Picture this familiar scenario: It is late on a Tuesday night, and you are endlessly scrolling through real estate listings on Zillow. You spot the perfect suburban home with a beautiful backyard, a cozy living room, and a pristine kitchen. You can instantly imagine your family living there. But just as quickly as the excitement builds, a wave of anxiety washes over you. You suddenly freeze at the sight of confusing mortgage jargon, towering interest rates, and intimidating property taxes.

Does this sound familiar? If so, you are definitely not alone.

Many first-time buyers look at the current real estate market and feel entirely defeated. Between the seemingly high interest rates, a massive 7% average down payment requirement, and fierce competition from cash-rich corporate investors, getting your foot in the door can feel impossible. The process of figuring out how to buy a house in the USA often feels like navigating a massive maze while blindfolded.

However, the modern American dream of homeownership is still very much alive and entirely achievable. In fact, recent data shows that a staggering 68% of millennials plan to buy a home by 2026. With the right preparation, a solid strategy, and a structured approach, you can successfully navigate this market and claim your very own piece of real estate.

| Step | Action | Key Tips |

|---|---|---|

| Assess Finances | Check credit (620+ ideal), income, debts | Aim for 3-20% down payment plus 2-5% closing costs. |

| Set Budget | Use 28/36 rule (housing ≤28% income) | Include taxes, insurance, maintenance (1-2% yearly). |

| Get Preapproved | Shop lenders for mortgage letter | Gather pay stubs, tax returns; valid 60-90 days. |

| Hire Realtor | Find agent via referrals/reviews | Seller pays 2.5-3% commission. |

| House Hunt | List must-haves (location, size) | Tour 3-5 homes; check schools, Walk Score. |

| Make Offer | Submit price + contingencies | Add 1-3% earnest money; negotiate counters. |

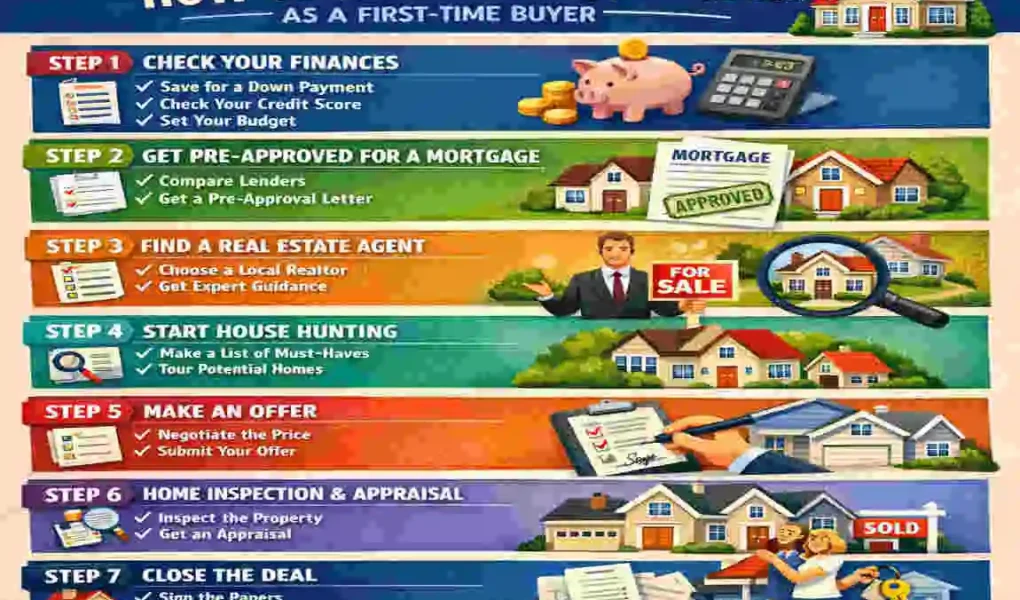

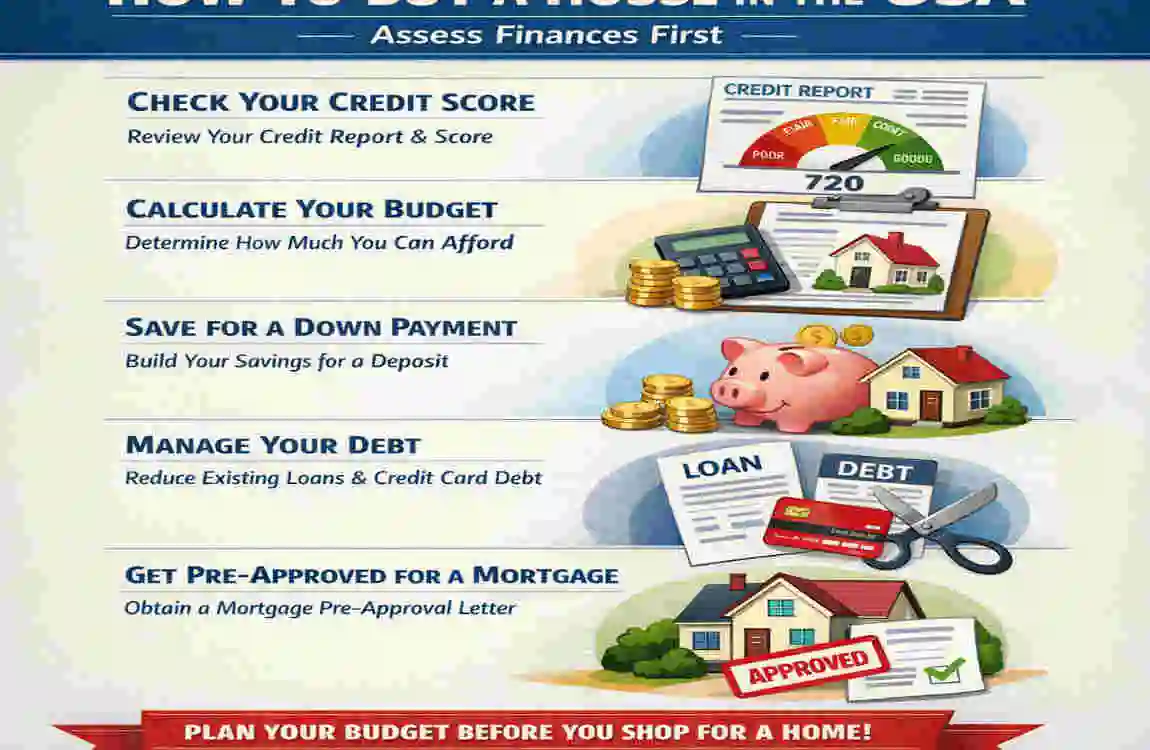

Assess Finances First

Before you even think about attending an open house or falling in love with a property, you need to take a hard, honest look at your financial health. The modern American dream starts with meticulous preparation.

Why Budget Before Browsing

Browsing homes before knowing what you can afford is a recipe for heartbreak. The very first metric you must understand is your debt-to-income ratio (DTI). Your DTI is simply a comparison of how much money you owe each month (like car loans, student loans, and credit cards) to your gross monthly income. Mortgage lenders generally want to see a DTI under 43%.

To keep your daily life comfortable, financial experts highly recommend following the 28/36 rule. This classic guideline states that your maximum household housing expenses should not exceed 28% of your gross monthly income. In comparison, your total overall debt should stay below 36%.

Let us look at the current numbers. With the median home price at $412,000, a typical buyer needs an annual income of roughly $119,000 to afford the monthly payments comfortably. If your savings account needs a boost to reach your goals, start applying the 50/30/20 rule today. Dedicate 50% of your income to absolute needs, 30% to your personal wants, and strictly funnel the remaining 20% directly into your down payment savings fund.

Check Your Credit Score

Your credit score is the ultimate magic number in the real estate world. It dictates whether a lender will approve your loan and, more importantly, what interest rate they will charge you.

Ideally, you should aim for a credit score of 620 or higher to secure the most favorable mortgage rates. However, do not panic if your score is lower. If you are willing to purchase a fixer-upper, the average approved credit score for certain government-backed loans is around 580.

Start by pulling your completely free credit reports via AnnualCreditReport.com. Comb through these documents carefully and immediately dispute any errors you find. Why is this so important? A simple 100-point score boost can save you $40,000 in interest over the life of your loan.

Calculate Affordability

When calculating exactly how much house you can afford, you must look beyond the sticker price and understand your PITI: Principal, Interest, Taxes, and Insurance.

Your monthly mortgage payment includes all four of these elements. For many first-time buyers, capping your PITI at $2,500 per month is a very safe, manageable goal.

Use reliable online mortgage calculators to run these numbers. Furthermore, you absolutely must include an extra 2% to 5% of the total loan amount in your budget to cover mandatory closing costs.

Secure Mortgage Pre-Approval

Once your finances are organized, your next major step in learning how to buy a house in the USA is securing a mortgage pre-approval. This crucial step turns you from a casual window-shopper into a serious, qualified buyer.

Types of Loans for Beginners

The mortgage world offers a variety of loan products tailored to different financial situations. As a beginner, here are the primary options you will encounter:

Loan Type Minimum Down Payment Best Suited For

FHA Loan 3.5% Buyers with lower credit scores or smaller savings.

VA Loan 0% Active-duty military members and honored veterans.

USDA Loan 0% Buyers purchasing homes in designated rural areas.

Conventional 3% to 5% Buyers with excellent credit and manageable debt.

For the vast majority of new buyers, the Federal Housing Administration (FHA) loan is the holy grail. In fact, an FHA loan is the ideal choice for 96% of first-time homebuyers with less than $100,000 saved for a down payment. Whichever route you choose, make sure to shop around and compare rates from at least three different lenders to secure the lowest possible interest rate.

Documents Needed

Lenders love paperwork, and they will want to verify every single detail of your financial life. To speed up your pre-approval process, gather the following documents into a dedicated folder:

- Your most recent pay stubs covering the last two months.

- Your W-2 forms from the past two years.

- Your complete federal tax returns from the past two years.

- Your bank statements from the last 60 days.

The lender will also ask for undeniable proof of your assets. They want to ensure you have enough cash reserves in the bank to cover emergency expenses after you close on the house.

Benefits of Pre-Approval

Do not confuse pre-qualification with pre-approval. A pre-approval is a firm, written commitment from a lender stating exactly how much money they are willing to let you borrow.

Getting this document before you start house hunting is vital. First, it shows sellers that you are a serious, financially secure buyer. Second, a pre-approval letter generally locks in your quoted interest rate for 60 to 90 days. This protects you from sudden, unexpected rate hikes while you search for your dream home.

Assemble Your Team

Buying a home is not a solo mission. You need a dedicated team of seasoned professionals to guide you through the complex legal and structural hurdles of the real estate market.

Hire a Buyer’s Agent

Your most valuable teammate will be your real estate agent. If you are worried about the cost, you can breathe a sigh of relief: hiring a buyer’s agent is almost always completely free for you! The seller typically pays a 2.5% to 3% commission to both agents involved in the transaction.

Take the time to interview at least three different agents. Seek out personal referrals from friends or family members who recently bought homes. Be on the lookout for major red flags during these interviews. If an agent is overly pushy or constantly tries to steer you toward homes that max out your budget, walk away and find someone who respects your financial boundaries.

Other Pros: Inspector, Appraiser, Attorney

Once you find a home, you will rely on several other experts to protect your investment. You will absolutely need to hire a licensed home inspector. While an inspection costs an average of $400, it is the best money you will ever spend. Inspectors catch hidden disasters, ultimately saving buyers an average of $15,000 in unforeseen repair costs.

Depending on where you live, you might also need legal representation. In about 10 US states, the law requires you to hire a real estate attorney to review all closing contracts formally.

Lenders and Title Companies

Your lender will handle the heavy lifting of your financing. At the same time, a title company will ensure the legal transfer of the property. Make sure your title company locks in a robust title insurance policy. This specific insurance protects you against any hidden liens or past ownership disputes that could threaten your legal claim to the home.

House Hunting Strategies

Now comes the fun part! With your pre-approval in hand and your team assembled, you can finally hit the streets and start viewing homes.

Define Your Must-Haves

Before you schedule a single tour, sit down and define your absolute must-haves. Create a strict list of 10 to 15 non-negotiable items.

Do you require at least three bedrooms and two full bathrooms? Is a daily commute of under 30 minutes critical for your sanity? Are you highly focused on education, requiring a local school district with a GreatSchools score of 7 or higher?

Write these criteria down and stick to them. Also, unless you are a highly skilled contractor with a massive cash reserve, it is incredibly wise to avoid major fixer-uppers for your first purchase.

Use Listings Wisely

Leverage the power of modern technology by using digital listing platforms like Zillow and Realtor.com. Set up customized, automated email alerts based on your target criteria, so you instantly know when a new property hits the market or when a seller lowers their price.

Plan to tour 5 to 10 homes in person. During these walkthroughs, look past the beautiful staging furniture. Note the overall condition of the property. Does the neighborhood suffer from excessive highway noise? Does the property sit in a valley that might present a severe flood risk?

Market Timing

Understanding how to buy a house in the USAthe USA means understanding the market’s rhythm. Spring is the absolute peak season for real estate, bringing fierce competition and bidding wars. If you want to find a great deal, try hunting during the off-season in late fall or winter.

There is also excellent news on the horizon for patient buyers: nationwide housing inventory is projected to increase by 20% in 2026. This extra supply will cool down the competition and give you far more options. To save time, utilize 3D virtual tours to aggressively filter out properties before you spend your weekends driving across town.

Neighborhood Deep Dive

Never buy a great house in a bad neighborhood. Use resources like CrimeGrade.org to check the local crime statistics. Furthermore, research the town’s municipal plans to see if any future commercial developments, such as a massive new shopping mall or a noisy highway expansion, are slated for your future backyard.

Make and Negotiate Offers

You found “the one.” Your heart is racing, and you are ready to claim it. Now is the time to draft a strategic, winning offer.

Craft the Offer

Work very closely with your real estate agent to determine a fair, competitive price. If the house has been sitting on the market for weeks, you can confidently offer 1% to 5% below the asking price.

However, if you are in a highly competitive bidding war, you should include an escalation clause. This clever legal addendum automatically increases your offer by a set amount if another buyer tries to outbid you.

To show the seller you mean business, you will submit an earnest money deposit alongside your offer. This good-faith deposit generally ranges from 1% to 3% of the total purchase price. It is held in a secure escrow account until closing day.

Contingencies Explained

Never submit an offer without protecting yourself. Contingencies are legal escape hatches built directly into your contract.

You must include a financing contingency, which allows you to back out with your earnest money intact if your mortgage loan falls through. You also need a strict inspection contingency. Finally, an appraisal contingency provides crucial gap coverage; if the bank values the home for less than your offered price, this clause allows you to renegotiate or walk away without penalty.

Negotiation Tactics

Expect the seller to push back. It is incredibly common to counteroffer two or three times before reaching a final agreement.

Do not be afraid to ask for specific concessions. You can request that the seller pay for necessary roof repairs, or you can ask for financial credits to cover a portion of your closing costs. Interestingly, statistics show that 60% of offers are accepted even with a strict inspection contingency included. Sellers expect you to protect yourself.

Your absolute greatest negotiation tactic is your walk-away power. Always keep a backup property in the back of your mind. If the seller refuses to be reasonable, confidently walk away.

Due Diligence Phase

The seller accepted your offer! The house is officially “under contract.” Now, you enter the critical due diligence phase, where you verify that the house is exactly what it appears to be.

Home Inspection Details

Schedule a full, comprehensive home inspection immediately. A standard inspection costs between $400 and $600 and covers the foundation, plumbing, electrical, and HVAC systems.

Depending on your region, consider purchasing add-ons like a radon gas test or a sewer line scope. Pay very close attention to massive red flags during this phase, such as an aging roof nearing the end of its lifespan or deep, structural foundation cracks.

Appraisal and Title Search

While you focus on the physical house, your lender will order a professional appraisal. The bank wants to ensure the property is actually worth the amount you are requesting to borrow. If the appraiser undervalues the home, you will face financing challenges and must renegotiate the price with the seller.

Simultaneously, the title company will run a deep background check on the property’s history. They will verify that the seller holds the absolute legal right to sell the home and ensure there are no unpaid tax liens secretly attached to the deed.

Final Walkthrough

About 24 to 48 hours before you officially close, you will conduct a final walkthrough of the empty property. This is your last chance to verify that the sellers completed all negotiated fixes and that they did not damage the floors or walls while moving their furniture out.

Insurance Shopping

You cannot secure a mortgage without providing proof of homeowner’s insurance. Start shopping for policies early, keeping in mind that the national average runs about $1,500 per year.

If your new home is in a designated flood zone (always check the official FEMA maps), your lender will require you to purchase a separate flood insurance policy. Additionally, if the home is part of a Homeowners’ Association (HOA), review their bylaws carefully and confirm their monthly fees.

Closing Day Essentials

The finish line is finally in sight. Closing day is when the property legally transfers from the seller’s name to yours.

Review the Closing Disclosure

Exactly three days before your scheduled closing date, your lender is legally required to send you a Closing Disclosure. This incredibly important document compares your final, locked-in loan terms against the original estimate you received months ago. Use this federally mandated 3-day review rule to scrutinize the paperwork heavily. Ensure there are no surprise junk fees hidden in the fine print.

Sign and Fund

Bring a strong pen to the closing table, because you will be signing a massive stack of legal documents.

You will also wire your down payment and your final closing costs to the title company. Remember, your closing costs will typically add up to 2% to 6% to your total loan amount. Once the paperwork is signed and the local county government officially records the transaction, the house is yours. You finally get the keys!

Post-Close To-Dos

Before you pop a bottle of champagne to celebrate, you have a few immediate chores to tackle.

Go online and update your permanent address with the postal service, your banks, and your employers. Next, drive to the hardware store, buy new deadbolts, and immediately change every single exterior lock on your new house. You never know who the previous owners gave a spare key to.

Lastly, stick to your budget. A surprising 10% of buyers deeply regret not budgeting enough cash for the actual move-in process, which includes moving trucks, immediate painting supplies, and basic furniture.

First-Time Buyer Programs

One of the greatest secrets to buying a first home in the USA is using government assistance. Do not leave free money sitting on the table!

Countless state and local governments offer generous Down Payment Assistance (DPA) grants and deferred loans. These localized programs can provide up to 5% in direct financial assistance to help you cover your down payment and closing costs.

If you are brave enough to buy a distressed property that needs major renovations, look into the FHA 203(k) rehab loan. This incredible program allows you to roll the purchase price of the home and the cost of all your planned renovations into one single, easy-to-manage mortgage.

Common Pitfalls to Avoid

As a beginner learning how to buy a house in the USA, it is incredibly easy to make expensive mistakes. Keep your guard up and avoid these common pitfalls.

First and foremost, do not let your emotions override your budget. Overbidding out of sheer desperation will leave you “house poor” and struggling to pay your daily bills.

Secondly, never skip your home inspection. In competitive markets, buyers sometimes waive their inspection contingency to make their offer look more attractive. This is a catastrophic mistake that can cost you tens of thousands of dollars in hidden damages.

Finally, do not ignore the fine print of HOA fees. A cheap condo might look appealing until you realize the mandatory HOA fees add an average of $300+ to your monthly expenses. Interestingly, 13% of buyers back out of a deal after the inspection precisely because they realize they underestimated the property‘s true cost.

FAQs

Here are some quick answers to the most common questions first-time buyers ask:

How much down payment do I actually need? You absolutely do not need to put down 20%. While 20% helps you avoid private mortgage insurance, most first-time buyers put down between 3% and 20% and use FHA or Conventional loans.

Can foreigners buy property in the US? Yes, foreigners can legally purchase real estate in the United States. However, securing a traditional US mortgage as a non-citizen is highly complex, making all-cash purchases significantly easier.

What is the typical timeline for buying a house? From the moment the seller accepts your offer, the escrow and closing process typically takes 30 to 60 days to complete.