Buying a home can feel exciting one minute and overwhelming the next. You find the house, make an offer, negotiate terms, and then hear a word that suddenly seems to carry a lot of weight: closing.

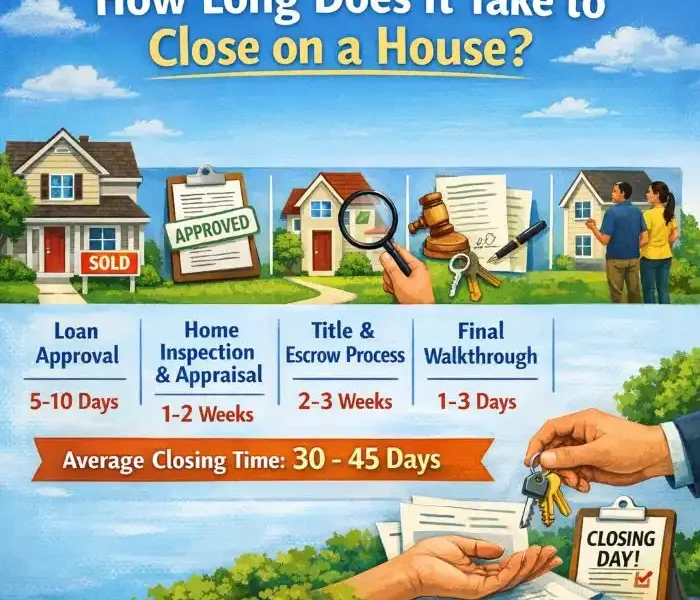

If you are wondering how long does it take to close on a house, the short answer is that it usually takes about 30 to 60 days after your offer is accepted. But that is only the average. Some deals move much faster, while others take longer because of financing issues, appraisal problems, title questions, repairs, or simple paperwork delays.

That is why it helps to understand what closing really involves. It is not just one appointment where you sign a few papers and get the keys. It is a full process with moving parts, deadlines, and multiple people involved. Your lender, agent, title company, seller, inspector, and sometimes even your employer all play a role.

The good news is that once you understand the home closing timeline, the process feels much less confusing. You can prepare early, avoid common mistakes, and respond faster when something comes up.

In this guide, you will learn what closing means, how long each stage usually takes, what can slow things down, and what you can do to keep things moving. If you are a first-time buyer, this article will help you know what to expect from the moment your offer is accepted to the day you officially become a homeowner.

What “Closing on a House” Means

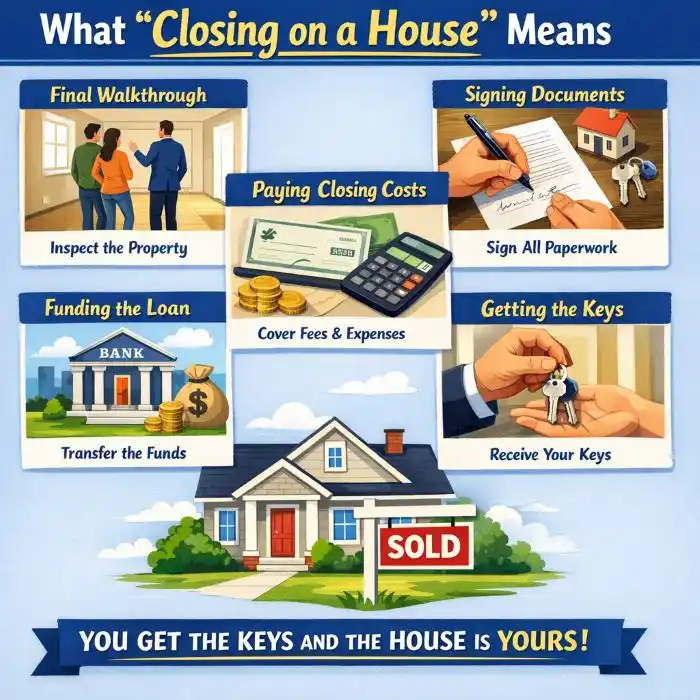

Closing on a house is the final legal step in the home buying process. It is the point where the sale becomes official and ownership of the property transfers from the seller to the buyer.

Think of closing as the finish line. Before you get there, a lot has to happen behind the scenes. Your lender has to approve the mortgage. The property has to be appraised. A title search has to confirm there are no ownership issues. You also need to review and sign a large stack of legal and financial documents.

This is why closing is very different from making an offer or getting preapproved for a mortgage.

When you make an offer, you are simply telling the seller what you are willing to pay and under what terms. When you get preapproved, a lender gives you an estimate of how much you may be able to borrow. Neither of those steps means the deal is final.

Closing is when everything becomes real.

At closing, you usually do all of the following:

- Finalize your mortgage

- Review your closing disclosure

- Pay your closing costs and remaining down payment

- Sign ownership and loan documents

- Complete the transfer of title

- Receive the keys, either that day or shortly after

So if you have ever felt confused about why the process takes so long after an offer is accepted, this is the reason. A home purchase is not just a handshake deal. It is a legal, financial, and administrative process that needs to be done carefully.

How Long Does It Take to Close on a House on Average?

In most cases, closing on a house takes 30 to 60 days from the time the seller accepts your offer.

That range is broad because not all purchases work the same way. A cash purchase may close in a week or two if the title is clear and both sides are ready. A financed purchase usually takes longer because the lender must verify your income, credit, debts, assets, and the property value before issuing final approval.

The loan type can also affect the timeline. A conventional loan often moves in a standard time frame if your documents are complete and your file is straightforward. FHA and VA loans can sometimes take longer because they may involve extra requirements for the borrower, the property, or both.

The answer also depends on practical details like these:

- How quickly your lender works

- How fast you return requested documents

- Whether the appraisal comes in at value

- Whether the inspection finds serious issues

- Whether the title search is clean

- How prepared the seller is

If everything goes smoothly, you may close closer to the 30-day mark. If there are complications, the process can stretch beyond 60 days.

So when people ask, “How long does it take to close on a house?” the most honest answer is this: it depends on the financing, the property, and how quickly everyone involved handles their part of the process.

Home Closing Timeline Week by Week

Understanding the timeline week by week can make the whole process feel much more manageable. Let’s break it down into simple stages so you know what usually happens and when.

Week 1 to 2: Offer Accepted and Contract Signed

Once the seller accepts your offer, the home officially goes under contract. This is a major milestone, but it is really just the beginning of the closing process.

At this stage, you will usually submit your earnest money deposit. This is money that shows you are serious about buying the home. It is not an extra fee. It usually goes toward your purchase costs later.

You will also complete your full mortgage application if you have not done so already. Your lender may ask for documents like recent pay stubs, tax returns, bank statements, ID, and permission to verify employment.

This is also the time when the home inspection and appraisal are often scheduled. The inspection looks at the home’s condition. The appraisal tells the lender whether the home is worth the price you agreed to pay.

These first two weeks matter a lot. Delays here can push everything else back.

If you want a smoother process, treat this stage with urgency. Return documents quickly. Schedule appointments as soon as possible. Read every email from your lender and agent carefully.

Week 2 to 3: Underwriting and Property Review

Once your lender has your application and documents, your file usually moves into underwriting.

Underwriting is the stage where the lender takes a close look at your entire financial picture. They review your income, debts, credit history, assets, employment, and ability to repay the loan. They also review the property itself.

This stage often feels slow to buyers because you may not see much happening. But a lot is going on in the background.

During this time:

- The appraisal is completed and reviewed

- The title company starts the title search

- The lender checks for document consistency

- The underwriter may ask for clarification or extra records

For example, they may ask about a large deposit in your bank account, request updated pay stubs, or want proof that you paid off a debt. These requests are common, so try not to panic if they happen.

The key here is speed and accuracy. If you send the wrong document or wait too long to respond, the file can stall.

Week 3 to 4: Clearing Conditions

After the initial underwriting review, the lender may issue a list of conditions. These are items that must be completed before final approval can happen.

Some conditions are minor. Others can take more time.

Examples include:

- Updated bank statements

- Letters explaining certain transactions

- Proof that homeowner’s insurance has been arranged

- Confirmation that required repairs were completed

- Additional title documents

- Clarification about employment or income

This is also the stage where problems sometimes surface. If the appraisal comes in low, the buyer and seller may need to renegotiate. If the title search finds a lien or ownership issue, the seller may need to resolve it before closing can move forward.

At the same time, the lender works toward issuing the clear to close, which means your loan is approved and ready for final closing steps.

You may also start preparing for the final walkthrough and reviewing the numbers on your loan estimate and upcoming closing disclosure.

Final Week: Closing Day Preparation

The final week is when everything starts to feel very real.

You should receive your closing disclosure, which outlines your final loan terms, monthly payment, closing costs, prepaid items, and total amount due at closing. Review it carefully. Make sure the numbers match what you were expecting.

This is also when you arrange your funds for closing. Depending on the amount and the local process, you may need to wire money or bring a certified check.

You will usually do a final walkthrough shortly before closing. This is your chance to make sure the property is in the agreed condition, any negotiated repairs were completed, and the home is ready for transfer.

Then the signing appointment is scheduled. At that meeting, you sign the mortgage documents, title forms, disclosures, and settlement paperwork.

Once the money is disbursed and the transaction is recorded, the sale is complete.

And yes, this is the moment when buyers finally breathe again.

What Can Delay Closing on a House?

Even a strong deal can hit a few bumps. In fact, some delay is normal in real estate. The important thing is knowing what causes problems so you can reduce the risk.

Here are the most common reasons house closing delays happen:

Missing Financial Documents

Lenders need complete and current records. If you forget to send a bank statement, submit an outdated pay stub, or send unreadable files, underwriting can pause your loan file until the issue is fixed.

Low Appraisal

If the appraised value comes in lower than the purchase price, the lender may not approve the full loan amount. That can lead to renegotiation, a larger down payment, or a dispute that slows the process.

Title Problems or Liens

The title company checks whether the seller truly owns the property and whether there are unpaid taxes, legal claims, or liens attached to it. If something turns up, it usually must be resolved before closing.

Inspection Issues

If the home inspection finds major defects, the buyer and seller may need to renegotiate repairs, credits, or price. That extra negotiation takes time.

Underwriting Delays

Underwriting can move slowly if the file is complex, the lender is overloaded, or the underwriter keeps asking for more information.

Lender Backlog or Holidays

Sometimes the delay is not about your file at all. It may simply be a busy season, limited staffing, or a holiday week that slows reviews, appraisals, wire transfers, or document preparation.

Changes in the Buyer’s Finances

This is a big one. If you switch jobs, open a new credit card, finance a car, miss a bill payment, or make large unexplained deposits during the closing period, the lender may need to reevaluate your file.

Seller-Related Delays

The seller may need more time to move out, complete repairs, find their next home, or clear title issues. Sometimes the buyer is fully ready, but the seller is not.

Here is a simple way to think about it: closing delays usually happen when money, paperwork, property condition, or timing gets complicated.

How Different Loan Types Affect Closing Time

The type of financing you use can shape your mortgage closing time more than many buyers realize. Some loans are more straightforward. Others come with extra rules and checks.

Below is a quick comparison.

| Loan Type | Typical Closing Speed | Why It May Be Faster or Slower | Best Fit For |

|---|---|---|---|

| Conventional Loan | 30–45 days | Often moves smoothly if credit, income, and paperwork are strong | Buyers with solid credit and stable finances |

| FHA Loan | 30–50 days | May take longer due to stricter property and borrower guidelines | Buyers needing lower down payments or more flexible credit rules |

| VA Loan | 30–50+ days | Can involve eligibility checks and property condition requirements | Eligible veterans, active service members, and some military families |

| Cash Purchase | 7–21 days | No mortgage underwriting, but title work and paperwork still matter | Buyers with available funds who want a faster close |

Now let’s look at each type a little more closely.

Conventional Loans

Conventional loans often follow a fairly standard closing timeline. If your credit profile is strong, your income is easy to verify, and the property appraises without issue, this type of loan can move efficiently.

That said, “conventional” does not always mean “fast.” You can still face delays if your lender is slow, your documents are incomplete, or the appraisal or title search uncovers a problem.

For many buyers, though, a conventional loan offers a good balance between flexibility and speed.

FHA Loans

FHA loans are popular with buyers who want a lower down payment or have less-than-perfect credit. They can be a great option, especially for first-time homebuyers.

But FHA loans sometimes take a little longer because the property has to meet certain safety and condition standards. If the appraiser flags issues, the seller may need to fix them before closing can happen.

That does not make FHA loans bad. It just means the process may involve a few extra steps.

VA Loans

VA loans can be an excellent benefit for eligible military borrowers. They often offer strong terms and can reduce upfront costs.

However, the closing timeline can vary depending on lender experience, borrower eligibility documents, and the home’s condition. The appraisal process may also involve standards that affect timing.

In many cases, VA loans close on a normal schedule. But if paperwork or property issues come up, the timeline can stretch.

Cash Purchases

Cash deals usually close the fastest because there is no mortgage underwriting. That removes one of the biggest sources of delay.

Still, “cash” does not mean “instant.”

The buyer still needs title work, a purchase contract, and closing documents. Many cash buyers also order inspections, and that can add time if repairs become part of the negotiation.

Even so, if the title is clean and both parties are ready, a cash purchase can close much faster than a financed one.

What Happens During the Closing Process?

The closing process includes several final steps that bring the transaction together. Here is what usually happens near the end.

First, you receive and review the closing disclosure. This document explains your final loan details and costs. Compare it carefully with your loan estimate so there are no surprises.

Next comes the final walkthrough. This is not a second home inspection. It is simply your chance to confirm that the home is in the agreed condition, repairs are done if required, and no major new issues appeared.

Then you attend the signing appointment. This is where you sign the mortgage note, deed of trust or mortgage paperwork, tax forms, title documents, and settlement documents.

You also pay your closing costs and any remaining down payment funds due.

After signing, the lender releases the loan funds. The title or closing company disburses money to the seller and any other parties who need to be paid, such as lien holders or service providers.

Finally, ownership transfers to you.

Some buyers get the keys the same day. In other cases, the keys are handed over once the sale is officially recorded. Your agent or closing company will tell you what to expect in your area.

How to Close on a House Faster

You cannot control every part of the process, but you can absolutely speed up your side of it.

Here are practical ways to help your deal move faster:

- Get preapproved before you start house hunting

- Choose a lender with a reputation for clear communication

- Keep your pay stubs, tax returns, W-2s, and bank statements ready

- Reply to lender requests the same day when possible

- Schedule the inspection quickly

- Avoid changing jobs or making large purchases

- Do not open new credit accounts before closing

- Review every document as soon as it arrives

- Stay in close contact with your agent and lender

- Ask questions early instead of waiting until the last minute

The biggest time saver is simple: be organized.

A lot of closing delays happen because buyers underestimate how document-heavy the process is. If you already have your records ready and you respond quickly, you remove one of the most common causes of slowdown.

Also, be careful with your finances while the loan is in progress. Even if you are approved, the lender may check your credit and employment again before closing. This is not the time to buy furniture on credit, finance a car, or move large amounts of money without a clear paper trail.

Closing Costs and Paperwork to Expect

Closing is not just about timing. It is also about being ready for the money and paperwork involved.

Common Closing Costs

Closing costs usually include a mix of lender fees, third-party service charges, and prepaid housing expenses. Depending on the loan and location, these may include:

- Loan origination fees

- Appraisal fee

- Credit report fee

- Title search and title insurance fees

- Attorney or settlement fee

- Recording fees

- Prepaid property taxes

- Prepaid homeowner’s insurance

- Prepaid mortgage interest

- Escrow funding

These costs can add up, so it helps to review estimates early in the process rather than waiting until the last week.

Common Closing Paperwork

The paperwork can look intimidating, but much of it is standard.

You may sign documents such as:

- Closing disclosure

- Promissory note

- Mortgage or deed of trust

- Settlement statement

- Title transfer documents

- Tax and escrow forms

- Occupancy and identity verification forms

Take your time when reviewing them. If something looks different from what you expected, ask before signing.

A lot of last-minute stress comes from buyers seeing these numbers for the first time at closing. You can reduce that stress by reading every document carefully as it comes in during the process.

Signs Your Closing Is on Track

Not sure whether things are moving normally? That is common. The closing process often feels quiet, and buyers sometimes worry even when everything is fine.

Here are some signs that your closing is on track:

Underwriting Is Moving Without Constant Problems

A few document requests are normal. But if your lender is asking for reasonable items and the file is progressing, that is a good sign.

The Appraisal and Inspection Were Completed on Time

These are two major milestones. If both happen early and no big issues are found, your timeline is usually in decent shape.

The Title Search Looks Clean

If no ownership disputes, liens, or legal claims are found, the path to closing becomes much smoother.

You Received the Closing Disclosure

Getting the closing disclosure usually means the loan is in its final stages and the numbers are being prepared for closing.

Final Funds Have Been Confirmed

If you know how much you need to bring and how to send it, that means the process is nearing the finish line.

The Closing Date Is Set and Everyone Is Communicating

A scheduled signing appointment with no major red flags is one of the clearest signs that things are on track.

If you are seeing most of these signs, you are probably in good shape.

When to Worry About Closing Delays

Some delays are small and normal. Others deserve immediate attention.

For example, it is not unusual for a lender to ask for one more bank statement or for a closing date to shift by a few days because documents are still being prepared. That can be frustrating, but it is usually manageable.

More serious delays tend to involve bigger unresolved issues, such as:

- Repeated underwriting concerns with no clear resolution

- A low appraisal with no agreement between buyer and seller

- A title problem that remains unresolved

- Missing repair work required by the lender

- An unexplained change in your credit, income, or employment

- The seller not being ready to close

So when should you worry?

You should pay close attention if deadlines keep slipping, nobody is giving you a clear explanation, or a problem has been sitting unresolved for several days without a plan.

If that happens, contact your lender and your real estate agent right away. Ask direct questions:

- What exactly is causing the delay?

- Who is responsible for the next step?

- What is the deadline to fix it?

- Is the closing date still realistic?

- Do we need to amend the contract timeline?

The goal is not to panic. The goal is to get clarity.

Most closing problems can still be solved, especially when they are addressed early.

FAQs About Closing on a House

Can you close on a house in 2 weeks?

Yes, but it is not common for a financed purchase. A two-week closing usually happens in a simple cash deal or in a very well-prepared transaction where the title is clean, inspections are either waived or completed quickly, and all documents are ready upfront.

If you are using a mortgage, two weeks is possible in rare cases, but it is aggressive. Most buyers should expect a longer timeline.

What is the fastest way to close on a house?

The fastest way to close is to be fully prepared before your offer is accepted. That means getting preapproved, choosing an efficient lender, having your financial documents ready, responding quickly to every request, and making sure the title and property condition do not create surprises.

Cash purchases are usually the fastest because they skip mortgage underwriting, but even then, title work and paperwork still take time.

Why does underwriting take so long?

Underwriting takes time because the lender is checking both you and the property. They verify your income, employment, debts, credit history, assets, and the home’s value. They are making sure the loan meets guidelines and that the risk makes sense.

Even a small inconsistency can trigger follow-up questions. That is why it can feel slow, especially if extra documents are needed.

Can a closing date be changed?

Yes. A closing date can absolutely be changed if the buyer, seller, lender, or title company needs more time. This happens more often than many people think.

The key is communication. If a delay becomes likely, it is best to address it early so contract deadlines can be updated properly and expectations stay realistic.

Does inspection delay closing?

It can. If the inspection finds only minor issues, it may not affect the timeline much at all. But if it finds major repairs, safety concerns, or hidden damage, the buyer and seller may need time to negotiate next steps.

That negotiation can delay closing, especially if repairs need to be completed before the lender will approve the loan.

Conclusion

So, how long does it take to close on a house? In most cases, you can expect the process to take around 30 to 60 days, though cash deals may close faster and more complex transactions may take longer.

The most important thing to remember is that some variation is completely normal. A closing timeline depends on financing, paperwork, the property itself, and how quickly everyone involved handles their part.

If you want the process to go smoothly, prepare early, stay organized, and respond fast. The more ready you are before the closing process begins, the easier it becomes to avoid delays and move into your new home with confidence.