You know that exact moment. You walk to your mailbox, pull out a thick, official-looking envelope from your local county assessor, and let out a heavy sigh. It is that time of year again—tax season for homeowners. As you scan the document, you might see the words “property tax” bolded at the top. But wait, when you filed your federal income returns last spring, your accountant kept talking about your “real estate tax” deductions.

This raises a common and important question for homeowners: Are real estate and property taxes the same thing?

If you are paying your annual bill and wondering whether you are being double-charged or missing out on key deductions, you are certainly not alone. The world of homeowner finance is packed with confusing jargon. People use these two terms interchangeably in everyday conversation, at neighborhood barbecues, and even in real estate offices.

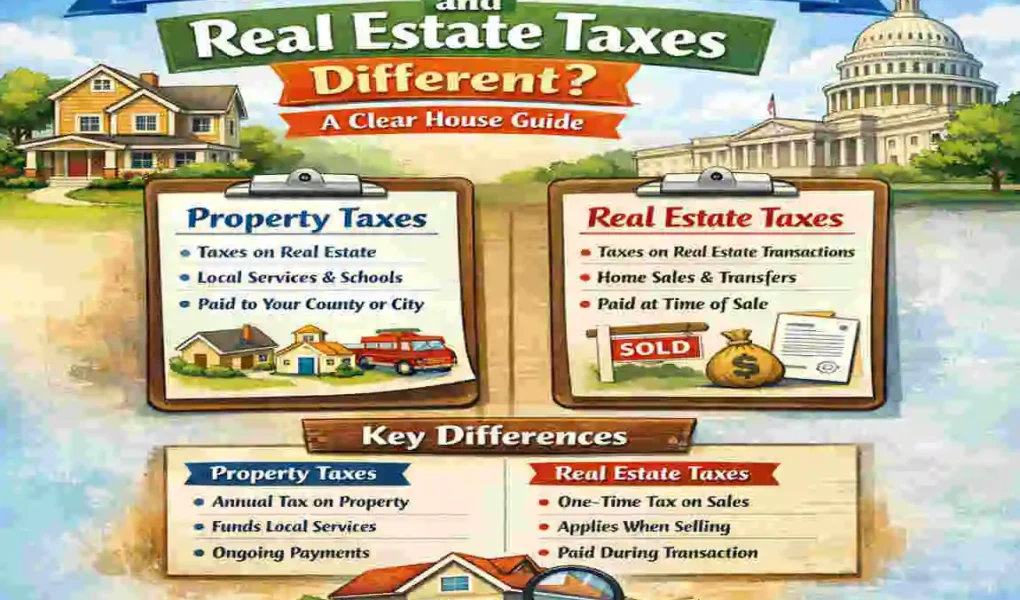

While they are largely synonymous in casual chat, they are not identical in the eyes of the law. The subtle differences between them depend heavily on your local jurisdiction and what exactly is being taxed. Generally speaking, real estate taxes target the physical land and the buildings permanently attached to it. Property taxes, on the other hand, act as a broader umbrella category that can encompass movable, personal assets as well.

| Aspect | Real Estate Tax | Property Tax (Broader) |

|---|---|---|

| What’s Taxed | Land + buildings (immovable property) | Real estate + personal items (cars, boats, equipment in some states) |

| Common Usage | IRS/official term for homes | Everyday term; includes movable assets |

| For Homeowners | Yes—same bill in most cases | Yes, but may add personal property tax |

| Levied By | Local gov’t (counties/cities) | Local/state gov’t |

Core Definitions: Breaking Down the Jargon

To truly understand how your money is being collected and spent, we need to establish clear, simple definitions. Let us put these two terms side by side so you can see exactly how they function in the financial world.

What is Real Estate Tax?

Real estate tax is an annual fee levied by your local government—usually your county, city, or school district. This tax applies only to real property. In the legal world, real property means land and anything permanently affixed to that land.

If you own a plot of dirt, you pay real estate tax on it. If you build a three-bedroom house on that dirt, pour a concrete driveway, and construct an in-ground swimming pool, all of those permanent structures become part of the real estate. Because you cannot pick up your house and move it to another state, it is classified as immovable real estate. Interestingly, when the IRS looks at your federal tax deductions, they prefer the term “real estate tax” to describe the deductible taxes you pay on your home.

What is Property Tax?

Property tax is a much broader category. Think of it as a massive financial umbrella. Yes, the taxes you pay on your physical house and land fall under this umbrella. But property tax can also include taxes on personal property.

Personal property refers to movable assets. Depending on which state you live in, your local government might levy a property tax on your car, your recreational vehicle (RV), your boat, or even heavy equipment you use for a small business.

Here is a simple table to help you visualize the core differences:

Tax Term: What It Actually Covers, Who Levies the Tax

Real Estate Tax Land and permanent, immovable structures (homes, buildings, fences, in-ground pools). Local government (Counties, cities, and public school districts).

Property Tax: The broader category. Includes real estate, PLUS personal movable property (cars, boats, business equipment). Local and sometimes state governments.

The Everyday Conversation Nuance

Here is why the confusion exists: in everyday American conversation, people almost always say “property tax” when referring to the bill for their house. If you ask your neighbor how much they pay in real estate taxes, they might look at you funny. We have socially adopted the broader term to describe the specific tax on our homes.

In most U.S. states, if you own only a home and a standard commuting vehicle, the two terms feel identical. But if you want to be legally and financially accurate, especially when talking to a certified public accountant (CPA), knowing the distinction is powerful.

Key Differences: Are They the Same Thing?

So, we must return to our primary question: are real estate and property taxes the same thing?

The direct, honest answer is: No, not always. Real estate tax is actually a subset of the broader property tax category.

To understand this, we need to dive into the concept of “ad valorem.” This is a Latin phrase that translates to “according to value.” Both real estate taxes and personal property taxes are ad valorem taxes. This means the amount you owe is directly based on the item’s monetary value.

However, the key difference lies in the asset’s mobility.

Immovable vs. Movable Assets

Real estate is immovable. Your local county assessor knows exactly where your house is located. It will be there today, tomorrow, and twenty years from now. Because it is tied to a specific geographical location, the taxes collected on it are used to fund localized services. Your real estate taxes pay for the public schools in your specific zip code, the fire department down the street, the local police force, and the maintenance of the roads you drive on every day.

Personal property is movable. If you own a luxury boat, you could hitch it to your truck and drive it to another state tomorrow. In states that levy taxes on personal property, this is handled differently. For example, you might receive a yearly bill from your county for the assessed value of your vehicles. Business owners often deal with this; a construction company in Texas might have to pay personal property taxes on its tractors, bulldozers, and office computers.

How States Handle the Difference

The United States is a patchwork of different tax laws. What is true in New York might be entirely false in Florida. Let us look at how different states handle the crossover between these two terms.

State Example: Are They the Same Thing Here?Important Context and Notes

Texas, mostly, but with a catch. In Texas, “property tax” is the blanket term. However, they make a clear distinction between real estate and personal property in business settings, where businesses pay taxes on their equipment.

Illinois, yes, effectively. In Illinois, the state does not levy a personal property tax on vehicles or individual movable assets. Therefore, when residents say “property tax,” they exclusively mean real estate tax.

General U.S. Often Interchangeable. It entirely depends on the context of the conversation. For the average homeowner, the terms mean the same thing daily.

Busting a Massive Homeowner Myth

Let us quickly bust a myth that causes a lot of anxiety for first-time buyers. You will not receive two separate, duplicate tax bills for your physical house. The government will not send you a “Real Estate Tax” bill and a separate “Property Tax” bill for the same structure. You will receive one consolidated bill for your home and land. You will only receive a second, separate bill if your state requires you to pay personal property taxes on your vehicles or business assets.

How Your Local Government Calculates These Taxes

Nobody likes opening a massive bill, but the sting is a little less painful when you actually understand how the math works. The process of calculating your real estate taxes can seem like a dark, mysterious art performed by bureaucrats in closed rooms. Still, it is actually a straightforward mathematical formula.

The Basic Tax Formula

At its core, your annual tax bill is determined by multiplying the assessed value of your property by your local tax rate.

Assessed Value × Millage Rate (Tax Rate) = Your Annual Tax Bill

Understanding the Millage Rate

You will often hear the term “millage rate” or “mills” thrown around during tax season. What on earth is a mill?

A “mill” represents one-tenth of one cent. In practical terms, one mill equates to $1 in taxes for every $1,000 of your home’s assessed value.

For example, if your local government sets a tax rate of 10 mills, that translates to a 1% tax rate. If your home is assessed at $1,000,000, a 1% tax rate (10 mills) means your annual tax bill will be $10,000.

The Step-by-Step Calculation Process

Let us break down exactly how your local county moves from reviewing your house to sending you a bill.

The Appraisal: Every few years (the exact frequency depends on your county), a local government official, such as an appraiser or assessor, will determine your property’s market value. They look at recent home sales in your neighborhood, the size of your lot, the square footage of your home, and any major improvements you have made, like adding a new garage. Let us pretend the appraiser decides your home’s fair market value is $300,000.

The Assessment Ratio: Not all counties tax you at 100% of your home’s market value. Many states use an assessment ratio. For instance, a county might have an assessment ratio of 80%. This means they only apply taxes to 80% of your home’s value.

- $300,000 Market Value × 80% Assessment Ratio = $240,000 Assessed Value.

Applying Exemptions Before doing the final math, the county subtracts any legal exemptions you qualify for. The most common is the “Homestead Exemption,” which lowers the taxable value of your primary residence. Let us say your state offers a $40,000 homestead exemption.

- $240,000 Assessed Value – $40,000 Exemption = $200,000 Taxable Value.

Applying the Tax Rate. Finally, the county applies the local tax rate to your taxable value. Let us say your local school board, fire department, and city council have combined their needs and set a total tax rate of 1.5%.

- $200,000 Taxable Value × 1.5% Rate = $3,000 Annual Tax Bill.

And just like that, the mystery is solved. That is exactly how the number on your envelope is generated.

Looking at the Map: Rates and Regional Comparisons

If you have ever talked to a friend who lives in a different state about their tax bill, you might have been shocked by the difference in what you both pay. Real estate taxes vary wildly across the United States.

The National Average Context

Currently, the national average real estate tax rate for a single-family home in the United States hovers around 1.1% of the property’s assessed value.

However, that national average is just a baseline. Because real estate taxes are locally controlled, they serve as the primary funding mechanism for communities without a state income tax. This creates massive regional disparities.

The Highest and Lowest States

If you are looking to relocate, you must pay attention to these regional differences.

States in the Northeast and Midwest typically carry the heaviest tax burdens. New Jersey famously holds the top spot for the nation’s highest real estate taxes, with an average effective rate hovering around a staggering 2.47%. If you own a $500,000 home in New Jersey, you are paying over $12,000 a year just in property taxes! Illinois, New Hampshire, and Connecticut follow closely behind.

On the opposite end of the spectrum, we have states that are incredibly gentle on homeowners. Hawaii has the lowest effective real estate tax rate in the country, at 0.27%. Alabama, Colorado, and Nevada also boast exceptionally low rates.

Why Does This Matter for You?

If you are planning to buy a home, you cannot just look at the property’s sticker price. You must factor in the local tax rate when calculating your monthly affordability. A $400,000 house in New Jersey will cost you thousands of dollars more per year than a $400,000 house in Hawaii.

When you are touring neighborhoods and looking at Zillow listings, always scroll down to the tax history section. Real estate taxes are a permanent, ongoing expense of homeownership. You will pay them long after your 30-year mortgage is fully paid off, so you must ensure the local rates fit your long-term financial goals.

Keep Your Money: Deductions and Savings Tips

Now for the best part of this guide: how to keep more of your hard-earned money in your own bank account. Real estate taxes are a massive expense, but there are entirely legal, smart ways to lower your burden. Real estate taxes, when explained properly, always include a discussion of deductions.

The Federal SALT Deduction

When you file your federal income taxes with the IRS, you are allowed to deduct the local and state taxes you have already paid. This is known as the SALT (State and Local Taxes) deduction.

When you itemize your deductions, you can deduct the real estate taxes you paid on your primary home, as well as any personal property taxes you paid on your vehicles.

However, there is a major catch that was introduced by the Tax Cuts and Jobs Act of 2017. Currently, the federal SALT deduction is capped at $10,000 per year (or $5,000 if you are married but filing separately). If your total state income tax and local property taxes exceed $10,000, you cannot deduct the excess amount on your federal return. It is vital to work with a qualified CPA to ensure you are correctly maximizing this $10,000 limit.

Actionable Ways to Lower Your Tax Bill

You do not have to sit back and accept the bill the county sends you. Here are five proactive ways to lower your costs:

Apply for a Homestead Exemption. We mentioned this earlier. Still, it is worth repeating because millions of homeowners forget to do it! If the house you own is your primary residence (not a vacation home or a rental property), you likely qualify for a homestead exemption. This automatically shields a portion of your home’s value from taxation. You usually have to file paperwork with your county to claim this, so do not assume it is applied automatically.

Look for Special Status Exemptions. Most states offer deep tax breaks for specific groups to help keep housing affordable. If you are a senior citizen (usually over the age of 65), a veteran of the armed forces, or a person with a recognized disability, you could see your tax bill slashed dramatically. Always check your county website for specialized exemption forms.

Protest Your Assessed Value. Remember that local appraiser we talked about? They are human, and they make mistakes. If you open your tax bill and see that the county claims your house is worth $500,000, but identical homes in your neighborhood are only selling for $400,000, you are being overtaxed.

You have the legal right to appeal your assessment. This is highly common in states like Texas. You file an appeal, gather “comps” (comparable recent home sales in your neighborhood), and present your case to an appraisal review board. If you prove your home is worth less than they claim, they will lower your assessed value, instantly dropping your tax bill.

Check Your Property Card for Errors. Your county maintains a “property card” that lists all the details of your home. Sometimes, this data is just wrong. The county might think you have four bedrooms when you only have three, or they might think you have a finished basement when it is just bare concrete. Go online, find your property card on the county assessor’s website, and check it for factual errors. Fixing a simple typo could save you hundreds of dollars.

Avoid Pulling Permits Just Before Assessment Time. If you are planning to build a massive new deck or add a swimming pool, timing matters. If you pull a building permit right before the county does its routine reassessments, your home’s value will spike immediately, increasing your taxes for that year. If you can wait to finalize your upgrades until after the assessment period closes, you might delay the tax increase by a full year.

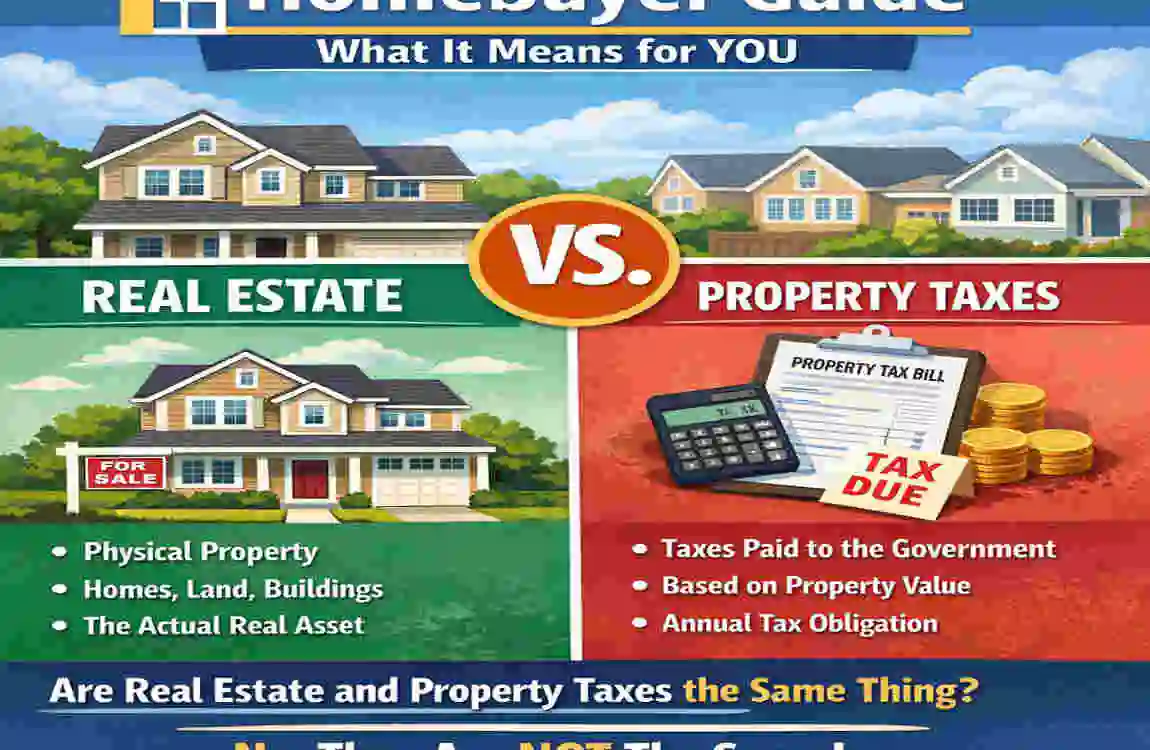

The Homebuyer Guide: What This Means for Your Wallet

If you are currently in the market to buy a home, understanding the nuances of real estate and property taxes is critical. These taxes directly impact your daily cash flow and your long-term wealth building.

Understanding Escrow Accounts

One of the most confusing moments for first-time buyers happens at the closing table when the lender explains the “escrow account.”

Because local governments will literally seize and foreclose on your house if you do not pay your real estate taxes, your mortgage lender is deeply invested in making sure those taxes get paid. To protect themselves, the lender will usually set up an escrow account for you.

Here is how it works: Instead of trusting you to save up $3,600 to pay a massive tax bill at the end of the year, the lender divides that bill by 12. They add $300 to your monthly mortgage payment. Every month, you pay the lender, and they put that $300 into a special, secure escrow savings account. When the county tax bill is due, the lender pays it on your behalf using the money in that account.

This is incredibly convenient because you never have to worry about writing a massive check to the government. However, it also means your monthly mortgage payment will fluctuate. If your local government raises the tax rate, your monthly mortgage payment will go up next year to cover the difference!

The Investment Angle: High Taxes vs. High Yields

If you are buying real estate as an investment, high-tax areas are not always a bad thing.

Why do places like New Jersey or certain suburbs of Chicago have such high real estate taxes? Usually, it is because they have incredibly well-funded, top-tier public school systems, expansive public parks, and excellent community services.

If you are buying a rental property, homes in high-tax areas with great schools attract high-income families willing to pay premium rent to live in that district. High taxes buy community desirability, which in turn protects your property value from declines during economic downturns.

Consult the Professionals for Tax-Smart Buys

Real estate is likely the largest financial transaction of your life. Do not navigate it unthinkingly. It is always wise to consult with a local real estate agent and a qualified tax professional before you buy. They can pull historical tax data, predict future tax hikes based on local city council agendas, and guide you toward tax-smart purchases. If you are looking for expert advice on building wealth through property, our business blog features a wealth of resources and consultations tailored just for you!

Common Myths and Tax FAQs Answered

We have covered a massive amount of ground, but you likely still have a few lingering questions. Let us tackle the most common myths and frequently asked questions head-on.

Q: So, are real estate and property taxes the same thing?A: In casual conversation regarding your house, yes. Legally, no. Real estate tax applies strictly to immovable land and buildings. Property tax is a broader term that includes real estate but can also include movable personal assets like cars, boats, and business machinery.

Q: Do I have to pay for both on my house?A: No! You will not be double-taxed on your physical home. You will receive one bill from your local county covering the land and the structure.

Q: Are my real estate taxes fully tax-deductible? A: Yes, but with a cap. If you itemize your deductions on your federal tax return, you can deduct your local real estate taxes. However, under current federal law, the total amount of State and Local Taxes (SALT) you can deduct is capped at $10,000 per year.

Q: How often do my real estate taxes change? A: Your tax bill can change every single year. It fluctuates based on two factors: changes in your home’s assessed market value, and changes in the millage rate voted on by your local city councils, school boards, and county commissioners.

Q: What exactly is a personal property tax? A: If your state leverages this, it is a tax on movable assets. The most common example is the annual “car tax” (also called the vehicle registration tax), based on the value of your automobile. States like Virginia and Missouri are famous for this.

Q: Do renters have to pay real estate taxes?A: Directly? No. Renters do not receive a tax bill from the county. However, indirectly, absolutely yes. Landlords factor real estate taxes into the monthly rent they charge. When taxes go up in a city, rents usually rise shortly thereafter to cover landlords’ increased expenses.

Q: How do I find out the exact tax rate for a home I want to buy? A: Property tax records are public information in the United States! You can easily go to the local county tax assessor’s website, type in the exact address of the home, and see the exact tax bills that were paid on that property over the last ten years.