strong></li>

<li>you have <strong>little or no emergency savings</strong></li>

<li>your payment would leave no room for repairs or lifestyle costs</li>

<li>you would struggle if one income stopped</li>

<li>the house would block your other goals, like retirement savings or paying off debt</li>

</ul>

<p>A home should support your life, not squeeze it.</p>

<p>If you are constantly juggling bills or planning to use every dollar just to close, that is a warning sign. You want a mortgage that fits your life even after the excitement of moving in fades.</p>

<p>If the math feels too tight, alternatives can be smarter:</p>

<ul>

<li>buy in a lower-priced neighborhood</li>

<li>save for a larger down payment</li>

<li>rent a little longer while building cash</li>

<li>choose a smaller home now and upgrade later</li>

</ul>

<p>The goal is not just to buy a house. The goal is to buy a house you can live with comfortably.</p>

<h2 id="checklist-before-you-make-an-offer-on-a-500k-house">Checklist: before you make an offer on a $500K house</h2>

<p>Before you commit, make sure you have the basics covered.</p>

<h3 id="quick-pre-offer-checklist">Quick pre-offer checklist</h3>

<ul>

<li><strong>Get mortgage pre-approval</strong></li>

<li><strong>Confirm your down payment and closing cost savings</strong></li>

<li><strong>Estimate the full monthly payment</strong></li>

<li><strong>Check property taxes and insurance costs</strong></li>

<li><strong>Review HOA rules and dues</strong></li>

<li><strong>Budget for inspection and appraisal</strong></li>

<li><strong>Keep an emergency fund after closing</strong></li>

<li><strong>Understand resale value and neighborhood demand</strong></li>

<li><strong>Compare similar homes nearby</strong></li>

<li><strong>Decide your maximum comfortable payment before house hunting</strong></li>

</ul>

<p>This checklist helps you stay grounded. It also keeps emotion from taking over when you fall in love with a property.</p>

<h2 id="tools-and-resources-to-help-you-decide">Tools and resources to help you decide</h2>

<p>You do not need to guess your way through this.</p>

<p>Useful tools include:</p>

<ul>

<li><strong>Mortgage calculator</strong> for estimating principal and interest</li>

<li><strong>Housing affordability calculator</strong> for checking safe price ranges</li>

<li><strong>Debt-to-income calculator</strong> for lender-style qualification estimates</li>

<li><strong>Refinance calculator</strong> if you want to compare future options</li>

<li><strong>County property tax lookup</strong> tools to estimate taxes by location</li>

</ul>

<p>It is also wise to talk to:</p>

<ul>

<li>a <strong>mortgage broker</strong> for rate and loan program options</li>

<li>a <strong>local real estate agent</strong> for neighborhood-level tax and HOA norms</li>

<li>a <strong>loan officer</strong> for pre-approval details</li>

<li>a <strong>tax professional</strong> if you want help understanding deductibility rules</li>

</ul>

<p>If your goal is to answer <strong>can i afford a 500k house</strong> with more precision, these tools can turn a guess into a real plan.</p>

<h2 id="faq">FAQ</h2>

<h3 id="do-i-need-20-down-for-a-500k-house-">Do I need 20% down for a $500K house?</h3>

<p>No, you do not. Many buyers purchase with less than 20% down. However, a smaller down payment may mean <strong>PMI</strong> and a higher monthly payment. If you can reach 20%, it often improves the overall numbers.</p>

<h3 id="how-much-income-do-i-need-to-afford-a-500k-house-">How much income do I need to afford a $500K house?</h3>

<p>There is no single number, but a rough rule is that your monthly housing payment should fit comfortably within your gross income. If the total housing cost is around <strong>$3,000 to $3,500 per month</strong>, you may need something like <strong>$120,000 to $160,000+ in annual gross income</strong>, depending on debts and the lender’s guidelines.</p>

<h3 id="what-interest-rate-should-i-use-in-my-calculations-">What interest rate should I use in my calculations?</h3>

<p>Use <strong>current market rates</strong> and run a few scenarios. Do not rely on just one quote. For planning, test a lower, middle, and higher rate so you can see how sensitive your payment is.</p>

<h3 id="can-i-afford-it-if-i-am-self-employed-">Can I afford it if I am self-employed?</h3>

<p>Yes, possibly. But lenders often want more documentation, such as tax returns, bank statements, and proof of stable income. They may also look closely at reserves and business cash flow.</p>

<h3 id="is-a-500k-house-a-good-investment-">Is a $500K house a good investment?</h3>

<p>It can be, but there is no guarantee. A home’s value depends on the local market, the condition of the property, neighborhood demand, and broader economic conditions. Buy it because it fits your life and finances, not just because you hope it will appreciate.</p>

<h2 id="conclusion-and-next-steps">Conclusion and next steps</h2>

<p>So, <strong>can i afford a 500k house</strong>? The real answer is <strong>it depends</strong> on more than the sale price. You need to consider the loan amount, your down payment, current mortgage rates, taxes, insurance, HOA dues, debt, and savings.</p>

<p>A smart next step is simple:</p>

<ol>

<li><strong>Estimate the full monthly payment</strong></li>

<li><strong>Check your DTI</strong></li>

<li><strong>Review your cash for closing</strong></li>

<li><strong>Run a few rate scenarios</strong></li>

<li><strong>Talk to a lender for pre-approval</strong></li>

</ol>

<p>If the numbers feel comfortable, you may be ready. If they feel tight, you still have options. You can save longer, reduce debt, or target a lower-priced home.</p>

<p>The best home purchase is not the biggest one you can qualify for. It is the one you can afford without stress, month after month.</p>

<p><a href="https://comeawayhome.co.uk/">House</a></p>

If you are asking can i afford a 500k house, you are already thinking the right way. A house price is only the starting point. The real question is whether the monthly payment, your upfront cash, and your overall budget all fit together without putting pressure on the rest of your life.

This guide breaks everything down in simple terms. You will learn how to estimate the monthly payment, how much cash you need before closing, how taxes and insurance change the real cost, and how lenders decide whether you qualify. If you are a first-time buyer, moving up to a larger home, or planning a purchase in 2026, this article will help you run the numbers with more confidence.

Can I afford a $500K house?

The short answer is: maybe, but it depends on your income, debts, down payment, and the local cost of owning the home.

A $500,000 house can be affordable for one household and too expensive for another. A buyer with a strong income, low debt, and a healthy down payment may feel comfortable. A buyer with student loans, car payments, credit card balances, or little savings may feel squeezed even if the house looks manageable on paper.

So, if you are wondering can i afford a 500k house, the best approach is to look at the full picture:

- Monthly principal and interest

- Property taxes

- Homeowners insurance

- HOA fees

- Private mortgage insurance, if needed

- Upfront cash for the down payment and closing costs

- Your debt-to-income ratio

- Your emergency savings

Read on, and we will walk through each part step by step.

How mortgage pricing works: principal, interest, and time

When you buy a home with a mortgage, you borrow money from a lender and pay it back over time. That payment has two main parts:

- Principal: the amount you borrowed

- Interest: the cost of borrowing that money

At the start of the loan, a larger share of your payment goes toward interest. Over time, more of it goes toward principal. This is called amortization. It is one reason a 30-year mortgage feels very different from a 15-year mortgage.

The basic idea behind a mortgage for a $500K house

If you buy a $500k house, your mortgage amount depends on how much you put down.

For example:

- 20% down on $500,000 = $100,000 down payment

- Loan amount = $400,000

- 10% down = $50,000 down payment

- Loan amount = $450,000

- 3% down = $15,000 down payment

- Loan amount = $485,000

The more you put down, the less you borrow. That usually lowers your monthly payment and can reduce or eliminate PMI.

30-year mortgage vs. 15-year mortgage

A 30-year mortgage usually gives you the lowest monthly payment, which is why it is the most common choice for many buyers. A 15-year mortgage has a much higher monthly payment, but you pay off the home faster and usually pay less interest overall.

Here is the tradeoff in plain language:

- 30-year loan: easier on monthly cash flow, more total interest over time

- 15-year loan: higher monthly payment, less total interest, faster payoff

For many buyers asking can i afford a 500k house, the 30-year option is the more realistic starting point because it creates more breathing room.

Why interest rates matter so much

Even a small rate change can make a big difference. In a high-rate environment, your monthly payment can jump quickly. As of May 2026, many buyers are still seeing mortgage rates that vary based on credit score, loan type, and market conditions. Instead of focusing on one exact number, it is smarter to run a few scenarios.

That is why a 500k house mortgage calculator is so useful. It lets you compare payments at different rates and down payments before you make a big decision.

How to estimate your monthly payment for a $500K house

A home’s sticker price is not your monthly payment. To estimate what you will really pay each month, work through these steps:

- Start with the purchase price

- Subtract your down payment

- Find the loan amount

- Choose an interest rate

- Choose a loan term

- Add taxes, insurance, PMI, and HOA fees

Let us look at the most important part first: the mortgage payment itself.

Estimate principal and interest

The mortgage payment for a $500k house depends heavily on your loan size and rate. Below are rough examples for a 30-year fixed mortgage. These numbers are approximate and meant for planning, not final underwriting.

Example 1: 20% down

- Purchase price: $500,000

- Down payment: $100,000

- Loan amount: $400,000

- Interest rate: 6.0%

- Loan term: 30 years

- Approximate principal and interest: $2,398 per month

Example 2: 10% down

- Purchase price: $500,000

- Down payment: $50,000

- Loan amount: $450,000

- Interest rate: 6.0%

- Loan term: 30 years

- Approximate principal and interest: $2,697 per month

Example 3: 3% down

- Purchase price: $500,000

- Down payment: $15,000

- Loan amount: $485,000

- Interest rate: 6.0%

- Loan term: 30 years

- Approximate principal and interest: $2,907 per month

Use ranges, not just one number

Rates move. Fees move. Insurance and taxes change by location. That is why it helps to think in ranges.

For a 30-year mortgage on a $500k home, a common planning range for principal and interest might look something like this:

- Lower end: around $2,300 to $2,600

- Middle range: around $2,600 to $3,100

- Higher end: above $3,100 if rates are higher or the loan amount is larger

If you want to answer can i afford a 500k house with confidence, you should use a mortgage calculator and test at least three different scenarios:

- a lower rate

- a middle rate

- a higher rate

That way, you do not build your budget around the best-case outcome only.

Do not stop at principal and interest

Many buyers focus on the mortgage payment and forget the rest. That can create a nasty surprise later. A home payment includes much more than the loan itself, and those extra costs can change the answer fast.

Add recurring housing costs: taxes, insurance, HOA, and PMI

When people ask how much is the monthly payment for a 500k house, they often mean the full housing cost, not just the loan.

Let us break down the costs that show up again and again.

Property taxes

Property taxes depend on your state, county, and city. In many places, they fall somewhere between 0.7% and 2.0% of the home value per year.

For a $500,000 home, that could mean:

- 0.7% = $3,500 per year or about $292 per month

- 1.0% = $5,000 per year or about $417 per month

- 2.0% = $10,000 per year or about $833 per month

That is a huge difference. A house that looks affordable in one county may feel much more expensive in another simply because of taxes.

Homeowners insurance

Homeowners insurance protects you against damage, theft, and certain disasters. Costs vary based on location, home age, coverage level, and risk factors like wind or fire exposure.

A rough planning range for a $500,000 home might be:

- $100 to $250 per month in many areas

- More in high-risk or high-cost areas

If the home is older, in a storm-prone region, or has special coverage needs, insurance can run even higher.

HOA fees

If the home is part of a homeowners association, you may owe HOA dues every month or quarter. These fees can be small or surprisingly large.

Common HOA ranges include:

- $50 to $150 per month for a modest community

- $200 to $500+ per month for communities with more amenities

HOA dues matter because they reduce how much room you have in your monthly budget. Two houses with the same price can have very different real costs if one has a high HOA and the other does not.

PMI: private mortgage insurance

If you put down less than 20%, you may need PMI. This protects the lender, not you. It often adds to your monthly payment until you build enough equity.

PMI cost varies, but a simple planning range could be:

- $100 to $350 per month

- Sometimes more for smaller down payments or lower credit scores

The exact cost depends on loan size, credit profile, and down payment amount.

A sample total monthly housing cost

Here is what a full monthly picture might look like on a $500k home.

Example total

- Principal and interest: $2,398

- Property taxes: $417

- Homeowners insurance: $150

- HOA fee: $100

- PMI: $0 if 20% down, or added if down payment is lower

That gives you a total of about $3,065 per month with 20% down and no PMI.

If you had a smaller down payment and PMI, that same home could easily move closer to $3,200 to $3,500+ per month.

This is why the question can i afford a 500k house is never just about the sale price. It is about the full monthly burden.

Upfront costs to buy a $500K house

A home purchase also requires cash before you even move in. Many buyers are surprised by how much they need beyond the down payment.

Down payment

Your down payment is the chunk you pay upfront toward the purchase price.

Common options include:

- 20% down: avoids PMI in many cases and lowers your loan amount

- 10% down: more accessible, but often includes PMI

- 3% to 5% down: possible with certain loan programs, but monthly costs are usually higher

For a $500k house, the down payment amounts look like this:

- 20% = $100,000

- 10% = $50,000

- 5% = $25,000

- 3% = $15,000

If you are trying to decide whether you can afford it, this is your first cash test. Just because you can qualify for a loan does not mean you can comfortably write the down payment check.

Closing costs

Closing costs are the fees you pay to finalize the purchase. They often include lender fees, title fees, appraisal costs, attorney fees in some states, and prepaid items.

A common range is 2% to 5% of the purchase price.

For a $500,000 home, that means roughly:

- 2% = $10,000

- 3% = $15,000

- 5% = $25,000

That is a big number, and it sits on top of your down payment.

Prepaids and reserves

You may also need money for:

- Initial escrow deposits

- Prepaid property taxes

- Prepaid insurance premiums

- Inspection fees

- Appraisal fees

- Moving costs

- Small repairs or immediate improvements

These items may not feel as important as the down payment, but they can be the difference between a smooth closing and a stressful one.

A realistic cash-to-close example

Let us say you buy a $500k house with 10% down.

- Down payment: $50,000

- Closing costs: $15,000

- Prepaids and escrow: $3,000 to $7,000

- Inspection and appraisal: $800 to $1,500

- Moving and immediate fixes: $2,000 to $5,000

Your total cash need could easily land around $70,000 or more.

That is why many buyers discover that the real challenge is not just qualifying for the mortgage. It is having enough liquid cash to close the deal safely.

Affordability rules and qualifying measures: DTI, income, and savings

Lenders do not just look at the house price. They look at your ability to carry the payment without too much risk. The main tool they use is your debt-to-income ratio, often called DTI.

What is debt-to-income ratio?

DTI compares your monthly debt payments to your gross monthly income.

There are two common versions:

- Front-end ratio: housing costs only

- Back-end ratio: housing costs plus all other monthly debts

A lender may look at both, but the back-end ratio is usually the bigger one.

Common benchmarks include:

- 28% front-end: housing payment should stay near or below 28% of gross monthly income

- 36% back-end: a conservative target

- 43% to 45% back-end: often the upper range for many loan programs, depending on the file

How to estimate the income you need

Let us say your total monthly housing cost is $3,100.

If a lender uses a 28% front-end ratio, then:

- $3,100 ÷ 0.28 = $11,071 gross monthly income

- That is about $132,850 gross annual income

If the lender uses a more flexible back-end rule and you have other debts, the income target may need to be even higher.

Why other debts matter so much

If you also have:

- a car loan

- student loans

- credit card minimum payments

- personal loans

then your qualifying room shrinks fast.

For example, if your housing payment is manageable but your total monthly debt load is too high, the lender may still say no.

This is why the phrase debt-to-income ratio matters so much when you ask can i afford a 500k house. You may feel ready, but the lender still has to see enough room in your budget.

Savings and reserve requirements

Even if you qualify on paper, lenders may want to see that you have savings left after closing.

That means:

- an emergency fund

- cash reserves for repairs

- money for job disruptions

- funds for maintenance and appliance replacement

A house is not just a payment. It is also a system that can break, leak, and need care. If your savings are thin, a $500k home can become stressful very quickly.

Real examples: income scenarios that can afford $500K

Let us make this practical. The table below shows three buyer profiles and how a $500k home might fit into each one.

| Profile |

Gross Annual Income |

Down Payment |

Monthly Debts |

Estimated Housing Payment |

DTI Result |

Likely Outcome |

| A: Dual-income young family |

$180,000 |

20% ($100,000) |

$900 |

$3,050 |

About 26% housing / 32% back-end |

Likely affordable |

| B: Single buyer with student loans |

$110,000 |

10% ($50,000) |

$850 |

$3,250 |

About 35% housing / 44% back-end |

Tight, but possible |

| C: High-earning professional |

$220,000 |

5% ($25,000) |

$1,200 |

$3,450 |

About 19% housing / 26% back-end |

Likely affordable |

Profile A: Dual-income young family

This couple earns a strong combined income and puts 20% down. Their loan is smaller, they avoid PMI, and their total monthly payment stays more controlled.

They likely qualify comfortably if their other debt is moderate and their savings remain healthy after closing.

Best fit: good option if they want stability and can handle a larger upfront cash commitment.

Profile B: Single buyer with moderate student loans

This buyer may be able to qualify, but the payment could stretch the budget. The lower down payment means PMI might apply, and the student loan adds pressure to the DTI ratio.

This buyer may still succeed if they keep other spending low and have enough savings. But this is the kind of case where asking can i afford a 500k house is especially important. The answer may be yes on paper, but tight in real life.

Best fit: possible with careful budgeting, but a larger down payment or lower purchase price would reduce stress.

Profile C: High-earning professional

This buyer has strong income and more room in the budget. Even with a lower down payment, the payment may still fit comfortably because the income cushion is larger.

That said, a low down payment can still mean PMI and less flexibility at closing.

Best fit: financially capable, but should still keep a reserve fund and avoid overbuying just because approval is available.

What these examples show

A $500k house does not automatically require a huge salary, but it does require the right mix of income, debt, and savings. Two buyers can make very different decisions based on the same home because their financial lives are not the same.

Ways to make a $500K house more affordable

If the home feels close but not quite comfortable, there are several ways to improve the numbers.

Put more money down

A bigger down payment can:

- reduce your loan amount

- lower your monthly payment

- remove PMI

- make your offer stronger in competitive markets

Reduce other debts first

Paying down a car loan, credit cards, or personal loans can improve your DTI and make it easier to qualify.

Shop rates carefully

Even a small rate difference can save a lot over 30 years. Compare offers and do not assume the first quote is the best one.

Consider lender credits or points

You may be able to pay points upfront to lower the rate, or accept a slightly higher rate in exchange for lower closing costs.

Look at lower-tax areas

A nearby neighborhood with lower property taxes or a smaller HOA can make a big difference in monthly cost.

Explore assistance programs

Depending on where you live, you may find:

- down payment assistance

- FHA loans

- VA loans

- USDA loans

- state or local homebuyer programs

These programs can help lower the cash needed to close, which may be the missing piece.

Consider a different property type

A condo, townhouse, or smaller single-family home may give you a lower entry price and lower overall monthly cost.

If you want practical afford 500k house tips, the biggest one is this: do not only focus on the purchase price. Focus on the total monthly burden and the cash you need on day one.

When a $500K house is NOT affordable

Sometimes the smartest answer is to wait.

A $500k house may not be the right choice if:

- your DTI is too high

- you have little or no emergency savings

- your payment would leave no room for repairs or lifestyle costs

- you would struggle if one income stopped

- the house would block your other goals, like retirement savings or paying off debt

A home should support your life, not squeeze it.

If you are constantly juggling bills or planning to use every dollar just to close, that is a warning sign. You want a mortgage that fits your life even after the excitement of moving in fades.

If the math feels too tight, alternatives can be smarter:

- buy in a lower-priced neighborhood

- save for a larger down payment

- rent a little longer while building cash

- choose a smaller home now and upgrade later

The goal is not just to buy a house. The goal is to buy a house you can live with comfortably.

Checklist: before you make an offer on a $500K house

Before you commit, make sure you have the basics covered.

Quick pre-offer checklist

- Get mortgage pre-approval

- Confirm your down payment and closing cost savings

- Estimate the full monthly payment

- Check property taxes and insurance costs

- Review HOA rules and dues

- Budget for inspection and appraisal

- Keep an emergency fund after closing

- Understand resale value and neighborhood demand

- Compare similar homes nearby

- Decide your maximum comfortable payment before house hunting

This checklist helps you stay grounded. It also keeps emotion from taking over when you fall in love with a property.

You do not need to guess your way through this.

Useful tools include:

- Mortgage calculator for estimating principal and interest

- Housing affordability calculator for checking safe price ranges

- Debt-to-income calculator for lender-style qualification estimates

- Refinance calculator if you want to compare future options

- County property tax lookup tools to estimate taxes by location

It is also wise to talk to:

- a mortgage broker for rate and loan program options

- a local real estate agent for neighborhood-level tax and HOA norms

- a loan officer for pre-approval details

- a tax professional if you want help understanding deductibility rules

If your goal is to answer can i afford a 500k house with more precision, these tools can turn a guess into a real plan.

FAQ

Do I need 20% down for a $500K house?

No, you do not. Many buyers purchase with less than 20% down. However, a smaller down payment may mean PMI and a higher monthly payment. If you can reach 20%, it often improves the overall numbers.

How much income do I need to afford a $500K house?

There is no single number, but a rough rule is that your monthly housing payment should fit comfortably within your gross income. If the total housing cost is around $3,000 to $3,500 per month, you may need something like $120,000 to $160,000+ in annual gross income, depending on debts and the lender’s guidelines.

What interest rate should I use in my calculations?

Use current market rates and run a few scenarios. Do not rely on just one quote. For planning, test a lower, middle, and higher rate so you can see how sensitive your payment is.

Can I afford it if I am self-employed?

Yes, possibly. But lenders often want more documentation, such as tax returns, bank statements, and proof of stable income. They may also look closely at reserves and business cash flow.

Is a $500K house a good investment?

It can be, but there is no guarantee. A home’s value depends on the local market, the condition of the property, neighborhood demand, and broader economic conditions. Buy it because it fits your life and finances, not just because you hope it will appreciate.

Conclusion and next steps

So, can i afford a 500k house? The real answer is it depends on more than the sale price. You need to consider the loan amount, your down payment, current mortgage rates, taxes, insurance, HOA dues, debt, and savings.

A smart next step is simple:

- Estimate the full monthly payment

- Check your DTI

- Review your cash for closing

- Run a few rate scenarios

- Talk to a lender for pre-approval

If the numbers feel comfortable, you may be ready. If they feel tight, you still have options. You can save longer, reduce debt, or target a lower-priced home.

The best home purchase is not the biggest one you can qualify for. It is the one you can afford without stress, month after month.

House